We went on a little vacation. After all the chilly Scandinavian gems of the last few weeks, we needed some sun. We traveled from Scandinavia to Italy and not only looked at the art, but also dug up one of the continent's most fundamental suppliers. Snam IT (ISIN: IT0003153415) is not a speculative speedboat, but a massive tanker that turns regulated cash flows into returns. After our short trip, we took another close look at the company using our formulas - here is the result. $SRG (-0.39%)

We have also included points 11 and 12 in the analysis from now on - you'll be surprised. We'll be happy to sum up later!

1. the company: What does Snam IT $SRG (-0.39%)

?

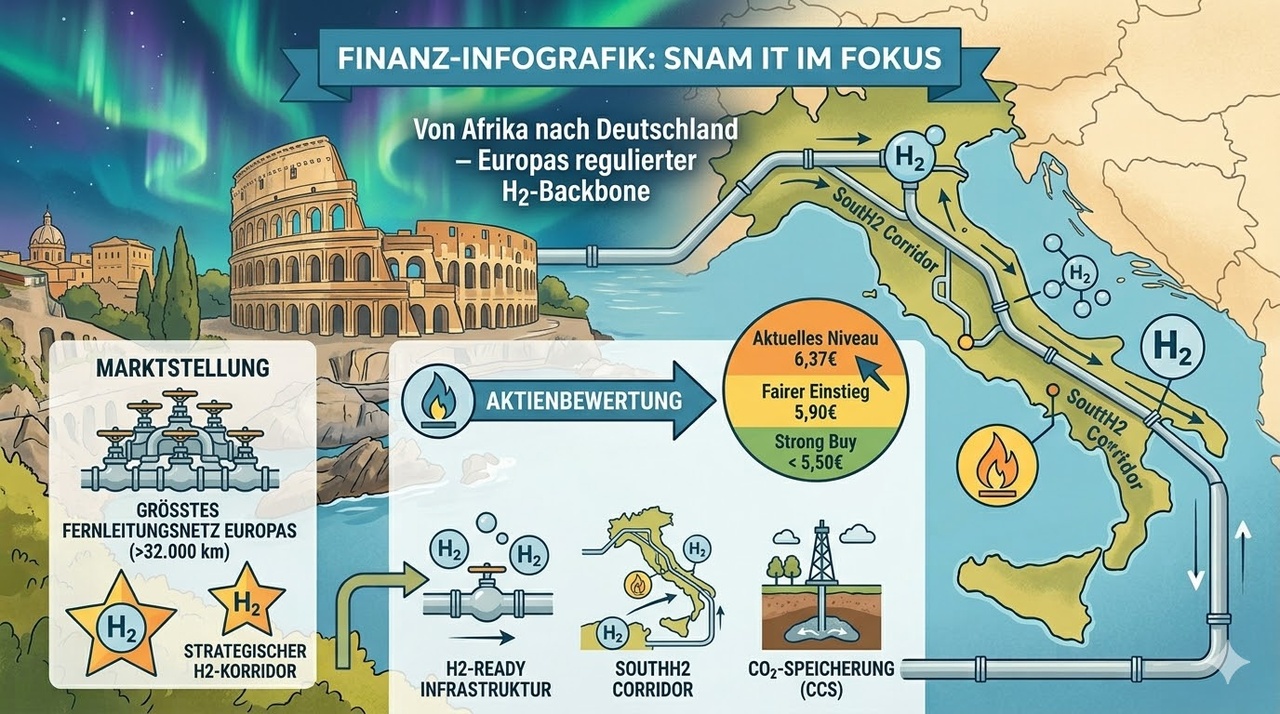

Snam is not just a "gas company". They are the largest transmission system operator in Europe. Think of Snam as the owner of the highways for energy: They own over 32,000 km of pipelines in Italy and control almost 20% of Europe's gas storage capacity. Their latest focus: CO2 storage (CCS) and the SoutH2 Corridor - a hydrogen highway from North Africa to Germany.

2. market position & ticker check

- Market position: Regulated monopoly position in Italy for transportation and storage. They are strategically indispensable for EU energy independence.

- Ticker: The official ticker on the Borsa Italiana is SRG. In Germany often referred to as SNAM in Germany.

3. key figures (as of March 23, 2026)

The share price is currently stable at EUR 6.37. The figures from the recently published 2025 annual report are impressively stable.

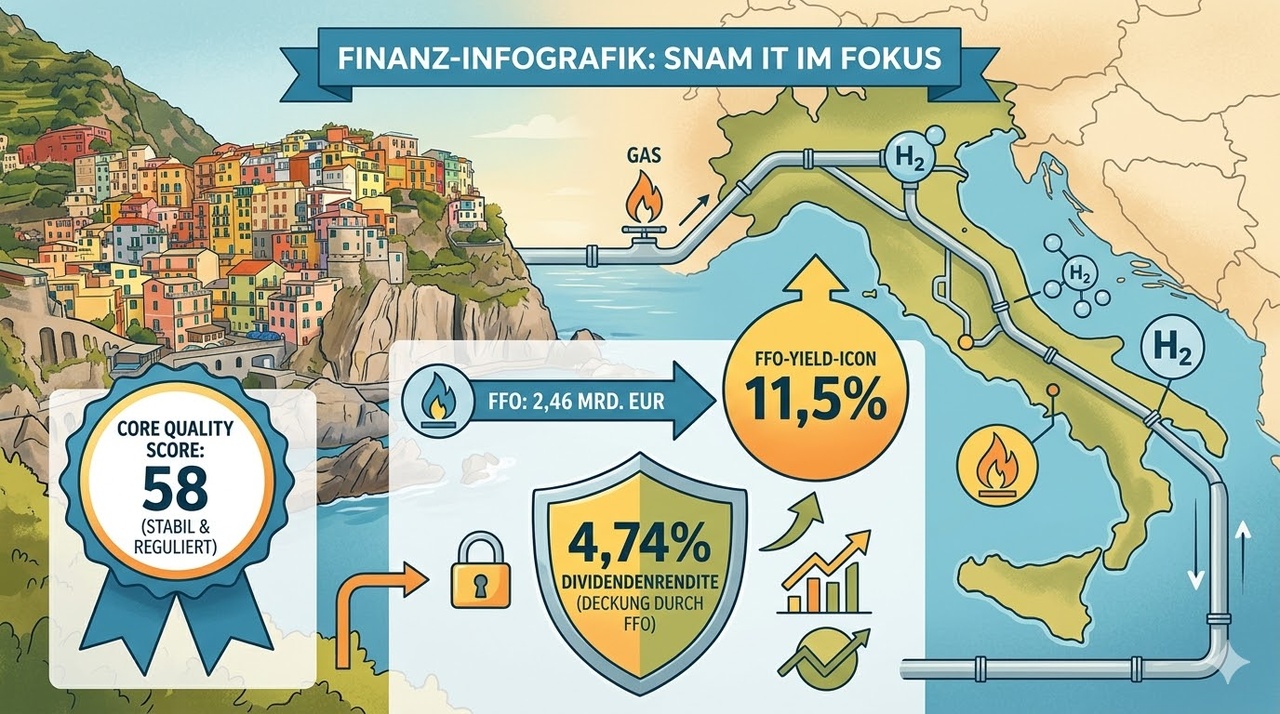

4. core quality formula check

Your filter: Sales growth (%) + Operating margin (%) = Score.

- Sales growth: +8.9 % (to EUR 3.88 billion)

- Operating margin (EBIT basis): approx. 49.1 %

- Result: 8,9+49,1=58

- Conclusion: With 58 points, Snam is well above your "very good" threshold (25). This is the power of a regulated monopoly.

5. cash flow quality formula

- Calculation: Since Snam is making massive CapEx (investments) for the hydrogen ramp-up (EUR 2.63bn net), the free cash flow (EUR 55m) is just positive. The FFO (Funds From Operations) of EUR 2.46 billion, however, shows the true cash generation.

- FFO Yield:

11,5% - Conclusion: The cash machine is running, but is being used for future infrastructure.

6. dividend filter (income core)

- Status: Passed.

- Details: 4.74% yield (EUR 0.3021). The dividend is covered by the FFO. Snam guarantees an annual increase of 4 %. This is a classic income anchor.

7. future prospects & competition

Snam is converting the pipeline system for hydrogen and CCS. The unfair advantage: the pipes are already in place.

- Competition: Enagas (Spain) or Fluxys (Belgium). However, Snam is strategically better positioned due to its geographical location as a bridge from Africa (solar H2).

8. chart analysis & Bargain Hunter's List

We see a healthy consolidation in a sideways phase between EUR 6.30 and EUR 6.60 after the strong recovery of 2023.

- Strong Buy: < EUR 5.50 (extreme margin of safety).

- Bargain Entry: 5.90 - 6.10 EUR.

- Current level: A fair entry for long-term dividend hunters (hold/buy).

9. profit margins & outlook

The operating margin of just under 50 % is phenomenal and secured by the regulated tariffs. Snam is the epitome of stability.

10. sustainability & risk

Snam is the "insurance" in the depot. Its future viability is secured by the conversion to hydrogen. The main risk is the high level of debt (net debt EUR 17.5 bn), but this is covered by the secured RAB (Regulated Asset Base).

11. what does the CEO say? (The latest news)

There has recently been an important change at the helm at Snam: since May 2025 Agostino Scornajenchi has been the new CEO (he took over from Stefano Venier). And Scornajenchi doesn't hesitate for long.

Just a few days ago (mid-March 2026), he presented the new strategic plan 2026-2030 and presented the annual figures for 2025, which even exceeded his own forecasts.

- His key message:

"We are investing around 14 billion euros by 2030 to create an increasingly integrated, secure and competitive Italian and European energy system." * The focus: He talks about an "Energy Integration Phase". It is no longer just about gas, but about making the grid fit for hydrogen, biomethane and CO2 storage (CCS). The management exudes absolute confidence in the stability of future cash flows.

12. analyst consensus: How do the professionals view the share?

Snam is seen by Wall Street and European houses as a classic "widows and orphans" stock, but with new momentum from the hydrogen transition.

- Average price target: The broad consensus (from around 19 analysts) is ~6.05 to 6.10 EURwhich implies a "Hold/Neutral" rating, as the stock has already performed well.

- The bulls: However, there is a breath of fresh air. Goldman Sachs upgraded the share in February 2026 to "Buy" with a target price of EUR 6.90. They justify this precisely with the new 14 billion investment plan and see Snam as undervalued with a P/E discount of 20% compared to direct competitors (such as Terna). Deutsche Bank is even more optimistic and sees the target at EUR 7.20.

- Conclusion of the professionals: A rock-solid dividend stock that is now gaining a slight growth fantasy thanks to the upturn in infrastructure investments in Europe.

My conclusion & future viability (the big picture)

Snam $SRG (-0.39%) is proof that even the old dinosaurs of the fossil era can survive if they have the infrastructure that everyone depends on. For a portfolio looking for a counterbalance to volatile growth or tech stocks, this stock is worth its weight in gold. The dividend is almost set in stone by the Italian state's regulated grid fees and the new CEO is aggressively but profitably driving the transformation to an H2 backbone. If you want to cover the eurozone and sleep soundly at the same time, Snam IT is an absolute no-brainer for the watchlist.

So we have successfully completed our little trip to Italy and added another building block to your AOK library. It's good to have some tangible, physical infrastructure in your portfolio among all the Nordic tech and financial stocks.

@Dividendenopi

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Multibagger

@schlimmschlimm

@Klein-Anleger

@TradingHase

@Simpson

@NichtRelevant

@Abyss

@SAUgut777 and everyone else too :)