Hello my dears,

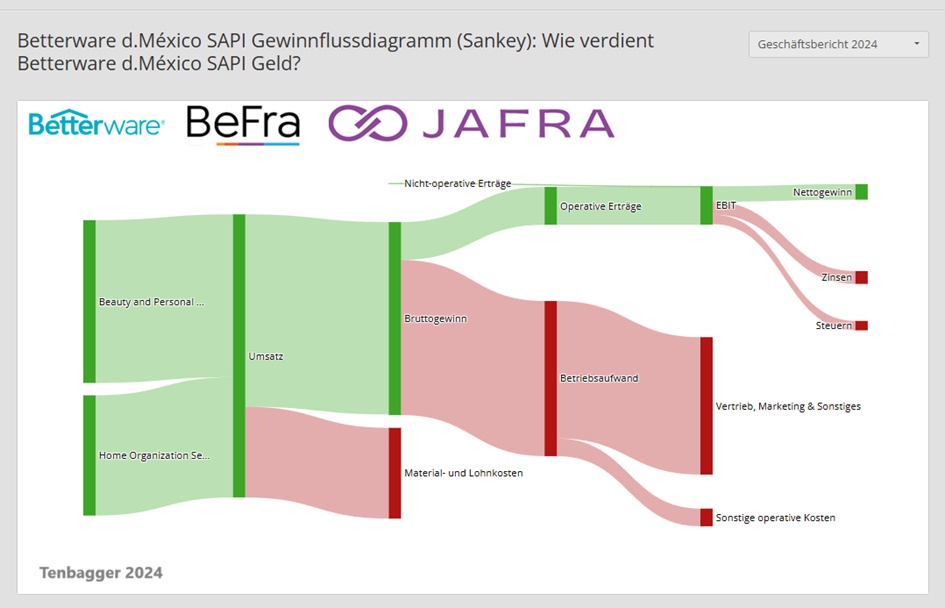

As I promised some of you, today there is a retail value with a double-digit EBIT margin.

But that's not the end of the story, and it probably won't satisfy some people either.

That is why there is another one:

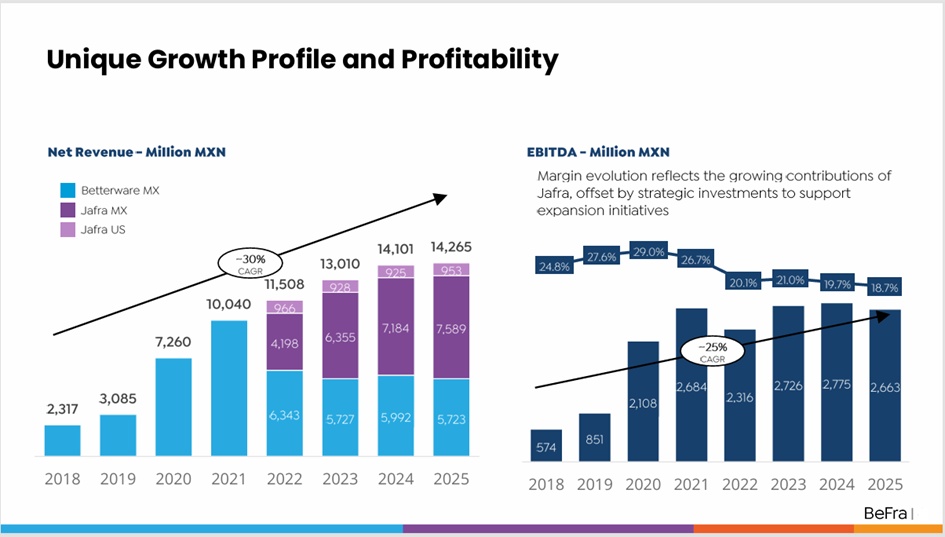

- double-digit sales growth

- Net profit grows by 56% this year

- Debt free

- P/E ratio below 10

- Dividend yield between 6-9 %

- Lots of potential through expansion into new markets (Latin America / USA)

My dears,

to find such a value for you, my search had to go as far as MEXICO to find such a value for you.

I look forward to many comments.

And have fun with Betterware de Mexico

Betterware de MexicoS.A.B. DE C.V. is a Mexico-based company that sells household appliances via an online portal. The company has a catalog that lists the company's various household products, including kitchen appliances, gardening tools and accessories for everyday use, as well as other categories. The company operates in all Mexican states, as Betterware's products reach every city in Mexico due to the strategic location of its production facility.

Number of employees: 2,595

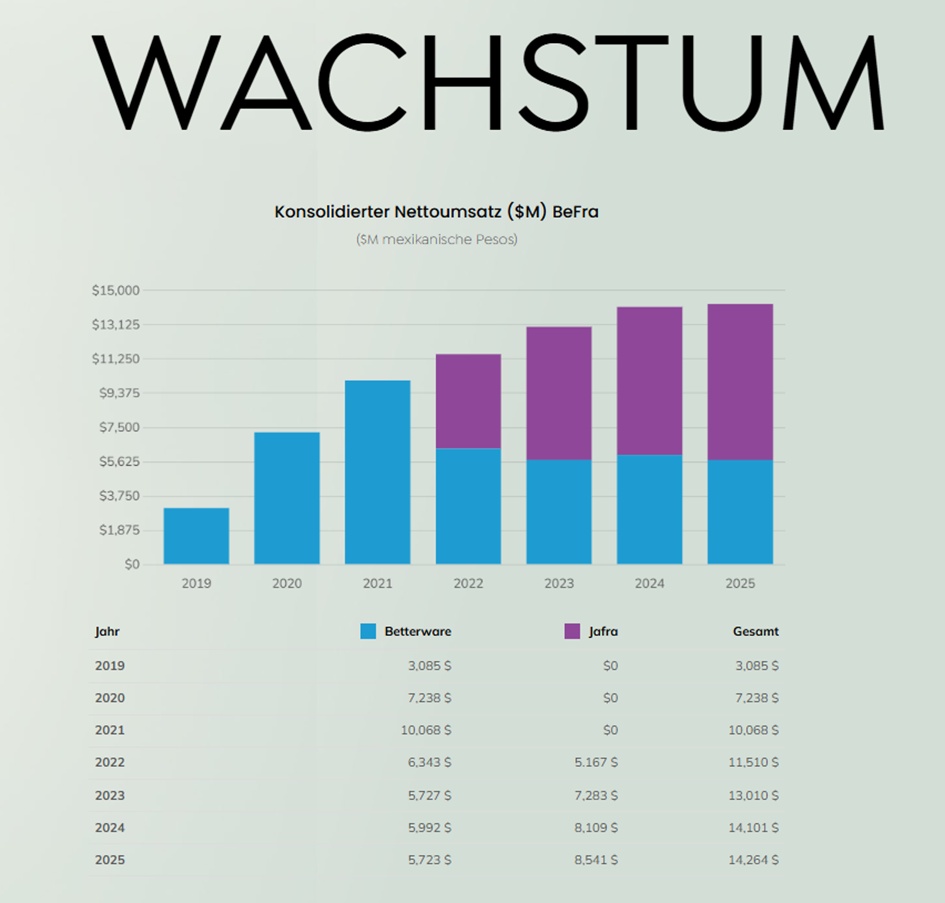

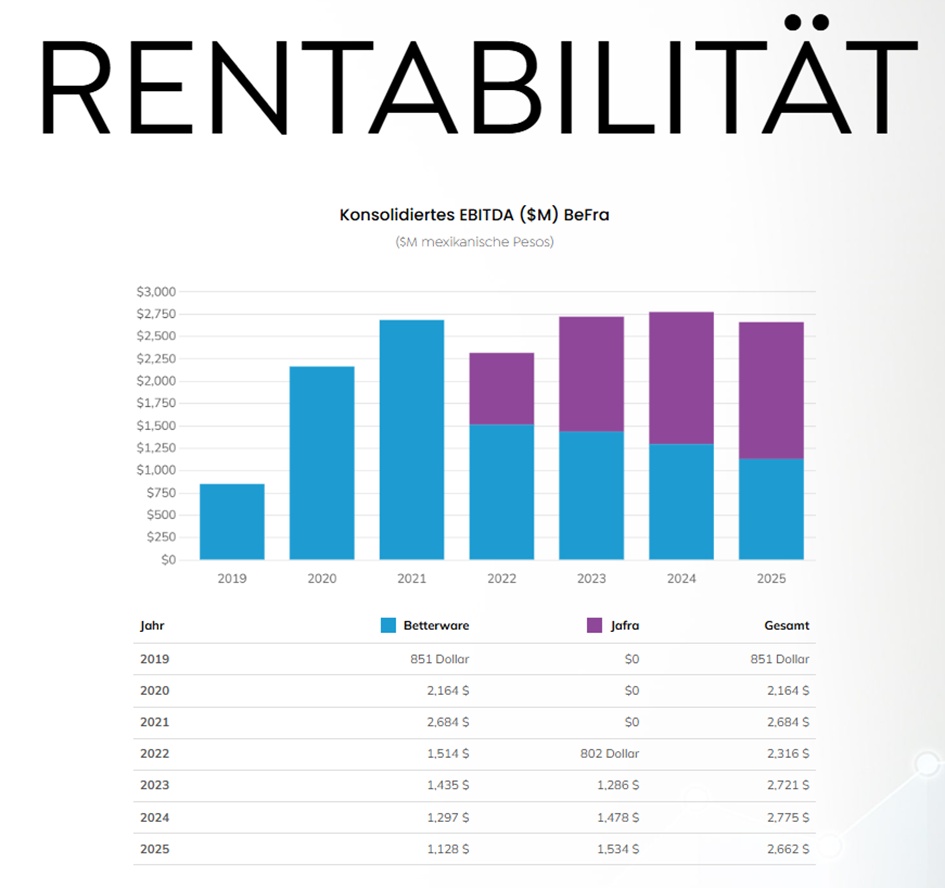

About BeFra

BeFra comprises the Mexico Group's leading direct selling brands, Betterware and Jafra. They offer a unique and wide range of products for every corner of the home through Betterware and beauty products through Jafra, with a combined network of 63,000 distributors and 1.13 million employees in Mexico and the US.

Their asset-light business model and state-of-the-art social selling platform enables their brand partners to create and build their own business by providing them with the best merchandising and digital tools as well as a broad portfolio of innovative products to create business opportunities. They work with a proven direct selling model through printed catalogs and digital social selling for both of their brands in Mexico and in the United States, where they also have an online presence.

- 2020 - Betterware de México is listed on the Nasdaq, becoming the first Mexican company to do so.

- 2022- Betterware de México acquires Jafra, expands its product portfolio to the beauty segment and gains access to the US market.

- 2024- Betterware de México establishes the new trade name, BeFra, consolidating the Group's brands under this corporate brand.

- 2024- Betterware launches operations in the United States, targeting the large and rapidly growing Hispanic population.

Betterware

Betterware is a leading direct-to-consumer company in Mexico focused on the home organization segment. In April 2024, we launched operations in the United States, targeting the large and fast-growing Hispanic population.

Mexico:

betterware.com.mx

United States:

betterware.com

Jafra

Jafra is a leading direct-to-consumer company in the beauty industry with a strong presence in Mexico and the United States.

Mexico:

jafra.com.mx

United States:

jafra.com

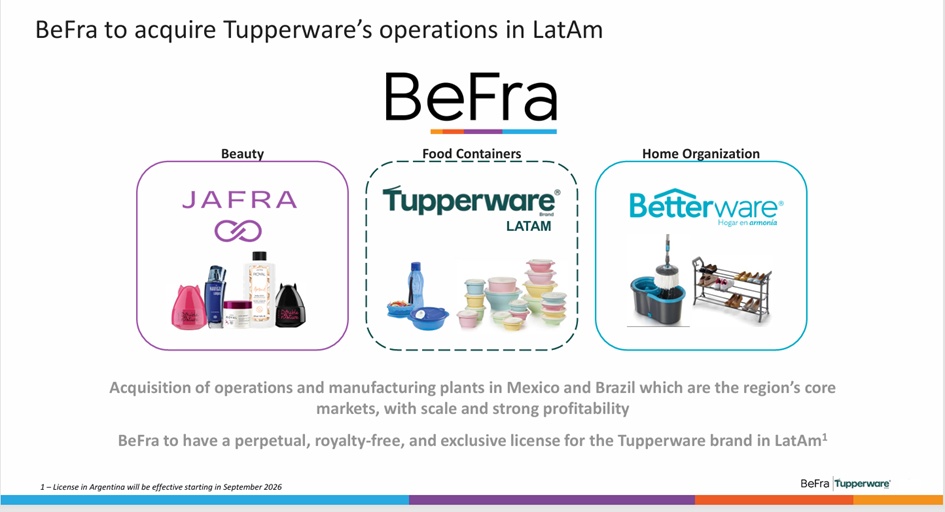

BeFra to acquire Tupperware businesses in Latin America

Products Betterware

Products JAFRA

JAFRA.com: Kosmetik, Hautpflege, Spa und Parfüm – Jafra Cosmetics International

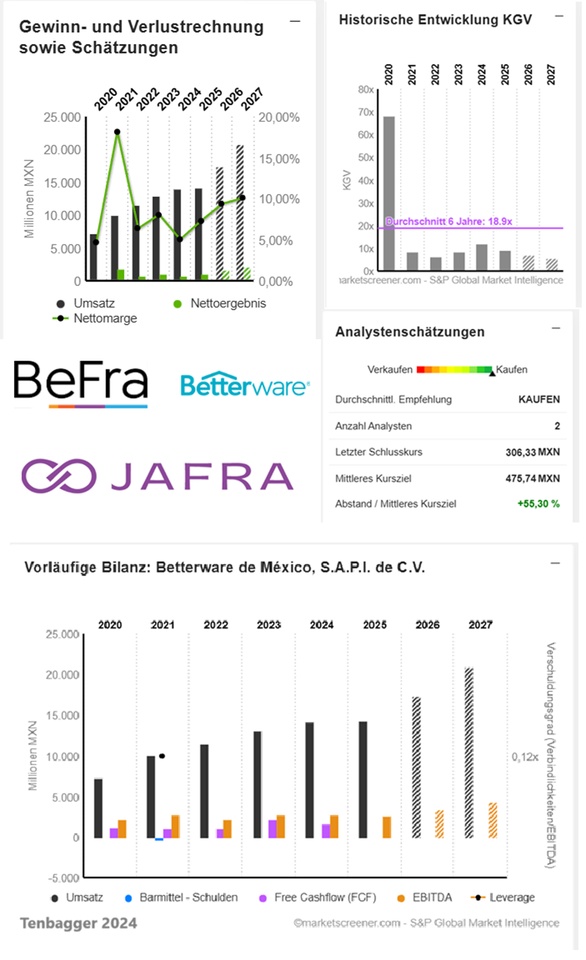

MXN in millions

Estimates

Year Sales Change

2024 14.101 8,39 %

2025 14.265 1,16 %

2026 17.401 21,98 %

2027 20.862 19,89 %

Year EBIT Change

2024 1.686 -28,12 %

2025 2.273 34,81 %

2026 2.964 30,38 %

2027 3.880 30,9 %

Year Net result Change

2024 711,7 -32,18 %

2025 1.043 46,51 %

2026 1.633 56,56 %

2027 2.104 28,89 %

Net debt not available

Year Free cash flow Change CAPEX

2023 2.236 101,18 % 131,1

2024 1.601 -28,37 % 222,3

2025 1.977 23,45 % 116

Year EBIT margin EBITDA margin

2024 11,96 % 19,68 %

2025 15,94 % 18,67 %

2026 17,03 % 19,31 %

2027 18,6 % 20,82 %

Year Earnings per share Change

2024 19,07 -32,38 %

2025 27,94 46,51 %

2026 42,17

2027 53,45 26,76 %

Year P/E ratio PEG

2024 12.2x -0.4x

2025 9.16x 0.2x

2026 7.26x -0.5x

2027 5.73x 0.2x

Market value 11,409

Number of shares (in thousands) 37,244

Date of publication 26.02.2026

@Get_Rich_or_Die_Tryin

@Raketentoni

@Dividendenopi

@Max095

@Klein-Anleger

@Multibagger

@Liebesspieler

@SAUgut777