Summary Earnings, 07.11.

$MUV2 (+0.58%)

| Munich Re Q3 24 Earnings

EPS EU7.02 (est EU6.67)

Sees FY Insurance Rev. About EU61B, Saw About EU59B

Sees FY Profit Above EU5B, Saw EU5B

$RHM (+0.42%) | Rheinmetall AG Q3 24 Earnings

Sales EU2.45B (est EU2.42B)

Still Sees FY Sales About EU10B (est EU9.99B)

Sees FY Operating Margin At Upper End Of Guidance

Nissan Motor Q2 2024 Earnings $7201 (-0.88%)

Q2 Operating Income 31.91B Yen (est 65.25B Yen)

Q2 Net Loss 9.34B Yen (est Profit 49.07B Yen)

Sees FY Oper Income 150.00B Yen, Saw 500.00B Yen

To Cut 9,000 Jobs Globally

To Reduce Global Production Capacity By 20%

To Sell Back Up To 10.02% Of Mitsubishi Motors Shares

Air France KLM Q3 24 Earnings $AF

EBITDA EU1.90B (est EU1.9B)

Rev EU8.98B (est EU8.88B)

Net Income EU780M (est EU874.3M)

Sees FY Capex EU3B, Saw Below EU3B

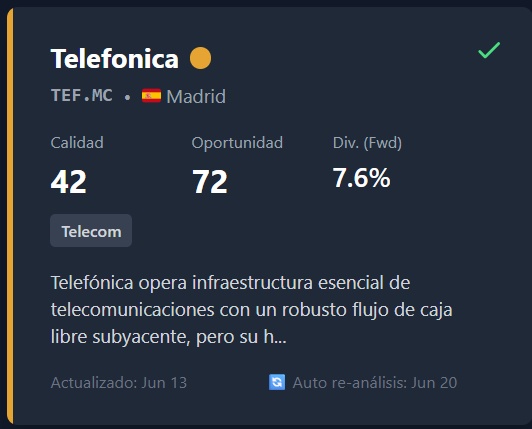

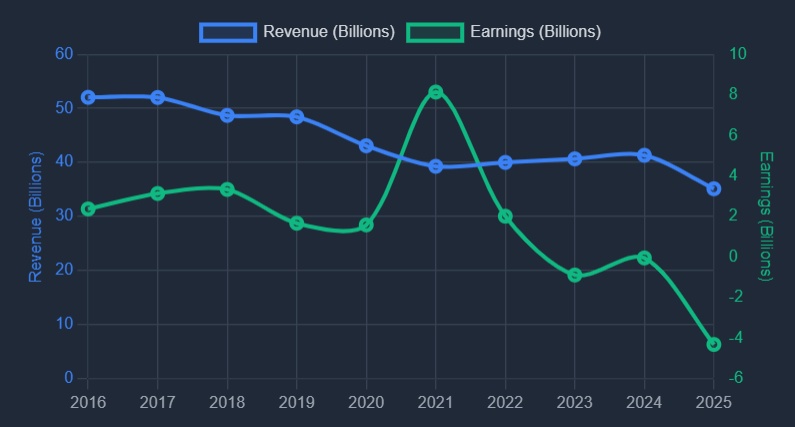

$TEF (+0.1%) | Telefonica Q3 24 Earnings

REV. EU10.02B (est EU10B)

Adj. EBITDA EU3.26B (est EU3.26B)

Net Income EU10M (est EU357M)

To Book €314 Million Non-Cash Impairment For Peru

ArcelorMittal Q3 24 Earnings: $MT (+0.74%)

- Sales $15.20B (est $15.23B)

- EBITDA $1.58B (est $1.47B)

- Still Sees FY CAPEX $4.5B To $5.0B

- Markets Conditions Are 'Unsustainable'

- Positive On Medium/Long Term Outlook

Daimler Truck Holdings Q3 24 Earnings: $DTG (+0.29%)

- Rev EU13.14B (est EU12.98B)

- Adj EBIT EU1.19B (est EU1.13B)

- Still Sees FY Rev EU53B To EU55B (est EU53.45B)

Adyen disappoints with lower than expected sales growth and loses 13% on the stock market. $ADYEN (+0.64%)

Lanxess-shares rise by 4.4% to 26.80 euros after a positive quarterly report, having previously fallen by 13%. The operating margin exceeds expectations, although prices weaken. $LXS (+0.15%)

National Grid increased its adjusted operating profit by 14% to 2 billion pounds in the first half of the financial year and expects an increase of around 10% for the year as a whole. Higher fees in New York and higher revenues in the UK are supporting growth. $NG. (+0.4%)

AMS-Osram increased its profitability in the third quarter despite a decline in sales, but expects business development to be subdued in the fourth quarter and early 2025. To ensure profitability, the company plans further cost reductions of 225 million euros by the end of 2026. $AMS

Suess Microtec is more optimistic after a strong third quarter and now expects to achieve its annual targets in the upper half of the forecast range. Sales are expected to reach 380 to 410 million euros, with an EBIT margin of 14 to 16 percent. $SMHN (+0.9%)

The investment company Mutares slips into the red operationally in the third quarter with an adjusted EBITDA loss of EUR 16.5 million. However, sales increased by 14% to 3.9 billion euros. $MUX (+0.09%)

Delivery Hero expects a free cash flow of EUR 50 to 100 million for 2024 and anticipates GMV growth at the upper end of the forecast of 7 to 9 percent. However, the Group expects adjusted EBITDA to be at the lower end of the range of EUR 725 to 775 million. $DHE

Deutz recorded an 80% drop in profits to EUR 7.2 million in the third quarter and slipped into the red with a bottom line of EUR 2 million. Turnover falls by 14.9% to 430.4 million euros due to a slump in demand. $DEZ (+1.09%)

Compugroup Medical records a decline in EBITDA in the third quarter

EBITDA fell by 12% to 54.9 million euros in the third quarter, but slightly exceeded

analysts' expectations slightly. Turnover falls by 1% to 283.4 million euros

euros, and the company confirms its reduced forecast for 2024. $COP (+1.29%)

Alzchem reports a jump in profits for the first nine months with

a 36% increase in EBITDA to EUR 76.8 million and increases the EBITDA margin to

EBITDA margin to 18.5 %. The Group is sticking to its profit target for 2024

but is aiming for the lower end of the sales forecast due to the discontinuation of low-margin

the lower end of the sales forecast. $ACT (+0.51%)

Nordex is raising its forecast for the EBITDA margin for 2024 and

now expects it to be closer to the upper end of the range of three to four

percent. In the first nine months of the year, the company recorded

an increase in revenue of 14 percent to EUR 5.1 billion and an improved

improved EBITDA margin of 3.7 percent. $NDX1 (+0.08%)

Nemetschek recorded an increase in revenue in the third quarter thanks to the

thanks to the GoCanvas acquisition, Nemetschek recorded a 15.1% increase in revenues to 253 million euros,

however, earnings remained slightly below expectations. The

The operating costs of the acquisition put pressure on profits, so that EBITDA

increases by 6.7 %. $NEM (+0.86%)

Rational increases earnings before interest and taxes in the third quarter

taxes by 18% to just under 78 million euros, exceeding analysts'

analysts' expectations, while sales revenues grew by 8% to 294 million

euros. The company confirms its forecast for the year. $RAA (+0.44%)