If you only look at the price trend, you will see a classic high flyer. If you dig a little deeper, you will see something else: a potential possible infrastructure bottleneck that is just beginning to become economically relevant.

For me, the development of $SIVE (+7,01%) well explained by two terms:

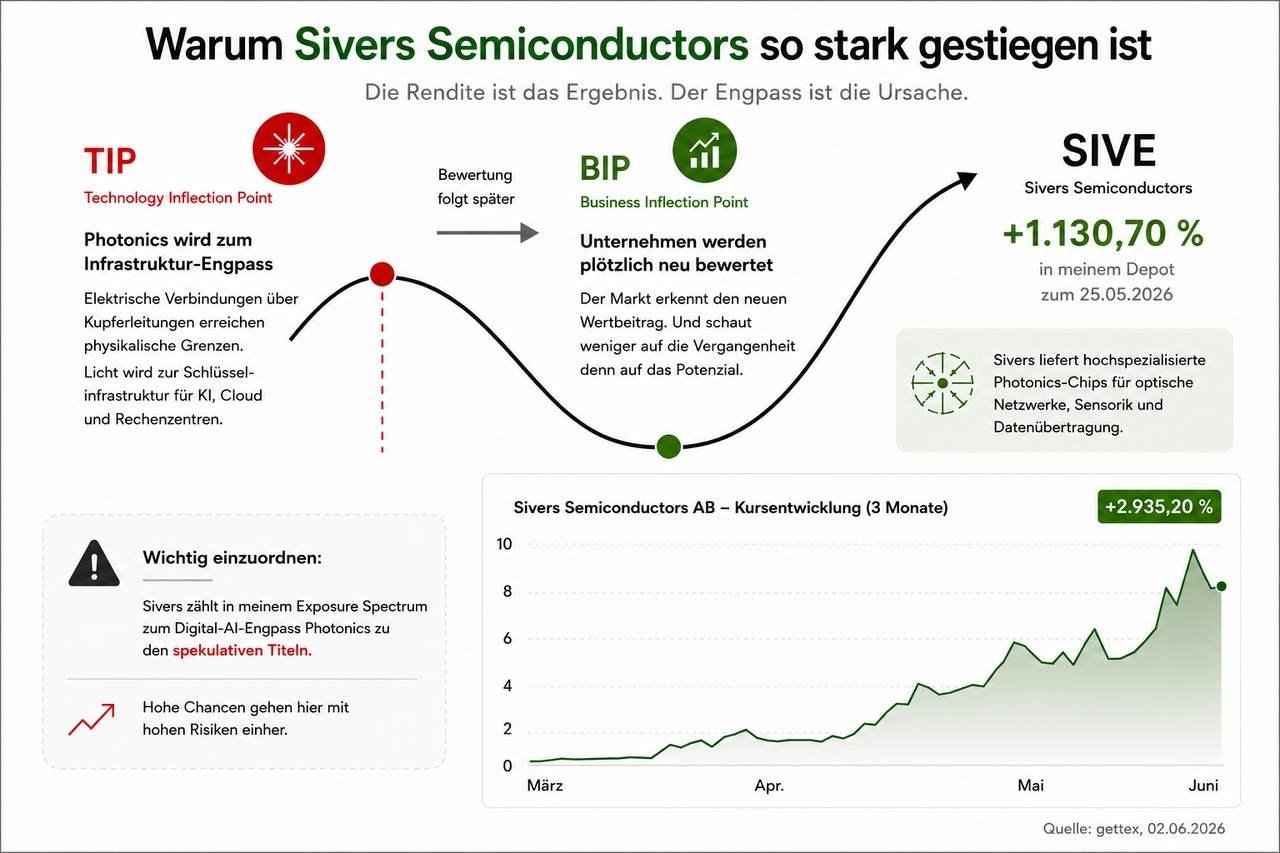

🔴 TIP = Technology Inflection Point

A technology inflection point occurs when a technology goes from being an interesting niche solution to a potentially indispensable infrastructure.

This could currently be the case with photonics could happen. AI systems are generating ever larger data streams. At the same time, electrical connections via copper are increasingly reaching their physical limits. Energy consumption, heat and signal losses are increasing.

This is why the industry is investing heavily in optical data transmission. Light instead of electricity. Photonics is therefore increasingly developing from a specialist topic into a potential AI infrastructure bottleneck.

🟢 GDP = business inflection point

The business inflection point often comes later. It occurs when companies suddenly benefit economically from this technological change. also benefit economically.

New orders.

New customers.

New sales potential.

New valuations.

A current example is the example is the collaboration between Sivers Semiconductors and GlobalFoundries that was announced today. This is interesting for me because such partnerships can show that a technology is finding its way out of the development phase and towards industrial scaling.

This is precisely the point at which a reassessment by the market. The market then looks less at the past and more at the question: "How big could this market become if the technology catches on?"

Nevertheless, it remains important that Sivers is still one of the speculative stocks in my exposure spectrum. speculative stocks in my exposure spectrum. The company is not an established infrastructure heavyweight like Coherent. It is much earlier in the cycle. The opportunities are therefore greater.

But so are the risks.

For me, Sivers therefore remains above all a bet that the current technology inflection point will eventually become a sustainable business inflection point.

After all, returns are rarely generated when everyone is convinced. They often arise when a new infrastructure bottleneck is just becoming apparent.

Incidentally, Sivers is also my driving force in the NextLimits wikifolio with a current gain of 822%.