Hello everyone 👋

I have to be honest and say that the last few days have been a bit too exhausting for me. Following every company, and there have been more and more, has become too much for me 🤯 - and I realize how much time it takes to check the individual price movements (to always find the "best" entry). 🕵️♂️📈

I'm still young and actually want to fill my time with more effective things than constantly checking the prices. 📉📊📈

So I've drawn up a list of stocks where I think it's enough to look at the portfolio once a week or maybe even just once a month, because I assume that they will be higher in a year's time than they are now. 🚀

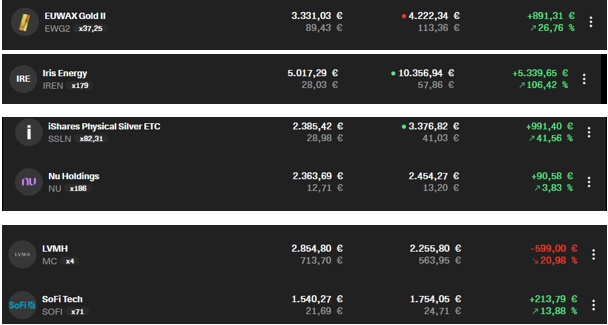

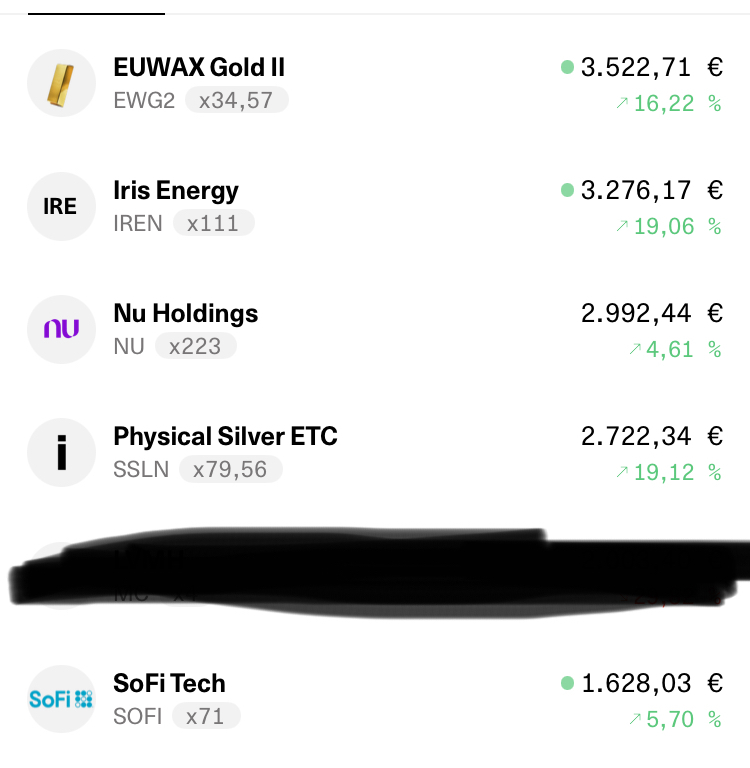

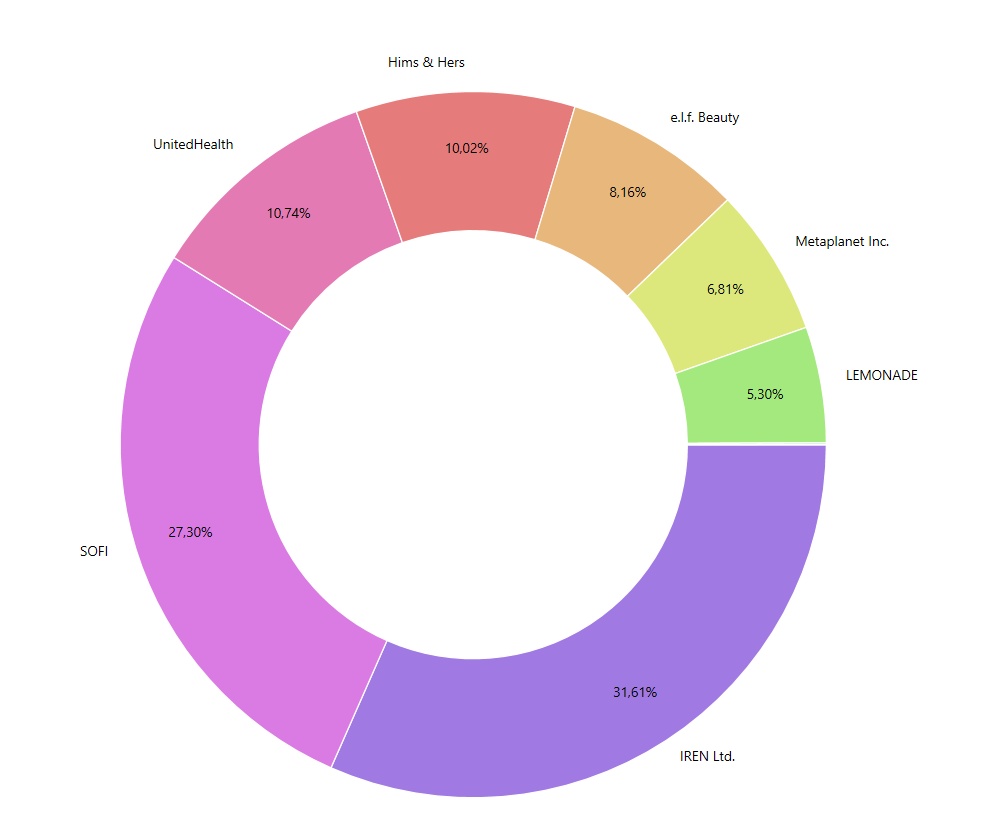

That's why I now only have seven companies in my portfolio and $BTC (+1.37%) 💰

Bitcoin:

All 7 stocks were increased, and all other positions were allowed out (I still have warrants, but these are also to be gradually reduced!).

$PNG (-3.88%) - (only a little, waiting for a setback)

$IREN (+5.74%)

$ONDS (+4.18%) (should also be out of the portfolio by the end of the year)

$RKLB (+2.27%)

$IPX (+2.36%)

$SOFI (+1.18%) - (increased the most because the position was previously very small)

$BNTX (-0.17%) - (unfortunately there was no money left today 😅)

Each company has a weighting of approx. 10/15% in the portfolio. IREN and Kraken Robotics a bit more, because I see the biggest upside there 💶

I know that these are stocks that would probably give value investors gray hair 😅,

but I'm deliberately focusing on growth. And even if one or two stocks take off, I will have achieved my target return of 25% per year. 💪📈

Please give me feedback on whether you think it makes sense to have such a concentrated portfolio - or whether you would say that the time investment is worth it after all and I would be rewarded with a return. 🤔📊

Kind regards ✌️

Small investor 😁