Once again, we dug deep into the Scandinavian soil and found what we were looking for - off the beaten track - in Finland.

I like to present the values that correspond to my formulas and investments, but today we are making an exception for our growth friends.

Finland is often criminally neglected. For many, Scandinavia ends in Stockholm, but those who dare to take the leap across the Baltic Sea will find a "deep tech" scene in Helsinki that is unparalleled worldwide. Today we have a company in our luggage that is not a "boring" dividend stock, but a genuine growth story that is deeply rooted in the DNA of global chip production. We will be unearthing more of these Finnish specialists over the next few weeks - but $LL1SPAC (+5.41%) Canatu kicks things off today.

⚠️ Important note: The "ticker chaos" & the two papers

Before you jump in, you need to pay attention. Since Canatu was acquired through a merger with Lifeline SPAC I you will find two different securities with many brokers:

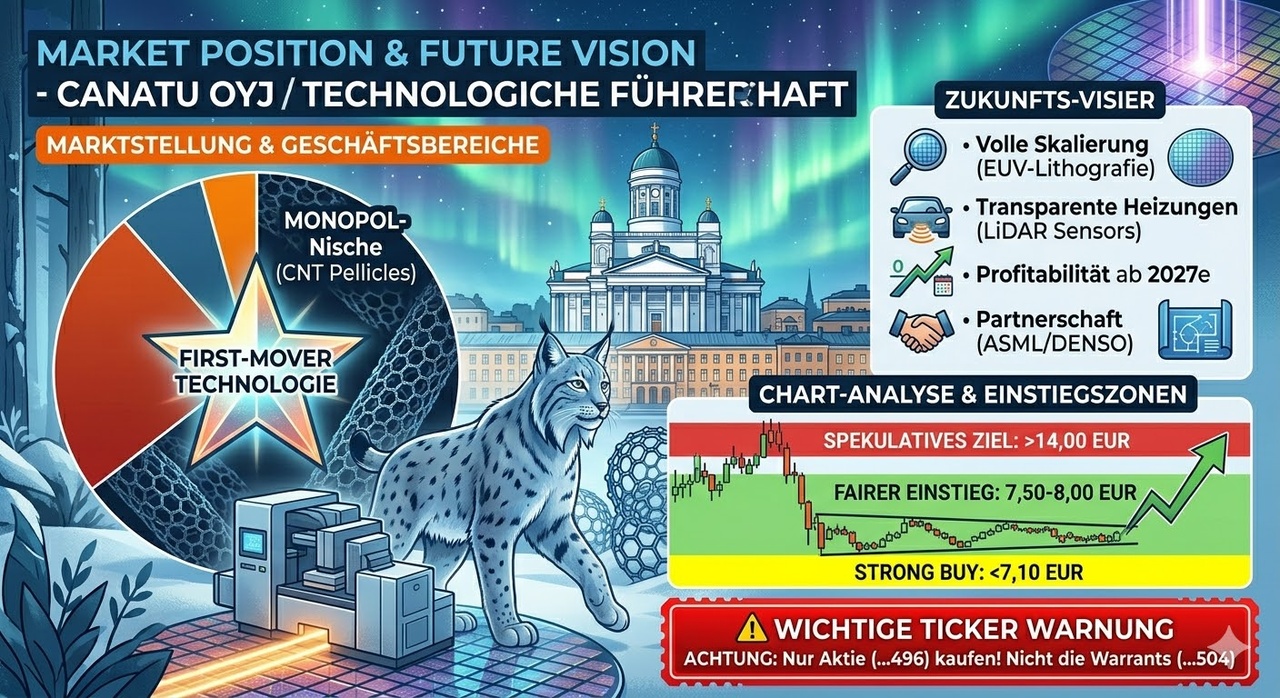

The share (Series A): Ticker: CANATU | ISIN: FI4000512496. This is the security we are analyzing here. It represents the direct ownership of the company.

The warrants (warrants): Ticker often CANATU1W | ISIN: FI4000512504. These are pure call options that give the right to buy shares at a fixed price at a later date. Caution: These are highly speculative and have a completely different risk profile. Please only buy the share (ISIN ends in ...496).

1. the business model: What does Canatu do?

Canatu $LL1SPAC (+5.41%) produces the cleanest carbon nanotubes (CNTs) in the world. Their membranes are so pure that they are used in EUV (extreme ultraviolet) lithography to protect the sensitive photomasks from dust. Without this technology, there would be no modern 2nm or 3nm chips. They also build transparent heaters for sensors in autonomous cars.

2. market position: the ASML enabler

Canatu is not a competitor to the major chip manufacturers, but their enabler. They are a key partner of ASML. The new generation of exposure machines ("High-NA") requires Canatu's technology in order to cope with the enormous heat development. This niche is hard to ignore if you want to make progress in semiconductors.

3. key figures (as of March 21, 2026)

4. core quality formula check

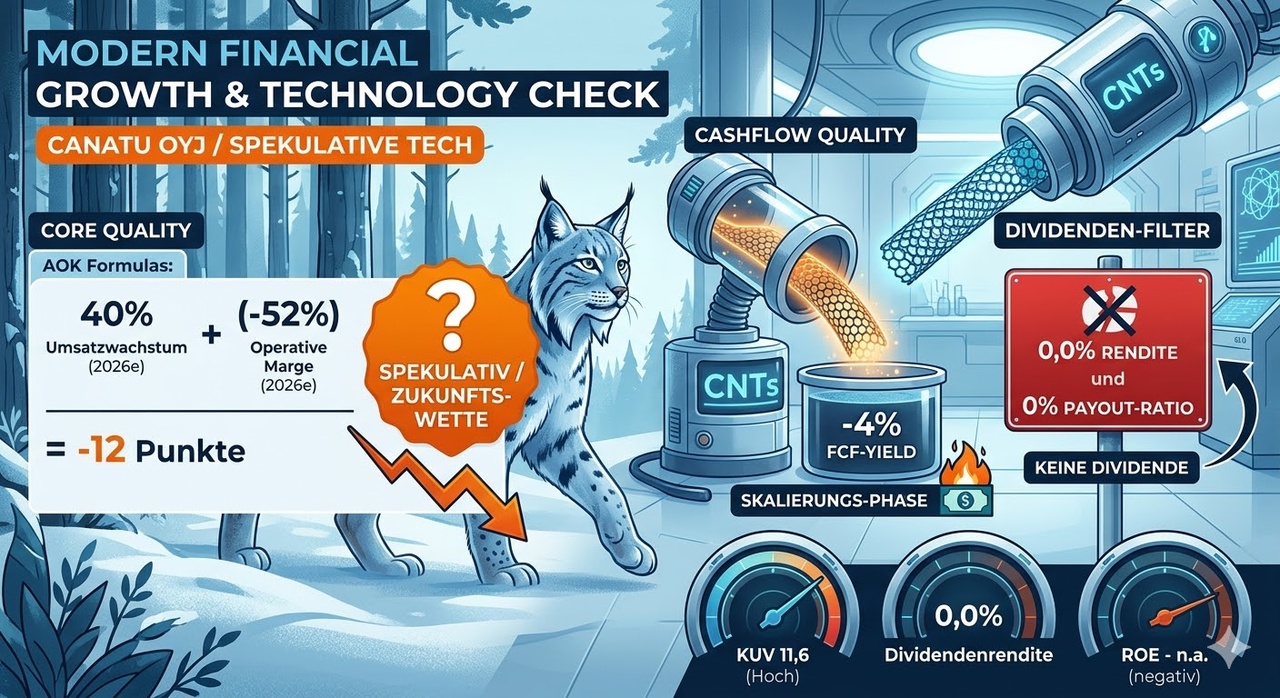

Your filter: Sales growth (%) + Operating margin (%) = Score.

- Sales growth: ~ +40% (Expected for the 2026 ramp-up)

- Operating margin: -52 % (still strongly negative due to R&D and scaling)

- Result: $40 + (-52) = 12

- Verdict:

Speculative. My formula is sounding the alarm here, as profitability is still lagging behind the story. It is a classic "future winner", not a value stock.

5. cash flow quality formula

- Free cash flow: Currently still negative (~ EUR -10m annually).

- FCF yield: Negative.

- Verdict: The company is living off capital increases and the reserves from the SPAC deal. Break-even is targeted for 2027/28.

6. dividend filter

- Verdict:

Failed. Canatu reinvests every euro in the factories.

7. future prospects & strategy

On March 26, 2026 the Capital Markets Day (CMD) is scheduled. Here, the management will explain how they are moving from pilot production to mass production for the automotive industry (with partner DENSO). This is the catalyst the market is waiting for.

8. competition & substitutability

There is hardly any competition that can produce carbon structures of this industrial purity. Substitutability is low, as ASML and other partners have calibrated their processes to Canatu materials for years (high switching costs).

9. chart analysis (last 6 months)

The share has undergone a painful correction. From highs of EUR 13.00 it has fallen to EUR 7.50 after short-term targets for 2025 were adjusted. We now see a bottom forming. The RSI indicates an oversold condition - technically an exciting rebound candidate.

10th Bargain Hunter's List

- Strong Buy: < EUR 7.10 (all-time low protection).

- Fair entry: EUR 7.50 - 8.00 (Before the CMD on March 26).

- Speculative target: > 14.00 EUR (If scaling is successful).

11. profit margins & outlook

In the long term, margins of over 20-25 % are possible as soon as the fixed costs of the factories are covered by high volumes. The upside potential is enormous, but so is the risk.

12 My perspective: Viability

Canatu is the "salt in the soup" for a depot. It is not a basic investment, but it is so deeply rooted technologically that a total failure is unlikely as long as the chip industry continues to grow. The story is great, but the figures must now be delivered at the CMD in March.

Bottom line:

Canatu is the perfect example of what we are looking for in the far north: Companies that are so technologically deep in global supply chains that it's hard to ignore them if you want to understand the future. Yes, the chart looks wild and "broken" at first due to the SPAC past, but if you analyze the 1.5 years since the merger closely, you will see a company that is just getting warmed up.

We'll stay tuned - Finland has more secrets like this in store for us.

As always, we welcome your opinions:

@Multibagger

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Stocktective

@Simpson

@Abyss

@NichtRelevant

@SAUgut777

@Klein-Anleger

@TradingHase

@WarrenamBuffet

@Keineui

@schlimmschlimm