The original Maritime thesis remains valid. Seabed awareness and autonomous underwater systems continue to be major technological bottlenecks. Nevertheless, I have revised the DIBS framework.

The reason: “Maritime” was ultimately too narrow a focus. Many of the underlying developments revolve less around shipping than around technological resilience—the ability of nations and companies to protect critical infrastructure, detect threats early, and develop new defense technologies.

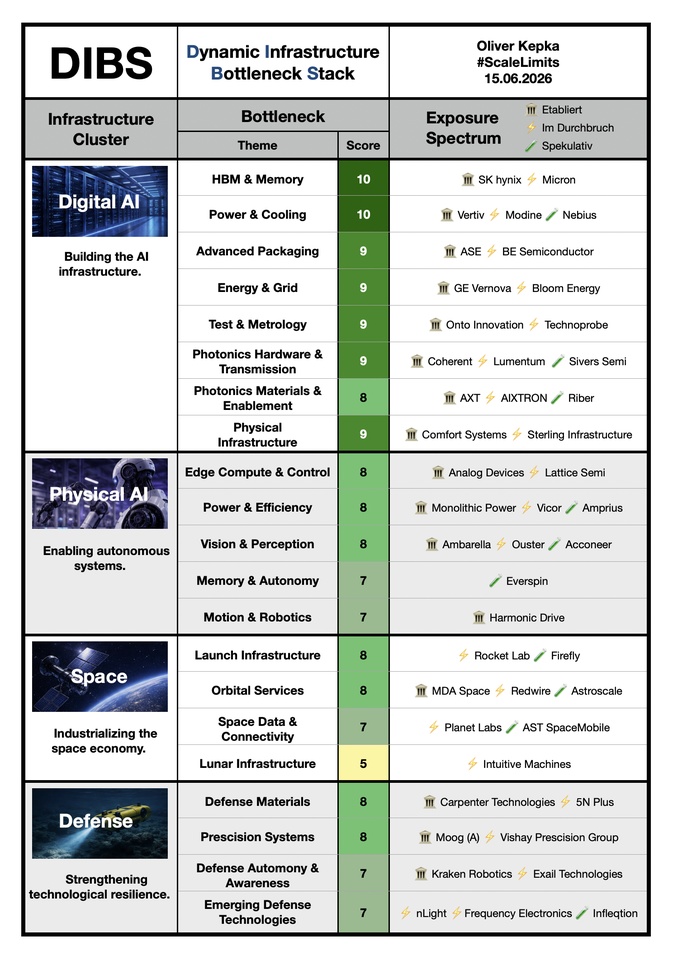

Maritime is therefore becoming Defense.

The Defense cluster comprises four areas:

1️⃣ Defense Materials

Modern defense starts with materials. Special alloys, high-performance metals, and critical materials determine what can be built at all.

• Carpenter Technologies $CRS (+1.24%) – Special alloys for aerospace and defense

• 5N Plus $VNP (+0.92%) – Critical specialty materials for sensor technology and defense applications

2️⃣ Precision Systems

Precision is becoming the bottleneck. Control systems, specialty electronics, and high-precision components determine the performance of entire systems.

• Moog $MOG.A (+3.13%) – Flight control and motion control systems

• Vishay Precision Group $VPG – Precision sensors and measurement technology

3️⃣ Defense Autonomy & Awareness

Detecting threats early and responding autonomously. This is precisely where new requirements arise.

• Kraken Robotics $PNG (+0.86%) – Underwater reconnaissance and maritime sensors

• Exail Technologies $EXA (+0.36%) – Autonomous systems and navigation technologies

4️⃣ Emerging Defense Technologies

The most speculative level of the cluster. This involves technologies that could fundamentally transform future defense—from high-power lasers and precise timing to quantum sensing.

• nLight $LASR – High-power lasers and directed energy

• Frequency Electronics $FEIM (+0.71%) – Timing and synchronization systems for aerospace and defense

• Infleqtion $INFQ – Quantum Sensing and Quantum Technologies

DIBS is not meant to be a static map. My conceptual framework continues to evolve as technological bottlenecks become clearer or can be better structured. The central question, however, remains the same: Where will the critical bottlenecks of the future arise, and which companies occupy the decisive positions in the value chain?

The stocks listed in the table are only a selection. I hold nearly all of them in my own portfolio, and many are also in my three bottleneck wikifolios: NextLimits, TechLimits, and CoreLimits.

I think the DIBS board has now reached a stable state in terms of its structure for the long term. Unless, of course, I come up with something else over the weekend 😁