The other day we were talking with@Keineui about freenet. Today I decided to do a longer post about it.

This is what the algorithm says:

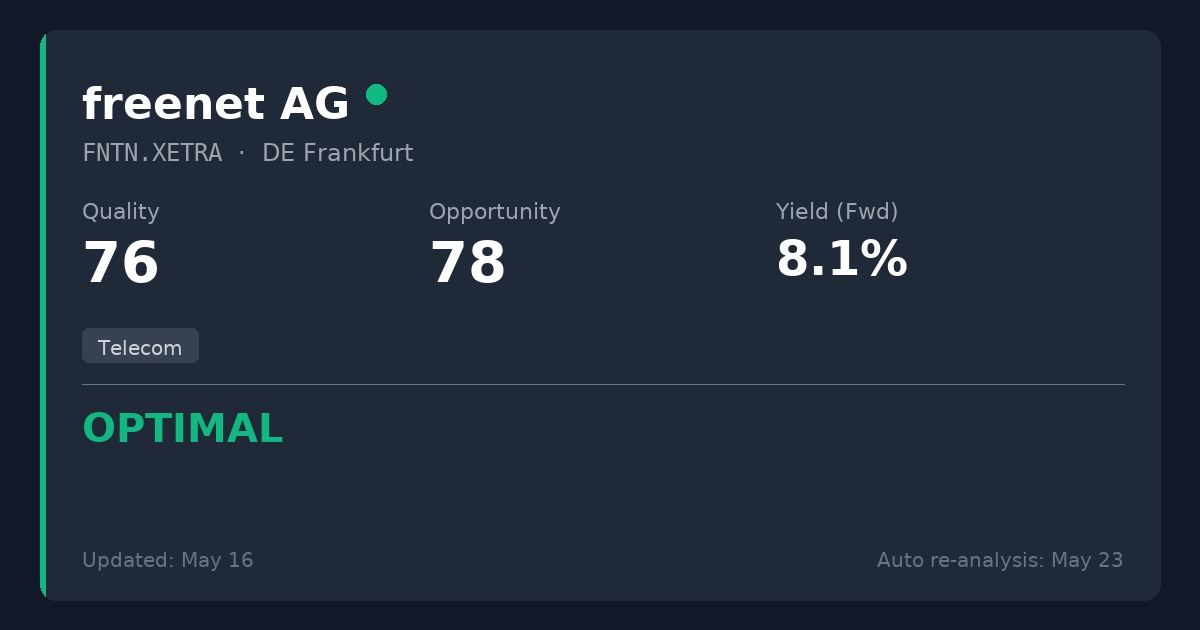

🇩🇪 freenet AG ($FNTN (-0,68%) )

🟢 OPTIMAL (Quality 75 / Opportunity 80)

• Current Yield: 7.8%

• Valuation: 8.0x P/FFO (Price to Funds from Operations)

Solid business at an attractive price.

This is what could look problematic at first glance:

• A scary 93% payout ratio based on classic accounting earnings.

• Top-line revenue historically looks stagnant.

• Short-term market noise and analyst downgrades regarding their wholesale network contracts.

This is why we like it:

🧠 The Capital-Light Advantage

Freenet operates a Mobile Virtual Network Operator (MVNO) model. They don't spend billions building physical cell towers—they just rent capacity. Because of this, their accounting earnings (EPS) are heavily suppressed by non-cash charges. Their true ability to generate cash is totally disconnected from their accounting noise.

💰 Cash Flow tells the real story

If we look past the 93% GAAP payout ratio and look at what really matters—Free Cash Flow—we find a highly secure 58% payout ratio. The 7.8% dividend is perfectly safe and easily covered by the actual cash they print.

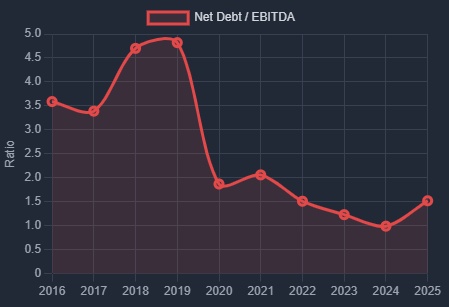

🛡️ Aggressive Deleveraging

Far from being in distress, their balance sheet is pristine. Over the last decade, they have crushed their Net Debt / EBITDA from 3.6x down to a very safe 1.1x today. They used their cash machine to pay down debt perfectly.

(plot from dividendquad , data provided by EODHD)

⚖️ The Valuation Opportunity

The market is currently pricing the stock based on short-term uncertainty around wholesale network renewals, leaving FNTN trading at a severely depressed 8.0x P/FFO.

The Verdict:

What looks like an accounting problem on the surface is actually a perfectly healthy cash flow engine. It's a rare chance to lock in a massive 7.8% yield covered by Free Cash Flow, backed by a strong balance sheet, while we wait for the multiple to expand.