Hello my dears,

I was so pleased that my last space share caused such a great discussion.

Naturally, I continued my search in this exciting sector.

And I found a Japanese champion.

It is important for me to start by pointing out the opportunities and risks:

- We are in the more speculative area here

- Opportunities due to low competition in an emerging market worth billions

- At the same time, the share remains volatile, as the business model is capital-intensive and sales will only scale with increasing commercialization.

- Triple-digit sales growth

- With triple-digit growth in net income, the company will be profitable in 2028

- Not yet profitable at present

- Trading volume currently low, which is typical for smaller Japanese growth stocks in foreign trade

- Net debt is rising dramatically (as is the case for almost all companies in the sector)

- CAPEX almost doubles

- Free cash flow is negative

- 2028 P/E ratio is around 204x

- EBIT margin negative / 2028 positive in the single-digit range

Even if here @Raketentoni will write:

" This is the ride on the cannonball "

I don't see everything so negatively here, and can also see great opportunities. The stock market plays the future, and I see it very well here.

Ladies and gentlemen, how do you see the future and the company here?

I look forward to your comments after reading my company presentation on Astroscale $186A (+2.7%) .

Commercial operators

Our daily lives depend on the continuous functioning of satellites that provide a variety of services, including global communications, navigation and detailed imagery of the Earth. However, commercial operators providing these services in all orbits via their high-value assets face various challenges, such as fuel consumption, collision hazards from expired satellites and other debris, failures of key subsystems or delayed replacements.

Civilian government

The global space arms race is accelerating more than ever, and nations are working together internationally to promote growth and solve national and international challenges through cutting-edge technologies.

National Security

As nations seek to monitor threats and deter adversaries in space, defense sectors worldwide are increasingly recognizing the value of in-orbit maintenance and RPO to secure satellite operations.

Astroscale Holdings Inc. is a Japan-based company engaged in the research and development of technologies related to on-orbit services such as debris removal and in-space demonstrations. The company offers four services, including EOL (End-of-Life) service, ADR (Active Debris Removal) service, LEX (Life Extension) service and ISSA (In-Situ Space Situational Awareness) service. The EOL service is a removal service that prevents satellites that have ceased operations from becoming debris. The ADR service is a service to remove existing debris by launching a service company of the Group, which captures the existing debris, descends into its orbit and burns it in the atmosphere. The LEX service is a service to extend the operational life of a satellite or to transfer it to another orbit. The ISSA service launches observation satellites, safely approaches objects at close range and collects data about the target object that can be used to analyze the cause of the failure and understand the target object.

Customers

- United States Space Force

- CNES

- JAXA

- ESA

- Eutelsat Oneweb

- British Space Agency

GOALS ~2027: Become a trusted partner for defense agencies and governments. 2030: Make on-orbit servicing (OOS) routine. 2035: Enable a circular space economy for prosperous space development.

ADRAS-J selected for the Minister of Defense Award

February 3, 2026

ADRAS-J Selected for the Minister of Defense Award

Astroscale Japan selected for JAXA's Space Strategy Fund program

Published on January 29, 2026

Development of electric propellant refueling technology for Geostationary Orbit Services

Tokyo, Japan, January 29, 2026 - Astroscale Japan Inc ("Astroscale Japan"), a subsidiary of Astroscale Holdings Inc, the leader in satellite services and long-term orbital sustainability across all orbits, has been selected as an implementing organization for the Japan Aerospace Exploration Agency's Space Strategy Fund Program. Under the theme of "Technology to realize flexible spatial mobility", Astroscale Japan will promote the development of electric propellant refueling technology to support future services in geostationary orbit.

Astroscale Japan Selected for JAXA’s Space Strategy Fund Program

Exotrail and Astroscale France join forces to build deorbit capability for LEO

from January 28, 2026

The partnership is designed as a multi-year collaboration. "This framework with Astroscale is much broader than just a one-off opportunity," said Maria. "The idea is to find a partner not only for this mission, but also to build a real commercial capability. What we want to show the market is that now is the right time to partner."

Astroscale UK has been awarded an ESA contract to develop a world-first in-orbit modernization and refurbishment service

Published on January 13, 2026

Harwell, Oxfordshire, January 13th, 2026 - Astroscale Limited ("Astroscale UK"), a subsidiary of Astroscale Holdings Inc, the world's leading in-orbit service provider, has been awarded a EUR 399,000 (approximately £350,000) Phase A contract by the European Space Agency (ESA) to lead the In-Orbit Refurbishment and Upgrading Service (IRUS), a pioneering mission concept that will enable satellites to be refurbished, repaired and extended while in orbit. This initiative supports the Space Safety Programme ESA and underlines Europe's commitment to reducing orbital risks and ensuring safe operations for future generations.

With the participation of the spacecraft manufacturer and operator BAE Systems as a future in-orbit service customer, IRUS represents a significant step towards a circular space economy where satellites are serviced, repaired and upgraded in orbit rather than being treated as a single-use asset. The development of this new capability will pave the way for more complex In-Orbit Servicing, Assembly and Manufacturing (ISAM) opportunities - as refurbishment and upgrades are essential prerequisites for the assembly and manufacturing of platforms in space.

Astroscale expects further satellite orders from the UK and Japan

Sep 16, 2025

The Tokyo-based company forecasts that defense-related revenue from the UK, US and Japan will grow this fiscal year, as well as government missions with the UK, Japan and the European Space Agency.

Astroscale achieved record quarterly revenues in the first quarter, with defense contracts accounting for 30% of total volume. The largest deals include a $41 million APS-R refueling mission with the US Space Force and a YEN 6.6 billion ($44.6 million) project with the Japanese Ministry of Defense, Matsuyama said.

Astroscale erwartet weitere Satellitenaufträge aus Großbritannien und Japan – The Japan Times

30.05.2025

TOKYO, May 30, 2025 - (JCN Newswire) - Honda R&D Co, Ltd. ("Honda"), a research and development subsidiary of Honda Motor Co, Ltd, will jointly develop a new spacecraft with Astroscale Japan Inc ("Astroscale"), a subsidiary of Astroscale Holdings Inc

to develop a refueling port connection system designed for in-orbit refueling of satellites. Honda will apply its mechatronics technologies accumulated through ongoing robotics research to jointly develop the connection system, with the aim of integrating it. with Astroscale RPOD (Rendezvous, Proximity Operations and Docking) technology so that it can be used in the technology demonstration of satellite refueling in low Earth orbit, Astroscale plans around 2029.

Business Update (October 2025)

Geographical sales distribution 2025:

UK JPY 1.52 billion

Japan JPY 898 million

U.S.A. JPY 26.7 million

France JPY 8.17 million

JPY in millions

Estimates

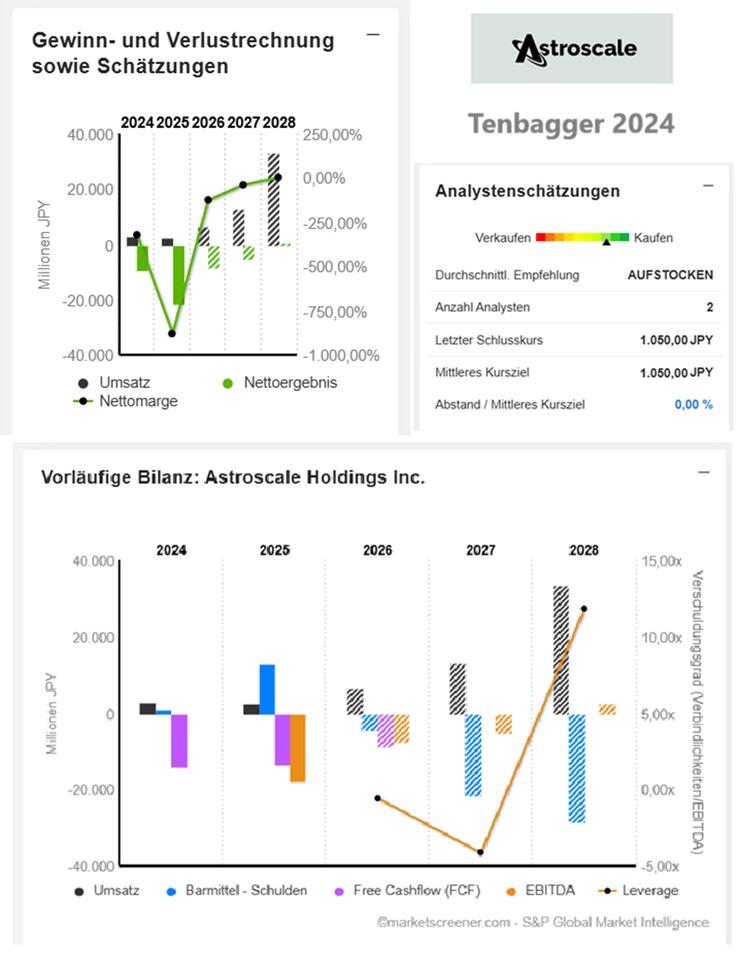

Year Turnover Change

2025 2.457 -13,85 %

2026 6.653 170,78 %

2027 13.026 95,8 %

2028 33.393 156,35 %

Year EBIT Change

2025 -18.755 -62,31 %

2026 -8.861 53,71 %

2027 -4.399 49,33 %

2028 1.500 134,1 %

Year Net result Change

2025 -21.552 -134,74 %

2026 -8.410 60,98 %

2027 -5.028 40,22 %

2028 700 113,92 %

Year Net debt CAPEX

2025 -12.775 696,8

2026 4.241 619

2027 21.479 1.040

2028 28.359 1.040

Year Free cash flow Change

2025 -13.295 4,98 %

2026 -8.786 33,91 %

Year EBIT margin ROE

2025 -763,34 % -373,9 %

2026 -130,49 % -118,36 %

2027 -33,6 % -74,85 %

2028 4,49 % -35,22 %

Year Earnings per share Change

2025 -188,9 -86,21 %

2026 -62,15 67,1 %

2027 -37,08 40,35 %

2028 5,15 113,89 %

Year P/E ratio PEG

2025 -4.09x -0x

2026 -16.9x 0.3x

2027 -28.3x 0.7x

2028 204x -2x

Market value 142,466

Number of shares (in thousands) 1,050.00

Date of publication 13.06.2025

Astroscale is since June 5, 2024 listed on the stock exchange.

PS. I have already seen an inquiry from you in the forum about @matsaz .

@Multibagger

@PikaPika0105

@Dividendenopi

@Klein-Anleger

@Get_Rich_or_Die_Tryin

@NichtRelevant All others

(Investments are not suitable for everyone, and mountains of risks)