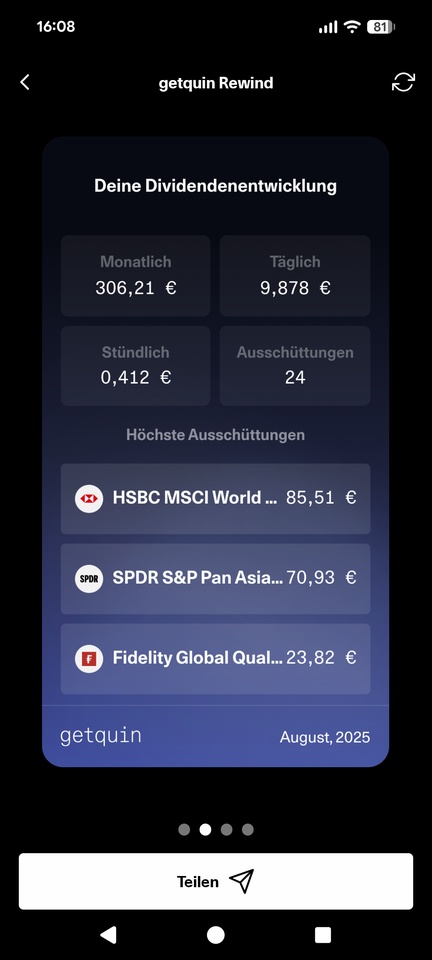

August wasn't so great for me either. But September is looking better so far...:) #rewind

The top 5 performers

$UNH (-5.78%) +20

$NOVO B (-3.44%) +16

$ENPH (-7.46%) +12

$LOW (-1.93%) +10

$8031 (-4.68%) +10

Posts

39August wasn't so great for me either. But September is looking better so far...:) #rewind

The top 5 performers

$UNH (-5.78%) +20

$NOVO B (-3.44%) +16

$ENPH (-7.46%) +12

$LOW (-1.93%) +10

$8031 (-4.68%) +10

You have $5,000 to build a portfolio, how are you building it based on these prices:

$1,000 each - $AAPL (-4.63%)

$TSLA (-6.86%)

$NVDA (-6.14%)

$MSFT (-3.3%)

$META (-5.02%)

$750 each - $HD (-1.47%)

$SBUX (-2.43%)

$LOW (-1.93%)

$AVGO (-7.17%)

$COST (-2.05%)

$500 each - $JNJ (-0.5%)

$ABBV (-1.22%)

$CSCO (-3.83%)

$UNH (-5.78%)

$KO (+0.18%)

🔹 Revenue: $23.96B (Est. $23.96B) 🟡; UP +2% YoY

🔹 Adj. EPS: $4.33 (Est. $4.24) 🟢; UP +6% YoY

🔹 Comp Sales: +1.1% YoY

FY25 Guide (updated for ADG acquisition)

🔹 Revenue: $84.5B–$85.5B (Est. $84.4B) 🟢

🔹 Oper. Margin: 12.1%–12.2% (Prev. 12.3%–12.4%) 🔴

🔹 Adj. EPS: $12.20–$12.45 (Est. $12.22) 🟡

🔹 Comp Sales: Flat to +1% YoY

🔹 Adj. Operating Margin: 12.2%–12.3%

🔹 CapEx: ~$2.5B

🔹 Tax Rate: ~24.5%

Operational & Strategic Updates

🔹 Retail footprint: 1,753 stores; 195.5M sq. ft.

🔹 Acquired Artisan Design Group (ADG) in June; strengthens Pro/new home construction segment

🔹 Capital allocation: $1.3B invested in ADG acquisition; $645M paid in dividends

Management Commentary

🔸 CEO Marvin Ellison: “Positive comps driven by both Pro and DIY despite weather headwinds; ADG acquisition expands our Pro reach.”

You have $5,000 to build a portfolio, how are you building it based on these prices:

$1,000 each - $AAPL (-4.63%)

$TSLA (-6.86%)

$NVDA (-6.14%)

$750 each - $HD (-1.47%)

$SBUX (-2.43%)

$LOW (-1.93%)

$AVGO (-7.17%)

$500 each - $JNJ (-0.5%)

$ABBV (-1.22%)

$CSCO (-3.83%)

$UNH (-5.78%)

$WMT (-0.92%)

$TGT (-4.66%)

$HD (-1.47%)

$LOW (-1.93%) Walmart, Home Depot, Lowe's and Target attend White House meeting

Target announces meeting to discuss next steps for retailers

US retailers suffer from tariffs and shrinking profit margins due to import dependence

WASHINGTON, April 21 (Reuters) - U.S. President Donald Trump met with major retailers including Walmart (WMT.N), opens new tab, Home Depot (HD.N), opens new tab, Lowe's (LOW.N), opens new taband Target (TGT.N), opens new tab to discuss broad-based tariffs on Monday that will likely raise the cost of imported everyday goods.

Major U.S. chains like Walmart and Target rely heavily on imported goods, and tariffs - including 145 percent levies on China - are likely to add to a U.S. population already burdened by persistent inflation.

🔹 Adj EPS: $1.93 (Est. $1.84) 🟢

🔹 Revenue: $18.55B (Est. $18.29B) 🟢;

🔹 Comparable Sales: +0.2%

FY25 Guidance:

🔹 Revenue: $83.5B-$84.5B (Est. $84.64B) 🟡

🔹 Diluted EPS: $12.15-$12.40 (Est. $11.94) 🟢

🔹 Capex: ~$2.5B (Est. $2.28B)

🔹 Outlook Reflects Near Term Uncertainty In Home Improvement Mkt

Other Q4'24 Metrics:

🔹 Net Income: $1.1B; UP from implied $1.0B YoY (based on EPS)

🔹 Stores: 1,748; 195.0M sq ft

Strategic/Shareholder Updates:

🔸 Repurchased $1.4B in shares; paid $650M in dividends in Q4

🔸 Awarded $80M in frontline associate bonuses

Management Commentary:

🔸 "Marvin R. Ellison (CEO): Our better-than-expected results reflect traction with Total Home initiatives, despite near-term DIY pressure, and we’re confident in our long-term strategy."

Wayfair ($W) (-5.47%) was a clear winner in e-commerce during the pandemic, but experienced a drastic crash afterwards. Now that the market has stabilized, investors are asking themselves: Is Wayfair ripe for a comeback or will the company remain under pressure?

Overview: What does Wayfair do?

Wayfair is one of the world's largest online retailers for furniture and home accessories. The company operates an asset-light model, which means that it does not produce its own furniture, but brokers products via a broad network of manufacturers and suppliers.

✅ Wayfair.com: Main platform for online furniture retail in the USA, Canada and Europe.

✅ Wayfair Professional: B2B platform for companies and interior designers.

✅ Perigold, AllModern, Birch Lane and Joss & Main: Other brands covering different design styles.

Wayfair relies heavily on data analysis and AIto understand buying behavior and optimize the supply chain.

Competition: Who are the competitors?

🔸 Amazon ($AMZN) (-5.92%) & Walmart ($WMT) (-0.92%) - Huge competition in online retail, which also offer furniture.

🔸 IKEA - The stationary furniture giant that is constantly expanding its online presence.

🔸 Home Depot ($HD) (-1.47%) & Lowe's ($LOW) (-1.93%) - Important competitors in the Home & Living segment.

🔸 Etsy ($ETSY) (-5.7%) & smaller specialty retailers - Competition from individual furniture and decoration suppliers.

Wayfair has the advantage of being a pure online specialist specialist for furniture, but has to hold its own against financially strong rivals.

Opportunities: Why could Wayfair make a comeback?

✅ Efficiency gains: Wayfair has worked hard on its cost structure and reduced staff in recent quarters.

✅ Stabilization of demand: After the extreme boom in 2020-2021 and the decline in 2022-2023, the market could now normalize.

✅ Improved consumer climate: Falling inflation and potential interest rate cuts could boost purchasing power.

✅ Improved margins: The company has recently achieved higher gross margins, which indicates better cost control.

✅ Expansion of B2B business: Wayfair Professional continues to grow and could be a stable revenue generator in the long term.

Risks: What could continue to weigh on Wayfair? ⚠️

⚠️ High competitive pressure: Amazon, IKEA and Walmart are strong opponents with better supply chains.

⚠️ Dependence on macro factors: High interest rates and weak consumer sentiment could delay the recovery.

⚠️ Profitability remains fragile: Wayfair has made losses in the past and needs to show it can sustain profits.

⚠️ Logistics and storage costs: Despite efficiency gains, shipping bulky furniture remains a challenge.

⚠️ Customer loyalty: Unlike Apple or Tesla, customers have little loyalty to Wayfair - many simply compare prices with the competition.

Conclusion: turnaround opportunity or value trap?

Wayfair could be one of the most exciting turnaround candidates in 2025. The company has worked hard on its cost structure and could benefit from a recovery in consumer sentiment. However, competition remains intense and it is not yet certain whether Wayfair will become sustainably profitable.

What do you think? Does Wayfair have the potential for a strong recovery or will the share remain a shaky candidate? 🚀

Lowe's Q3 FY24 #EarningsReport Summary | $LOW (-1.93%)

In Q3 FY24, Lowe's faced challenges from reduced DIY discretionary demand, partly offset by strong Pro sales, online growth, and storm-related purchases. Despite these challenges, Lowe's demonstrated resilience with earnings exceeding modest expectations.

📊 Income Statement Highlights (vs. Q3 FY23):

▫️ Net Income: $1.70B vs. $1.77B (-4.39%)

▫️ Total Revenue: $20.17B vs. $20.47B (-1.47%)

▫️ Adjusted EPS: $2.89 vs. $3.06 (-5.56%)

▫️ Gross Margin: 33.69% vs. 33.66% (+0.03pp)

▫️ Operating Income: $2.54B vs. $2.70B (-5.93%)

▫️ GAAP Operating Margin: 12.57% vs. 13.17% (-0.60pp)

💼 Balance Sheet Highlights (vs. Q3 FY23):

▫️ Total Assets: $44.74B (+5.23%)

▫️Total Liabilities: $58.16B (+0.86%)

▫️ Shareholders' Deficit: $(13.42)B vs. $(15.15)B (+11.38%)

▫️ Cash and Cash Equivalents: $3.27B vs. $1.21B (+170.25%)

🔮 Future Outlook:

For FY24, Lowe's updated its guidance:

▫️ Total sales: $83.0B–$83.5B (previously $82.7B–$83.2B)

▫️ Comparable sales: Down 3.0%–3.5% (improved from down 3.5%–4.0%)

▫️ Adjusted Operating Margin: 12.3%–12.4%

▫️ Adjusted EPS: $11.80–$11.90

Lowe’s strategic priorities for Q4 include leveraging Pro and online growth, while navigating ongoing DIY demand softness. Anticipated storm-related sales will provide modest tailwinds.

Given the continued stability of real estate prices and expected demand driven by factors such as urbanization and immigration (at least in the US), I see several sectors and companies benefiting from this trend:

REITs, $DHI (-1.25%) , $LEN (+0.32%) , $HD (-1.47%) , $LOW (-1.93%) , $CAT (-2.48%)

However, there has already been a good boost in the current YTD.

Have a nice Sunday everyone!

Top creators this week