I'm already up 100% on $WYFI (+1.93%) since April. It's tempting to take profits, but what's the deal again? Let winners run ;)?

Valuation vs. Growth Restraints

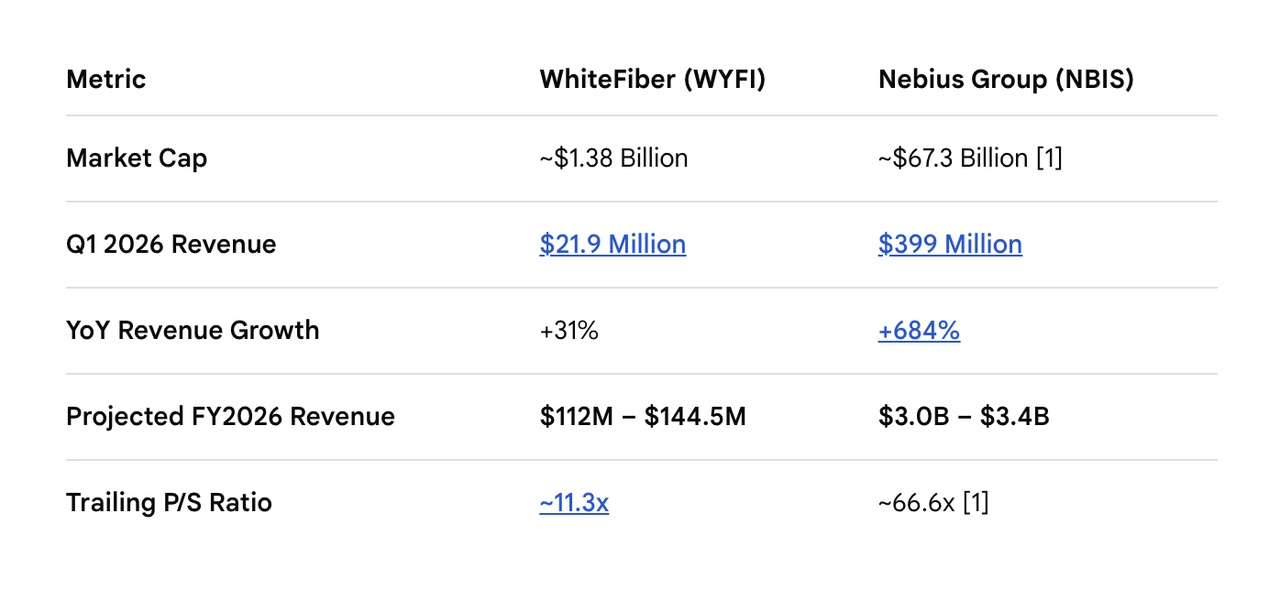

$NBIS (-0.25%) is nicely priced out of this world because of multi-billion-dollar hyperscaler growth. WhiteFiber is vastly cheaper at 11.3x P/S and locked in a solid $865M, 10-year co-location runway.

But WYFI also faces brutal constraints to match that explosive scale:

- The CapEx Wall: Nebius has a $20B+ CapEx budget to hoard next-gen chips. WhiteFiber's whole market cap is only $1.38B. Capacity bottlenecks are a permanent risk.

- The Power Grid: Securing data center electricity is getting cutthroat. WhiteFiber is building mid-tier capacity (40MW contract), but they can't buy up nuclear plants like the big guys.

- Dilution: Without deep cash reserves like Nebius' $9.3B, WhiteFiber has to dilute shares or take on heavy debt to build out servers.

WYFI is a new on the block micro-cap alternative. If they execute their backlogs cleanly, the cheap entry price gives it plenty of room to multiply. But, my issues are:

- Possible diluting with giving away shares?

- Getting more debt to finance power grid buy in?

It's going to be a long wayyyy to reach Nebius level.

Thoughts?