Today I decided to sell a good performer of mine and reallocate profits into the right now hated sector of gambling.

Gambling as a sector is going through a lot of pressure right now mainly because of 2 factors:

- Competitors in the predictions markets space like Polymarket and Kalshi

- Increasing Tax and regulation concerns

Big companies like $DKNG (+1,5 %) , $PENN (+1,12 %) , $ENT (+0,58 %) and $FLTR (+0,28 %) are collapsing in the stock market because of these fears.

Why I chose to buy Flutter Entertainment $FLTR (+0,28 %) then?

Flutter operates both online betting and in retail stores around the world.

It operates more or less like a serial acquirer in the gambling sector.

1) Flutter is market leader in mutiple markets around the world and is currently using the cash flow produced from mature and profitable markets like Italy, Uk, Australia and Ireland to finance is expansion in high-growing markets like Brasil and the USA.

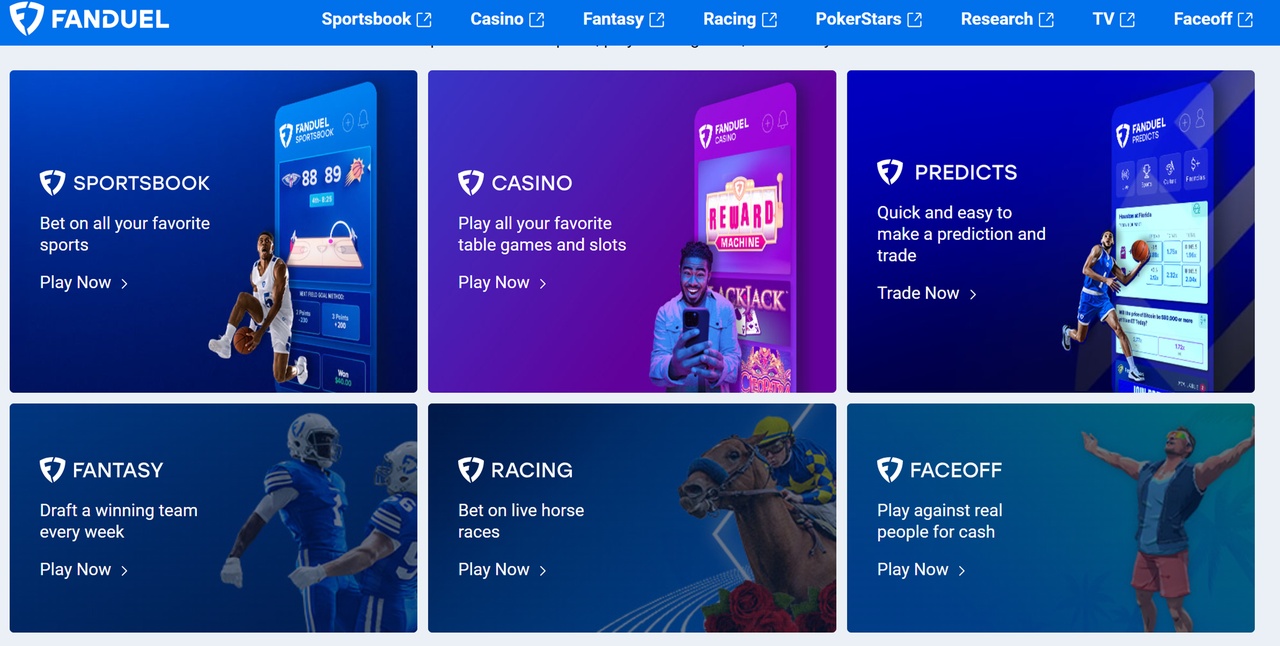

Fanduel has over 40% marketshare in the USA and NSX Group (owned by Flutter) is the leading brand in Brasil.

It is market leader in a lot of developing countries like Turkey and Morocco throught the brand Sisal, in Georgia and Armenia through the brands Adjarabets.

Brazil and USA only recently allowed online gambling bets that's why Flutter is spending a lot of money to quickly capture market share in both these new 2 countries.

2) It recently started a parternship with financial giant $CME (+0,85 %) to provide market prediction directly in Fanduel to compete against Polymarket

3) The Turkey case: Recently Turkey decided to close all illegal online betting websites and that cause an increase of revenue of over 30% for Flutter in the region.

Flutter is a highly regulated entity who collaborate not only with professional leagues but also with nations across the world and that alone made Flutter the favourite default choice.

4) $AMZN (-1,07 %) Partenrship: In the USA now you can bet directly into the Prime app ecosystems during sports events increasing the fluidity and the experience for customers.

5) The Morocco case: in Morocco it operates through the brand Sisal but government allow only the national lottery. Flutter only provides the software and all the payout is in the hand of the local government.

That's a high recurring, high margin revnue model that can be potentially exported in other markets

6) Margin compression: Flutter is investing heavily in USA and Brazìl and that's why margin are compressing, however this are temporary costs linked to promotions, advertising etc...

7) The India case: India recently banned online betting in every form and Flutter lost a big market there.

However it still operates as a gaming platform with mobile phone games (with no money bets) and hoping that one day regulation will change.

If regulation changes in the future Flutter already has customers, games and distribution.

It is currently using the indian market as a test market for different type of games.

Yes, it is an unprofitable market for obvious reasons.

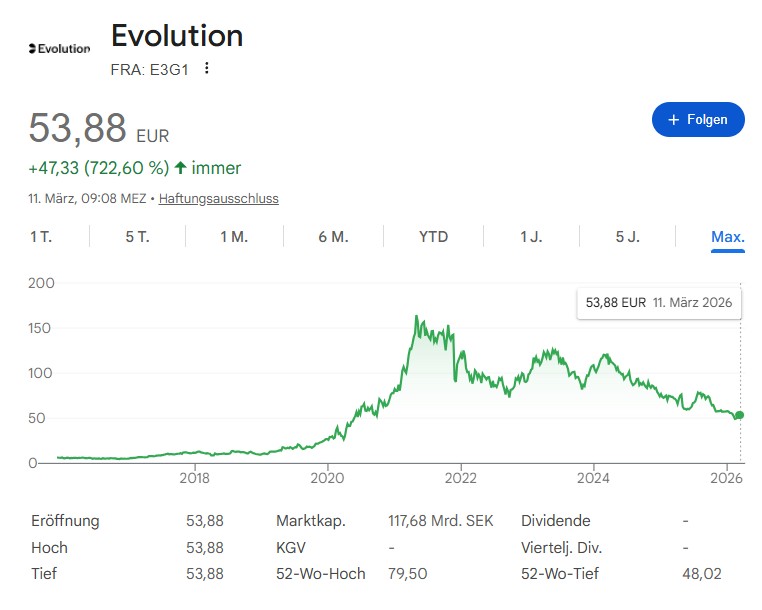

8) Flutter has the biggest selection of high quality casino games produced by market leaders like $HACK (+0,16 %) and $EVO (+2,61 %) and it's the platform who offers most games.

Casino games are important because they represent the most profitable chunk of the revenue.

9) Macroevents like the Football world cup will instantly increase demand for betting in all markets.

It's the biggest competition in the world and now for the firs time it has more teams who partecipates than ever.

10) Online betting has a TAM of approximately 300bln$ worldwide, flutter currently has 16bln$ revenue so the unpenetrated market opportunities are still huge.

Flutter is also the only gambling company who operates as a serial acquirer around the world and have a presence in almost every country in the world.

11) Recently England increased taxes on betting and that hit direclty Flutter's EBITDA margins, however the compnay is still profitable and market regulation is an intrinsic risk in the sector that cannot be erased, but only reduced thanks to geographic diversification.

12) The company is trading at the same price it was trading in 2017 however the business as a whole improved a lot both in terms of revenue and geographic expansions.

13) Debt is high due to the acquisitions like Snai in Italy, Fanduel in Usa and NSX in Brasil.

During the conference call Management said that it stopped the acquistion spree and is now focused to pay down debt and increase profitability.

It started by removing bonus and decreasing marketing costs in the USA, Italy and UK.

Even after cutting marketing costs customers still increased (On the earnings presentation it shows a decrease in number of users because they removed the indian market due to regulations, if you adjust the data it shows a significative increase).