Good morning,

Even in a tech correction as big as the one we experienced on Friday, our dear dividend investors remain completely relaxed.

Because the yield continues to flow nicely into their accounts.

So, somewhat unusually for me, I'm going to introduce you to a dividend stock today.

It's more in line with my expectations that the company will achieve growth in net income of 40% next year.

Of course, I also expect performance from this.

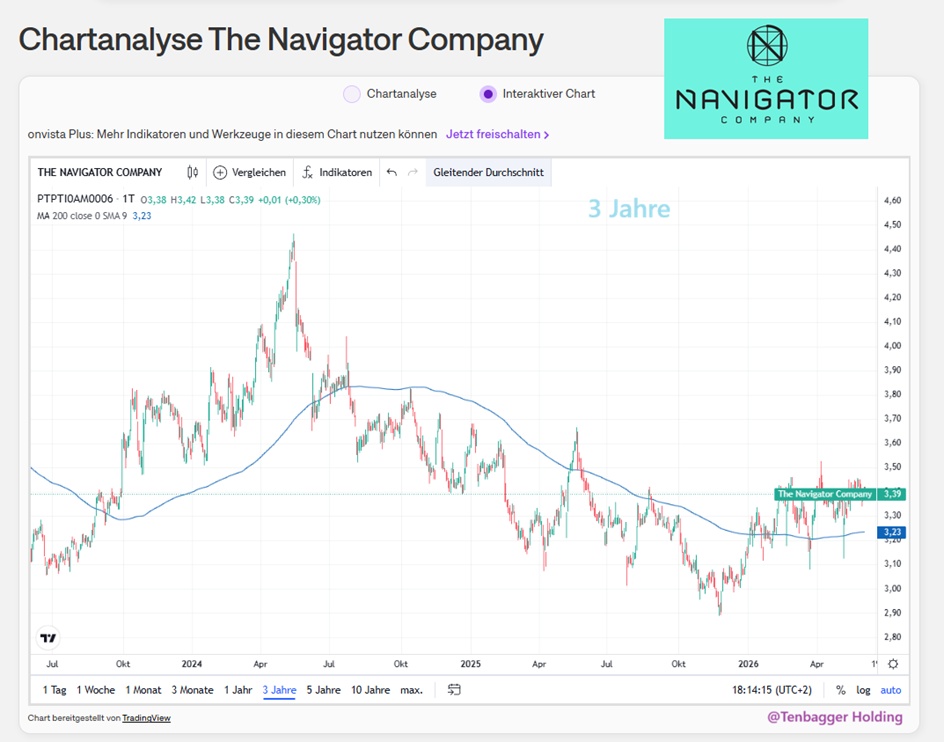

You can see from the chart that investors are slowly recognizing this.

My dears,

as I tend to deal less with dividend stocks. I am already very excited about what the expert and friend @Dividendenopi will say.

I am particularly looking forward to his assessment, but of course also to yours. And I hope for many comments.

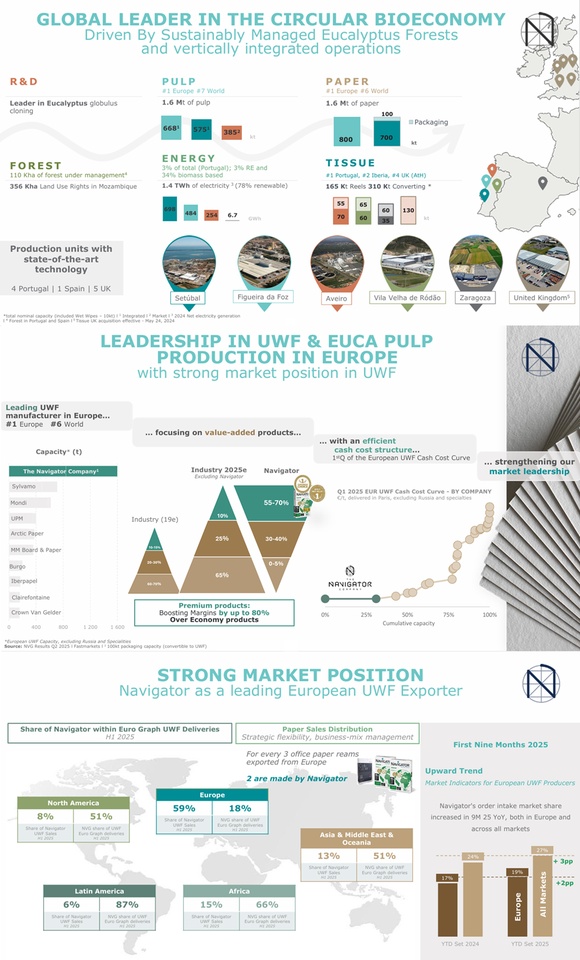

The Navigator Company is Europe's largest manufacturer of uncoated, wood-free paper.

It has a total capacity of 1.6 million tons of paper per year, a eucalyptus pulp capacity of 1.5 million tons per year (80% of which is integrated into paper) and produces 2.5 TWh of electricity per year.

The activities are located in four large-scale production plants, which are equipped with state-of-the-art technology and represent a quality benchmark in the sector. The Navigator Company manages 120,000 hectares of forest and is the largest eucalyptus nursery in Europe.

Navigator Company has an annual turnover of over 1.6 billion euros, its main markets are Europe (70%), Africa (9%) and North America (8%) and focuses on premium products and its own brands. Listed on Euronext Lisbon since 1995, Navigator Company has a majority shareholder, Semapa, with 69% of the share capital.

Navigator Company, S.A. is a leading European manufacturer of printing paper. Net sales break down by business segment as follows:

- Production of printing paper (61.5%): 1,297 kt sales in 2025 (Navigator, Inacopia, Discovery, MultiOffice, Inacopia brands, etc.);

- Tissue paper sales (24.6%): 231 kt sold;

- Production of eucalyptus pulp (8.9%): 347 kt sold;

- Other (5%): mainly electricity generation from biomass and production of forest products.

The geographical breakdown of net sales is as follows: Portugal (13.2 %), Europe (59.2 %), America (10.2 %), Africa and Middle East (10 %) and Asia (7.4 %).

Number of employees: 3,932

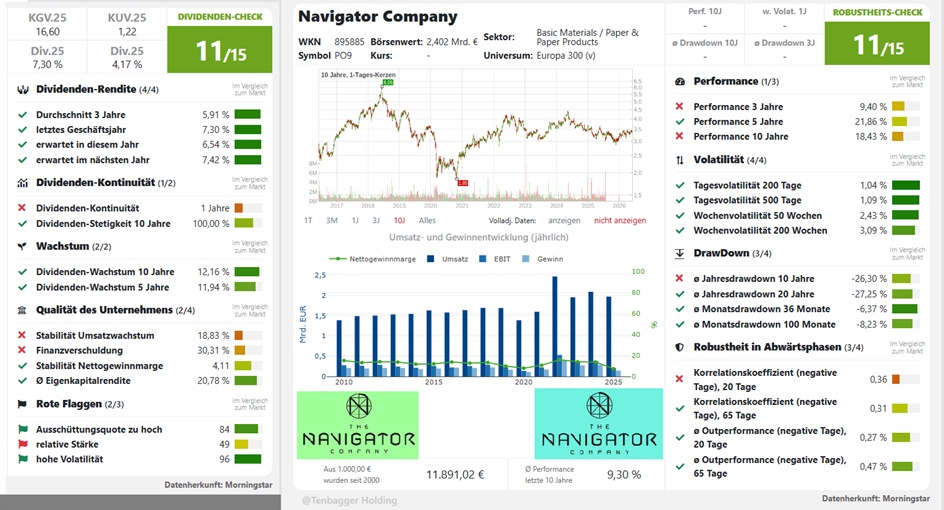

🧭 Why Navigator tends to be more stable than many cyclicals

1. business model with basic needs Navigator produces paper, pulp, tissue and increasingly packaging (gKRAFT™). These are products that are also needed in weaker market phases. → This dampens volatility.

2. strong market position + pricing power Several price increases in 2026 (4-7% for UWF, 5-7% for Tissue) show that Navigator can pass on cost inflation. → This stabilizes margins in correction phases.

3. high international diversification Four large plants in Portugal + presence in UK & Spain. → Regional fluctuations have less impact.

4. solid dividend policy Regular dividends (last communicated on 02.06.2026). → Dividend stocks often hold up better in corrections.

🚨 But: Navigator is not a classic defensive stock

Despite the stability points, Navigator remains dependent on:

- Paper and pulp prices

- energy prices

- global industrial demand

- economic cycles

This makes the share less volatile than techbut more volatile than true defensive sectors.

📉 How Navigator typically behaves in corrections

Historically (and in terms of the business model):

- Falls less sharply than cyclical industries

- Recovers fasterif paper prices remain stable

- Runs sidewayswhen demand weakens

- Profits whenwhen price increases go through (as in 2026)

Navigator is therefore a anchor of stability in the portfoliobut not a "safe haven".

🎯 Conclusion for you

Navigator brings robust cash flows, pricing power and dividend stability - this ensures in a market correction for above-average resiliencebut not for absolute crisis resistance.

NVG_Interim_Results_2026_Q1.pdf

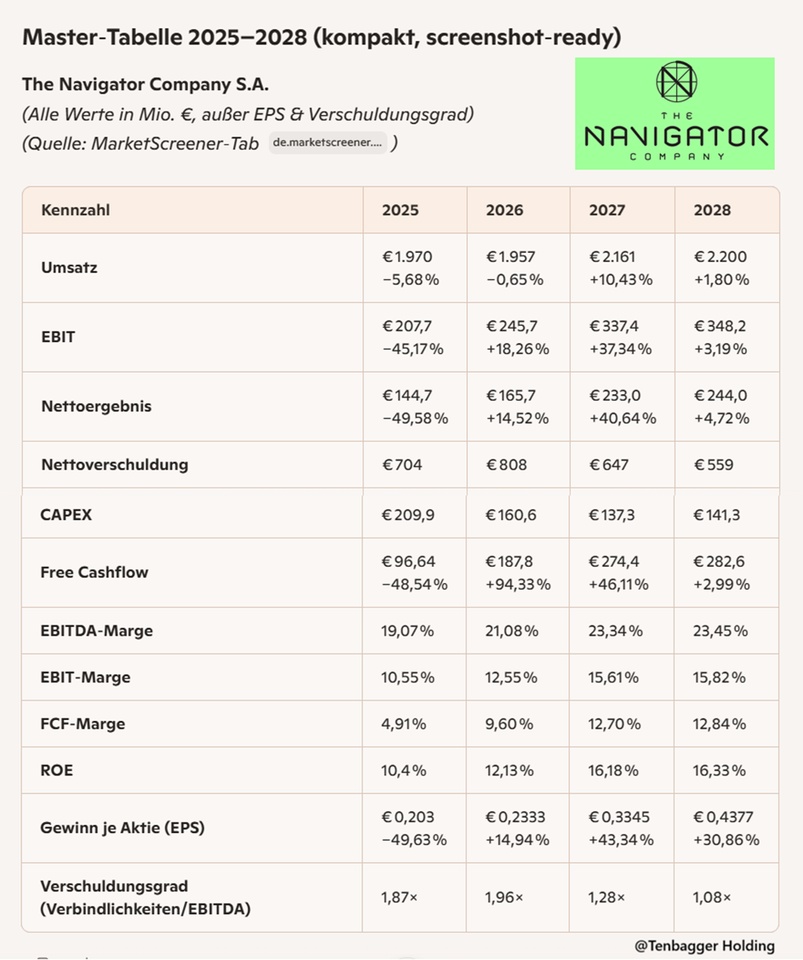

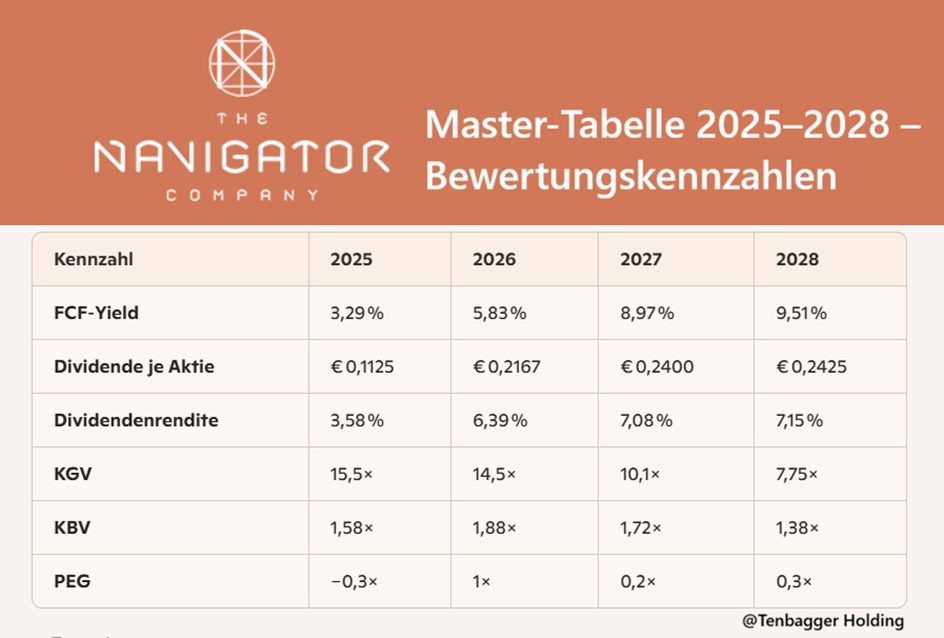

🟣 Juan-style interpretation - Navigator Company (2025-2028)

"Navigator is like a well-oiled industrial engine: not flashy, but reliable, with clean cash flow." - Juan

1) Growth & cycle

- Turnover remains stable to slightly increasing, 2027 clear jump +10 %, then normalization again.

- Not a high-growth stock - rather solid cyclicalwhich will reach its sweet spot in 2027.

Juan take: "It's not a racing car, it's a diesel SUV: pulls consistently, doesn't guzzle much, lasts forever."

2) Profitability - the silent star

- EBIT margin increases from 10,5 % → 15,8 %.

- EBITDA margin climbs to 23 %+.

- FCF margin practically doubles: 4,9 % → 12,8 %.

Juan-Take: "The margin makes the difference. Navigator is becoming more efficient, not bigger - and that is often more valuable."

3) Cash flow - really strong

- Free cash flow grows 2025 → 2028 by almost 3×.

- 2026 is the turbo year: +94 % FCF growth.

- CAPEX decreases structurally → more cash remains.

Juan-Take: "This is FCF quality that you don't expect from paper. It's almost tech level - just without the hype."

4) Balance sheet - clean & ever cleaner

- Net debt falls from € 808 million → € 559 million.

- Leverage (net debt/EBITDA) improves from 1,96× → 1,08×.

Juan-Take: "Navigator is getting lighter financially every year. It's like an athlete losing fat and building muscle."

5) EPS - underestimated lever

- EPS increases 2025 → 2028 by +115 %.

- 2027 & 2028 are the clear earnings power years.

Juan-Take: "The EPS profile is much more dynamic than sales. That is a sign of quality."

6) Overall picture - Juan's conclusion

Navigator is a cash machine cyclical with a quality profile. Not a growth miracle, but a company that margin, cash flow and balance sheet consistently improved.

Juan's summary: "Navigator is like a quiet professional: talks little, delivers a lot. 2027-2028 look really strong."

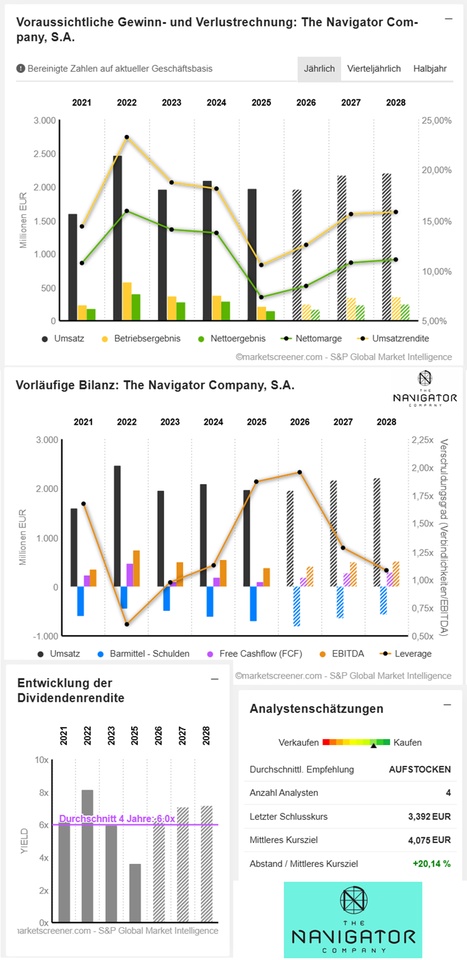

Market value 2,412

Number of shares (in thousands) 711,183

Date of publication 19.02.2026

EUR in millions

Estimates

🟣 Overall Juan conclusion

Navigator is a quality cyclical with a strong cash flow profile and attractive valuation. Not explosive, but extremely solid - and 2027/2028 look really strong.

Juan summary: "Navigator is like a quiet pro: delivers consistently, gets better every year and is almost a value sweet spot in 2027/2028."

And delivers an FCF yield that would even knock Mr. Prompt (@Raketentoni ) off the weight bench.

05,06,2026, 17:55:00 -

Lisbon (EUR)

3,392 EUR