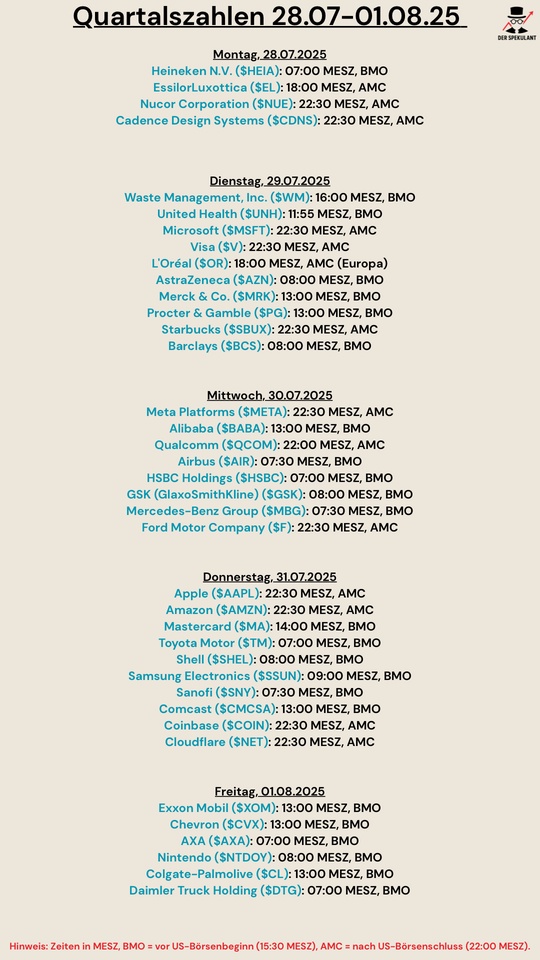

$XOM (+1.51%)

🔹 Adj. EPS: $1.64 (Est. $1.56) 🟢

🔹 Revenue: $81.51B (Est. $80.39B) 🟢

Production & Operational Metrics

🔹 Total Production: 4.63M BOE/d (Est. 4.51M) 🟢; Highest Q2 since Exxon-Mobil merger

🔹 Permian: Record 1.6M BOE/d

🔹 Refinery Throughput: 3.94M b/d (Est. 3.88M) 🟢

🔹 Energy Product Sales: 5.59M b/d

🔹 Chemical Sales: 5.26M tonnes

🔹 Specialty Product Sales: 2.00M tonnes

Segment Highlights

Upstream

🔹 Earnings: $5.4B; DOWN QoQ

🔹 Record Q2 production; growth from Permian & Guyana

🔹 Lower realizations offset by higher volumes and cost savings

Energy Products

🔹 Earnings: $1.37B; UP +65% QoQ

🔹 Refining margins improved on seasonal demand

🔹 Strathcona Renewable Diesel (20K bpd) & Fawley Hydrofiner ramping

Chemical Products

🔹 Earnings: $293M; Flat QoQ

🔹 Volumes up from China Complex ramp-up; margins soft

Specialty Products

🔹 Earnings: $780M; UP +19% QoQ

🔹 Record high-value product volumes

🔹 Singapore Resid Upgrade project in start-up phase

Other Key Q2 Metrics:

🔹 Net Income: $7.08B; DOWN -36% YoY

🔹 Cash Flow from Ops: $11.5B

🔹 Free Cash Flow: $5.4B

🔹 Capex: $6.3B

🔹 On pace for $20B buybacks in 2025

🔹 Q3 Dividend Declared: $0.99/share (Payable Sep 10, 2025)

🔹 Net Debt Ratio: 8%; Debt-to-Capital: 13%

Strategic & Efficiency Updates

🔸 Started 6 of 10 major projects YTD

🔸 $13.5B structural cost savings since 2019 (leading among IOCs)

🔸 FY25 Capex forecast: $27B–$29B (unchanged)

🔸 Repurchased ~40% of shares issued for Pioneer acquisition

🔸 “We’re delivering industry-leading results and building long-term earnings power. Our cost structure, scale, and advantaged portfolio continue to differentiate us.” – CEO Darren Woods