Hello everyone!

As announced recently, we are currently pointing our compass more towards the far north. Why? Because, away from the loud and expensive US tech hype, you can still find companies here in Scandinavia that are absolutely world-class in their niche - and earn extremely hard money.

Today we have brought you a very special candidate from Sweden. A former stock market darling and VIP guest in every growth portfolio, but one that has recently been brutally punished by the market.

Today we are asking the all-important question about this Swedish heavyweight: are we dealing with a classic "Fallen Angel" who has just handed us the entry opportunity of the decade on a silver platter? Or are we reaching blindly into a falling knife and falling into the ultimate value trap?

Fasten your seatbelts, we are hunting today $EVO (+1.11%) ruthlessly through the key figures meat grinder!

📜 A quick look at the history books:

From studio in Riga to global monopolist Evolution was founded in 2006 by Jens von Bahr and Fredrik Österberg. The idea was simple but ingenious: they wanted to bring the real casino experience with real dealers directly into gamblers' living rooms via livestream. Starting out in a small studio in Riga, they practically invented the market for live casinos single-handedly and dominated it for years. On their way to the top, they diligently swallowed up competitors such as NetEnt and Big Time Gaming (the inventors of Megaways Slots) and built up a powerful empire.

🃏 What does Evolution do today?

In short, they are the shovelers in the digital gold rush of gambling. Evolution does not operate its own casinos (and therefore bears no direct player risk), but builds and streams live casino games (blackjack, roulette, game shows such as "Crazy Time") for the world's major online casinos. If you offer live casino online, there is practically no way around Evolution's software and studios.

⚔️ The competition: who is peeing on the top dog's leg?

A quasi-monopoly inevitably attracts envious parties. The biggest and most dangerous threat is currently Pragmatic Play. These guys are extremely aggressive, copying successful formats at breakneck speed and forcing their way onto the market with predatory pricing. There are also long-established players such as Playtech (quite a dinosaur, but one that holds on to its market share). Evolution is still the absolute gold standard in terms of quality and innovation, but Pragmatic Play's breathing down its neck is definitely noticeable and costs margins.

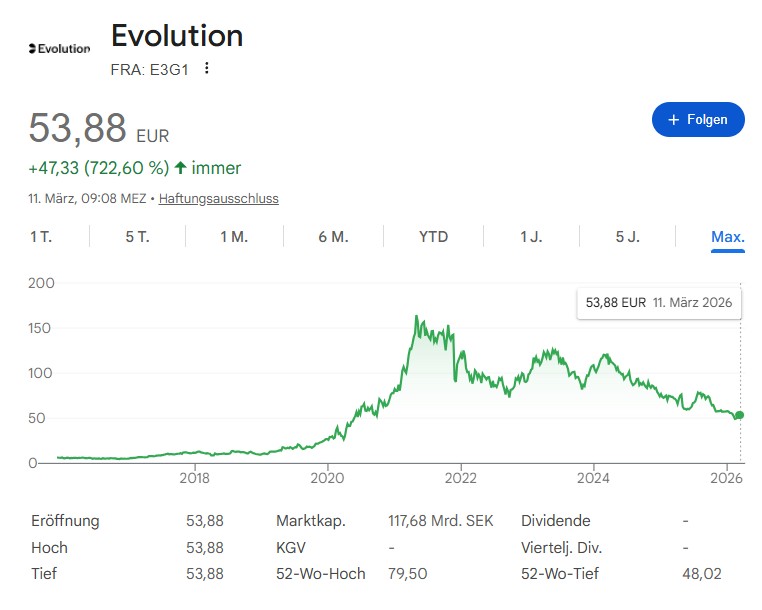

📊 The bare key figures (as of March 2026)

Before we get philosophical, here are the facts on the table (share price currently approx. 566 SEK or 53.50 EUR):

- Price-earnings ratio (P/E ratio): ~10,0 (Historically ridiculously cheap for this company)

- Price-Cashflow Ratio (KCV): ~9,8

- Price-Sales Ratio (KUV): ~5,7

- Price-Book Value Ratio (P/BV): ~3,0

- Dividend Yield: ~5,5 %

🧪 Our endurance test: The formulas

We filter stocks according to strict, qualitative rules. Here is the report card for the Swedes:

1st Core Quality Formula (Qualitative Growth)

- Sales growth (FY 2025): +0,2 % (Ouch. More on that in a moment).

- Operating margin: Insane 58,4 %.

- Score: 0,2 + 58,4 = 58,6

- Verdict: The margin is absolutely perverse (in a positive sense). Evolution keeps almost 60 cents of every euro earned as operating profit. The score is gigantic, BUT Growth has recently come to a complete standstill.

2. cash flow quality formula (the cash machine)

- Free cash flow (FCF): ~ SEK 12.5 bn (approx. EUR 1.12 bn).

- FCF yield:

~10,8 % * Verdict:

Extremely attractive. An FCF yield of almost 11% means that Evolution is currently an unparalleled cash cow. Nothing is glossed over in the balance sheet here, the free cash flow is literally bubbling over.

3. dividend filter (income check)

- Dividend yield: ~5,5 %

- Verdict:

Passed with an asterisk. The payout ratio is a conservative ~51%. The dividend is completely covered by the massive cash flow, there is virtually no debt. No "pseudo payout", but real income.

🚨 What's the catch? (opportunities & risks)

When a market leader with a margin of almost 60% is trading at a P/E ratio of 10, the market smells blood.

The risks: Sales growth (previously reliable at 20-30% per year) has recently hit the brakes. This is due to increasing regulation (including in the UK), stubborn competition and problems in Asian "gray markets". There have also been repeated staff strikes in the studios. The market has downgraded Evolution from an untouchable growth star to a value stock.

The opportunities: The valuation is now a joke. Even if Evolution never grows again, for a P/E ratio of 10 you get a company with an FCF yield of almost 11% and a secure 5.5% dividend, which also pumps the rest of the money massively into share buybacks.

🎯 Share price targets: Where is the journey going?

If you look at the analysts of the major banks, the average target price is currently just under 650 to 680 SEKalthough the bulls (such as Morgan Stanley) still have targets of over 800 SEK . This would correspond to an upside of a good 20 % to 40 % from the current level.

But be careful: These higher targets are based on the assumption that Evolution will restart growth (towards 5-10 % per year), for example through a wave of legalization in North America. If growth remains permanently at zero, the share is fairly valued at the current price of just under SEK 570 - then it is "only" a first-class, extremely high-yielding dividend bond.

⚔️ The competition: who is peeing on the top dog's leg?

A quasi-monopoly inevitably attracts envious parties. The biggest and most dangerous threat is currently called Pragmatic Play. These guys are extremely aggressive, copying successful formats at breakneck speed and forcing their way onto the market with predatory pricing. There are also long-established players such as Playtech (quite a dinosaur, but one that holds on to its market share). Evolution is still the absolute gold standard in terms of quality and innovation, but Pragmatic Play's breathing down its neck is definitely noticeable and costs margins.

🏁 Conclusion for the forum

If you are strictly dependent on dynamic growth, the current stagnation is a red flag. Evolution must then be placed on the watch list until sales growth picks up again. But if you love falling knives with a dominant market position and want to sweeten the wait with a 5.5% dividend and 11% FCF yield, you will hardly find a better bargain at the moment.

What do you think? A value trap or an opportunity?