I entered Vitec Software today with an initial position.

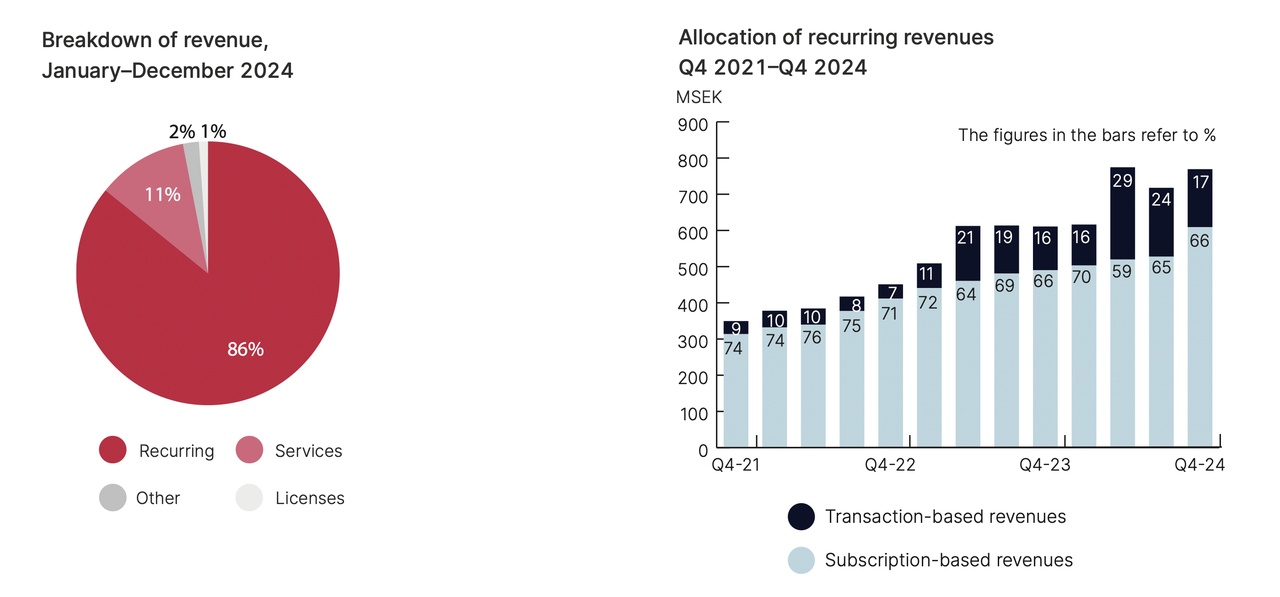

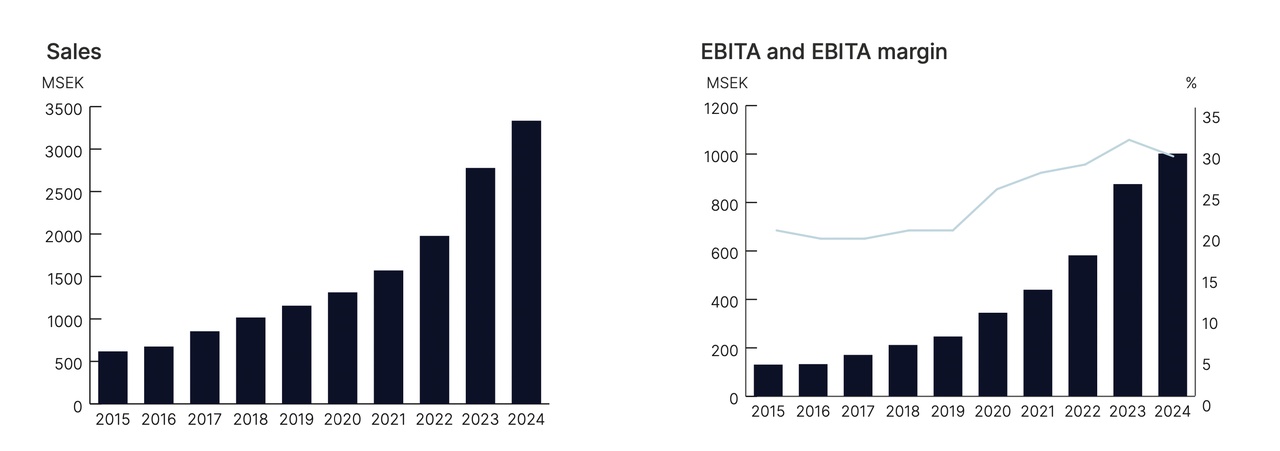

The company has been doing the same thing for over 20 years. It buys small, specialized niche software companies in Europe, lets them operate autonomously and reinvests the free cash flow in the next acquisition. Over more than a decade, Vitec has achieved an ROIC of around 30% on its acquisitions. 88% of sales are recurring and the customer retention rate is just under 99%. The founder is still on the board.

The market is currently penalizing a single negative factor - an energy market-sensitive subsidiary in Norway - with a valuation discount that calls the entire model into question. The EV/EBITDA is 8.5×, the historical average is 23×. The direct peer Topicus trades at 14×. In my view, this gap is not fundamentally justified.

With this investment, I am deliberately increasing my exposure to Europe. My portfolio was previously too US-heavy, and Vitec is a Swedish company with customers in 13 European countries, which offers exactly the geographical complement that I would like to see in the portfolio.

I entered with 40% of the planned budget. A second tranche will follow at ~€16 if the share price reaches this level.

I am reserving the third tranche for after the Q1 figures on April 23 - this will also only take effect if the price is still at this level and the margin improvement becomes visible.

I see profit zones at ~€28, where I would sell 25%, and at ~€40 for a further 40%. Hard stop is at ~€14.

Three scenarios: In the bullish case with 45% probability, I see ~€54 as the target price. In the neutral case with 40% probability ~€30. In the bearish case with 15% probability ~€15. The weighted expected value is around €39, the CRV just under 4:1. This is of course not investment advice. Time will tell whether I am right.

edit: the text was not copied when posting. Great to see that @Raketentoni also sees the approx. 16 € :)