You can only pick ONE portfolio for the next decade, which are you taking?

Portfolio A

Portfolio B

Portfolio C

Posts

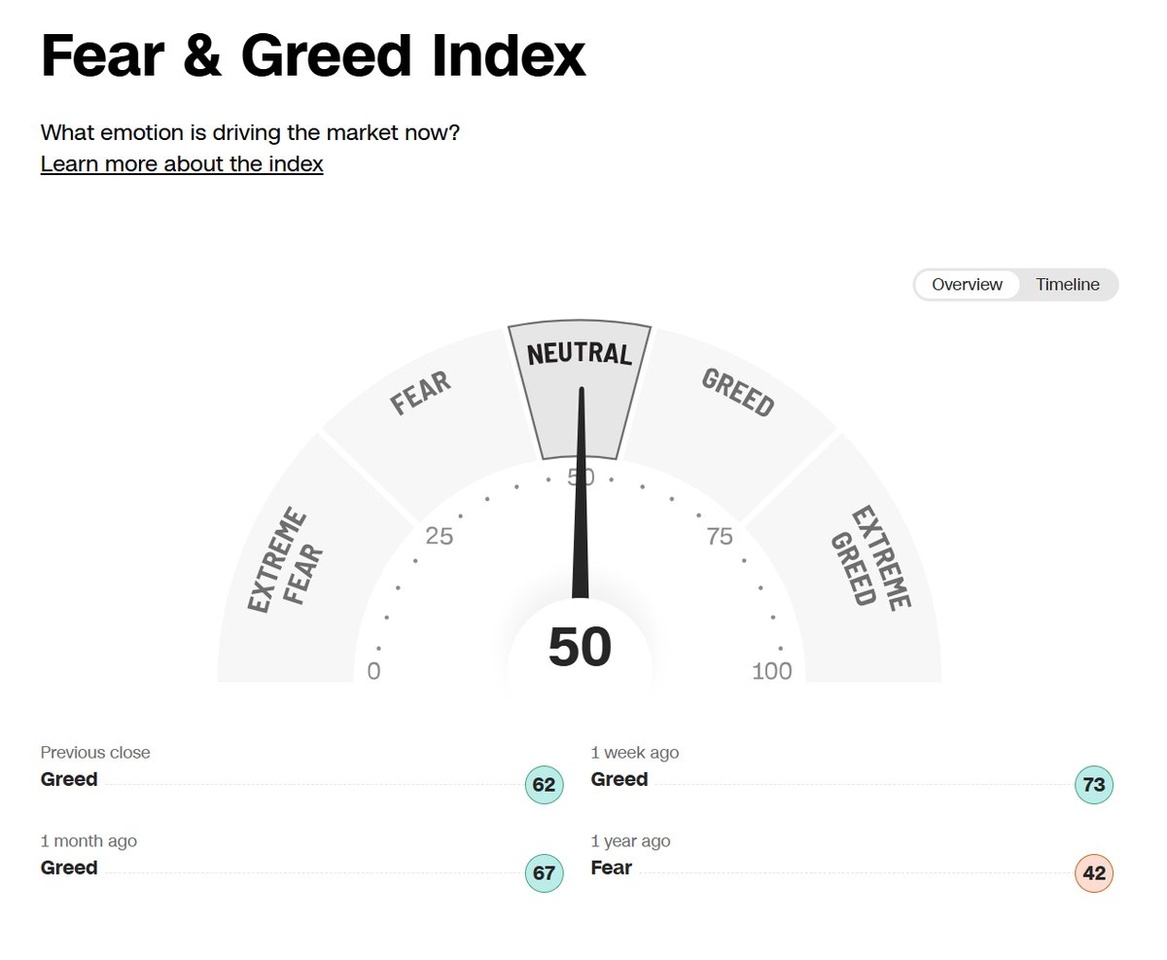

103Negative news is piling up again and market sentiment cooled down a little in August:

"Brace for a crash before the golden age of AI." - Financial Times

"Is the AI bubble about to burst - and send the stock market into freefall?" - The Guardian

Some people are thinking:

"The market MUST crash soon! What do I do now? Maybe I'd better sell everything?"

If you hold highly valued individual shares such as $PLTR (+2.01%) such thoughts may quickly rob you of sleep.

(Yes, the bull in the picture has a Palantir logo on his chest and is running towards a cliff 😘)

Others remain calmly on autopilot and continue to save in their ETF portfolio and look forward to opportunities for extra purchases in the crash.

And those who follow strict rules (momentum à la @Epi ) are hardly affected by "doom & gloom" headlines anyway.

The widely known truth is, of course:

🤷♂️ Nobody knows what the market will do tomorrow.

👉 But: There are macro signals that in the past have frequently have often flashed before major drawdowns. Not perfectly, not always, but often enough to keep an eye on them.

I have built a TradingView indicator from them:

_____________________

Big Mo's crystal ball 🔮

The glass ball bundles several US macro indicators into a single risk oscillator (0-100), colors the line smooth from green → orange → red and marks "yield curve re-steepen warning window" discreetly in the background.

🤡 I see the indicator more as a "fun experiment" than as a serious tool.

Just take a look, duplicate the code and play around with the numerous settings (see FAQ below).

👉 Link to the indicator:

https://www.tradingview.com/script/EWH6Gvcw-Big-Mo-s-Glaskugel-Macro-Drawdown-Risk-v1-1-2/

📍What's inside? (short & crisp)

Inversions are well known - my twist: re-steepening (the jump back above 0 after an inversion). This signal has often been the more useful harbinger of stock market stress.

When Baa spreads shoot well above their 12-M average → Risk-On → Risk-Off transition.

Weak Leading Economic Index (6-month rate) = economic headwind.

High valuation ≠ immediate crash, but increases downside risks.

Sudden spikes in volatility are "boosted" in the score.

⚠️Wichtig:

This is not an oracle or a guarantee of anything.

They are warnings, not commands.

💡Nevertheless:

These are precisely the factors that have made various large declines conspicuous before (dotcom, GFC, 2020 etc.).

⁉️Was do you see on the chart?

Example:

Here I have the first "yield curve re-steepener" in the red⚡HIGH risk zones on the chart of the $SPY (+0.13%) marked.

This shows you where the indicator would have "released" you from the market with today's hindsight bias. 😏

Why not in the 2022 bear market? 🤷♂️

💬FAQ

What is the crystal ball good for?

To visualize macro risk in a compact form. Not a timing tool for the next 5-minute trade, but a possible early warning radar.

For which market is this optimized?

For the US market. All data sources are US macro series.

No matter which chart you load (stock, ETF, crypto): The data remains US macro. It's best to look at the SPX/SPY. If it collapses, practically everything else goes with it anyway...

I have activated the indicator on stock XY. Why wasn't the crash "predicted" there?

Because the crystal ball measures the macro perspective, not the idiosyncratic risk of an individual stock. Company news can move the stock regardless of the macro picture.

Which timeframe?

Recommendation: 1W (The underlying series come in D/M from FRED/MULTPL anyway).

Is it possible to see the measured values in the panel when hovering a point in time?

Unfortunately not. This is a limitation of Pine Script.

Which settings can I customize?

Is THe FiNaNciAL AdVicE? 😱

No. No recommendation, no guarantee. Use it as context and combine it with your own research & risk management.

Build a portfolio with a STRONG FOUNDATION

ETFs are the easiest way to do this

$SPY (+0.13%) S&P 500

$QQQ Invesco QQQ

$VTI (+0.05%) Vanguard Total Market

$DGRW WisdomTree Div Growth

$SCHD Schwab US Dividend Equity

I still remember a conversation I had years ago with a new trader who was proud of his first big investment.

He told me, I just bought the S&P 500 ETF because I heard it’s the best index fund in the world.

I asked him, Do you know the difference between an ETF and an index fund?

He smiled and said, Aren’t they totally different things?

That’s when I realized, this confusion isn’t just for beginners. Even people already putting money to work often don’t fully understand what they’re buying. And in this business, what you don’t know can hurt you.

So here’s how I broke it down for him, the same way I’d explain it to anyone on the trading desk.

1. First, what’s an index?

An index is nothing more than a list. It’s not a product you can buy directly, it’s a benchmark that tracks the performance of a specific group of securities.

Examples:

• S&P 500 – 500 large U.S. companies, market-cap weighted.

• Nasdaq-100 – 100 largest non-financial stocks on Nasdaq.

• Russell 2000 – 2,000 small-cap U.S. companies.

Indices are rules-based. They have strict criteria for what’s included, how it’s weighted, and how often they’re rebalanced.

2. What’s an index fund?

An index fund is simply a pool of investor money that tries to copy the performance of a specific index.

It owns the same securities, in the same weights, as the index.

Two main formats:

• Mutual Fund Index Fund – Trades once a day at the end-of-day NAV (Net Asset Value). You can’t trade it intraday.

• ETF Index Fund – Trades like a stock all day long with real-time prices.

The big “aha” moment for most people is:

➡ An ETF can be an index fund, and an index fund can be an ETF. “Index fund” describes the strategy, “ETF” describes the structure.

3. Why traders love ETFs

For active traders and tactical investors, ETFs have major advantages:

• Intraday Trading – Enter and exit positions whenever the market is open.

• Tight Spreads – In heavily traded ETFs like $SPY (+0.13%) or $QQQ, spreads are often just a penny wide.

• Options Access – You can trade calls, puts, spreads, and hedges on many ETFs.

• Tax Efficiency – Thanks to the in-kind creation/redemption process, ETFs often avoid triggering capital gains distributions that mutual funds pass on to investors.

4. The hidden plumbing | creation/redemption

Most people never see this, but it’s what keeps ETFs functioning properly.

Large institutions called Authorized Participants (APs) create or redeem ETF shares by exchanging baskets of the underlying securities.

• If ETF prices drift above the value of the underlying assets, APs create new shares and sell them into the market, pushing the price back down toward fair value.

• If ETF prices drift below NAV, APs buy ETF shares in the market and redeem them for the underlying assets, pushing the price back up.

This constant arbitrage keeps ETFs trading very close to their NAV.

5. Advanced concepts & risks to understand

• Synthetic ETFs – Instead of owning the actual stocks, these use derivatives (like swaps) to mimic an index’s return. This can expose you to counterparty risk if the swap provider fails.

• Leveraged & Inverse ETFs – Designed for daily performance multipliers (2x, 3x) or the opposite (-1x, -2x, -3x) of an index. Over time, compounding and volatility decay can produce returns far different from what you expect. Great for short-term tactical plays, risky for long-term holding.

• Tracking Error – No ETF tracks its index perfectly. For large, liquid ETFs, the difference is tiny. For niche or illiquid markets, it can be much larger than you think.

• Liquidity & Spreads – Always check trading volume and spreads. A low-volume ETF might have a spread big enough to eat into your returns before you even get started.

6. How pros choose between ETFs and mutual funds

• Use ETFs if you want flexibility, options trading, lower minimum investments, or intraday control.

• Use mutual funds if you’re dollar-cost averaging in a retirement account, prefer automatic investments, or don’t need intraday pricing.

7. Real-world example

Want S&P 500 exposure?

• SPY (ETF) – Trades all day, ultra-liquid, optionable, small tracking error.

• VFIAX (Mutual Fund) – Same holdings, but only trades at end-of-day NAV, requires minimum investment, ideal for long-term retirement accounts.

Both are index funds. The difference is how they trade and fit your plan.

8. The biggest beginner mistakes

• Holding leveraged ETFs long-term thinking they’ll just go up faster.

• Buying low-volume ETFs without realizing spreads eat into returns.

• Owning synthetic ETFs without understanding the counterparty risk.

• Confusing the index itself with a tradable product.

Quick Reference Cheat Sheet (screenshot this)

• Index = List of securities (not tradable).

• Index Fund = Fund that tracks an index (can be mutual fund or ETF).

• ETF = Fund traded like a stock (can track an index or follow another strategy).

• Leveraged/Inverse ETFs = Short-term tactical tools, not long-term holdings.

• Synthetic ETFs = Use derivatives, have counterparty risk.

• Tracking Error = Difference between ETF performance and its index.

That new trader I spoke to years ago? He still owns ETFs today, but now he knows exactly why he’s using them, how they work behind the scenes, and which ones to avoid.

In this game, the right tool in the wrong hands can be dangerous… but the wrong tool in the right hands is worse.

Understand what you own, and you’ll trade and invest with confidence instead of luck.

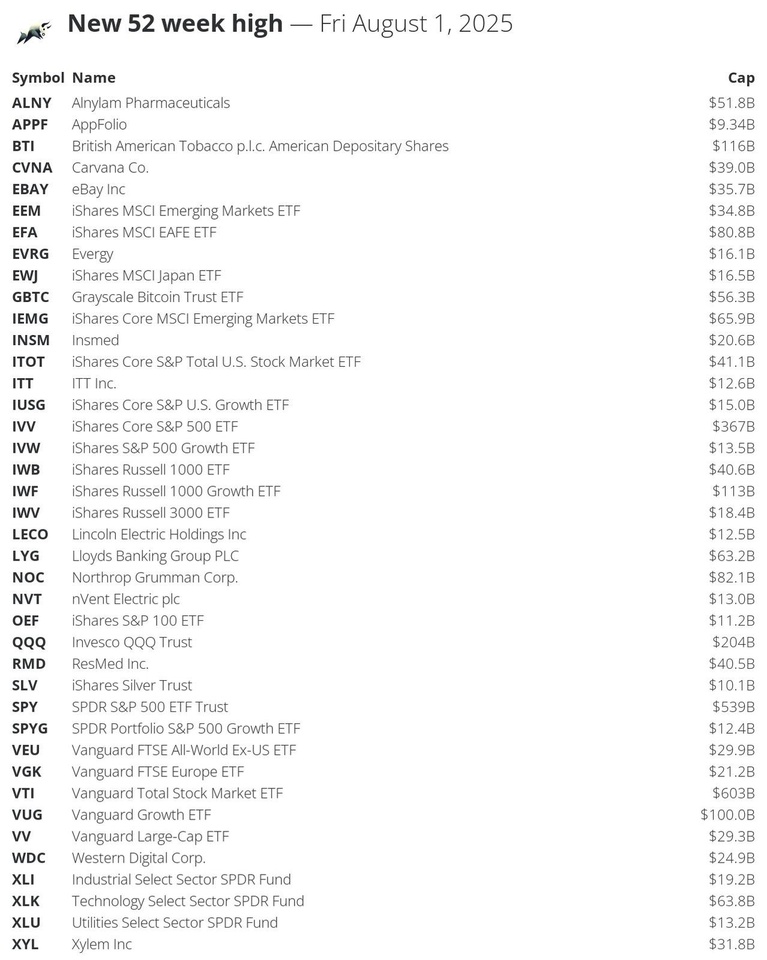

🔝 Stocks that made a new 52-week high today: $VTI (+0.05%)

$SPY (+0.13%)

$IVV (+0.12%)

$QQQ

$BTI (+2.29%)

$IWF (-0.02%)

$VUG (-0.08%)

$NOC (+1.99%)

$EFA

$IEMG (-0.1%)

$XLK

$LYG

$GBTC

$ALNY (+1.54%)

$ITOT (+0.06%)

$IWB (+0.11%)

$RMD (+1.17%)

$CVNA (+0.47%)

$EBAY (+2.25%)

$EEM

$XYL (-0.72%)

$VEU (-0.27%)

$VV (+0.14%)

$WDC (-4.08%)

$VGK (-0.23%)

$INSM (+2.96%)

$XLI

$IWV (+0.05%)

$EWJ (-0.99%)

$EVRG (+1.12%)

$IUSG

$IVW

$XLU

$NVT

$ITT (-0.65%)

$LECO (+0.5%)

$SPYG

$OEF (+0.24%)

$SLV

$APPF (-1.15%)

#52weekHigh

Bought the dip on Liberation, but since $MSFT (-0.4%) is a very big Position in $SPY (+0.13%) which I am DCAing for awhile and trying decrease my exposure to US overall thought it is time to already say good bye Microsoft.

It wasn't an easy decision but a necessary one.

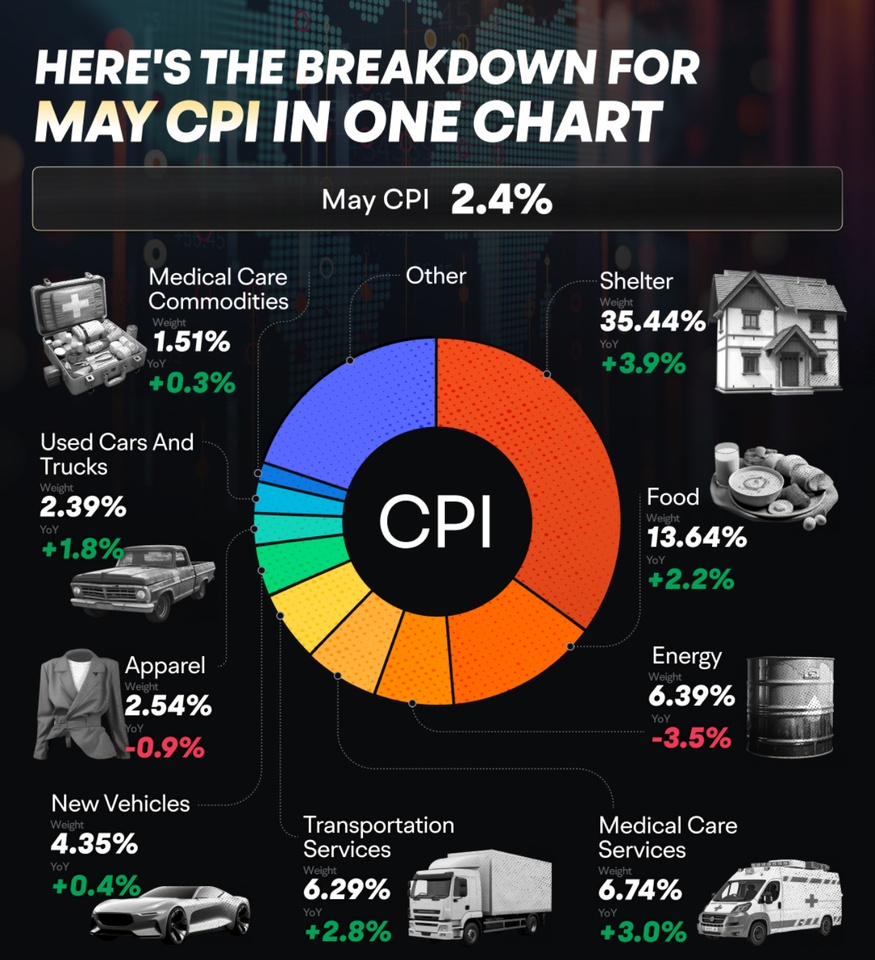

The CPI US Consumer Price Index rose to 2.4% in May 2025 for the first time in four months, up from a low of 2.3% in April 2021, although it was below the expected 2.5%. On a monthly basis, the CPI rose by 0.1%, which was below both the previous month's figure of 0.2% and the expected 0.2%.

Food prices rose by 2.2% year-on-year, following an increase of 2.8% in the previous month. Energy costs fell by 3.5% year-on-year, following a fall of 3.7% in April. Energy prices fell by 1.0% on a monthly basis.

Prices for used cars and trucks rose by 1.8% year-on-year, following a rise of 1.5% in the previous month. Housing costs rose by 3.9% year-on-year, following an increase of 4.0% in April.

The annual core inflation rate, which excludes the volatile food and energy sectors, remained steady at 2.8%, the lowest level since 2021 and below the expected increase to 2.9%. The monthly core CPI also rose by 0.1%, but remained below the 0.2% in April and the expected 0.3%.

$DAX

$NDAQ (+0.93%)

$SPY (+0.13%)

$NVDA (+0.07%)

$BTC (-1.9%)

$MSFT (-0.4%)

$SPY (+0.13%) $SPX 1H: MA cross on radar, but volume’s quiet. 5,950 resistance key—needs to reclaim fast or risks 5,900 support

Top creators this week