Grupa Kety S.A. specializes in the production and marketing of aluminium components and systems. The Group's activities are divided into three product families:

- Aluminum profiles and components: for the automotive, transport and industrial sectors, etc.;

- aluminum structures: for the construction sector (windows, doors, facades, shutters, etc. for buildings);

- flexible aluminum packaging and polypropylene films: for the food, pharmaceutical and chemical industries.

The geographical breakdown of net sales is as follows: Poland (51 %), European Union (39.2 %), Europe (6.4 %) and Other (3.4 %).

Number of employees: 6,000

Grupa Kety

Production of aluminum profiles and components (extruded products segment, EPS)

ALUPROF

Design and production of architectural systems and sun protection systems (Aluminum Systems segment, ASS)

Alupol

Production of flexible packaging and easily recyclable polypropylene films (Flexible Packaging segment, FPS)

Foreign companies

Alupol Ukraine

The production facility is located in Borodianka, 50 km from Kiev. It includes a modern printing plant offering high-quality extruded products.

The plant's business activities are mainly focused on the Ukrainian market and neighboring countries, as well as on providing processing services for the company.

In its offer, Alupol provides a wide range of standard profiles, however, the plant's production is mainly based on profiles tailored to the individual drawings of customers representing different market segments. Buyers from the construction and building industry are the main group of customers.

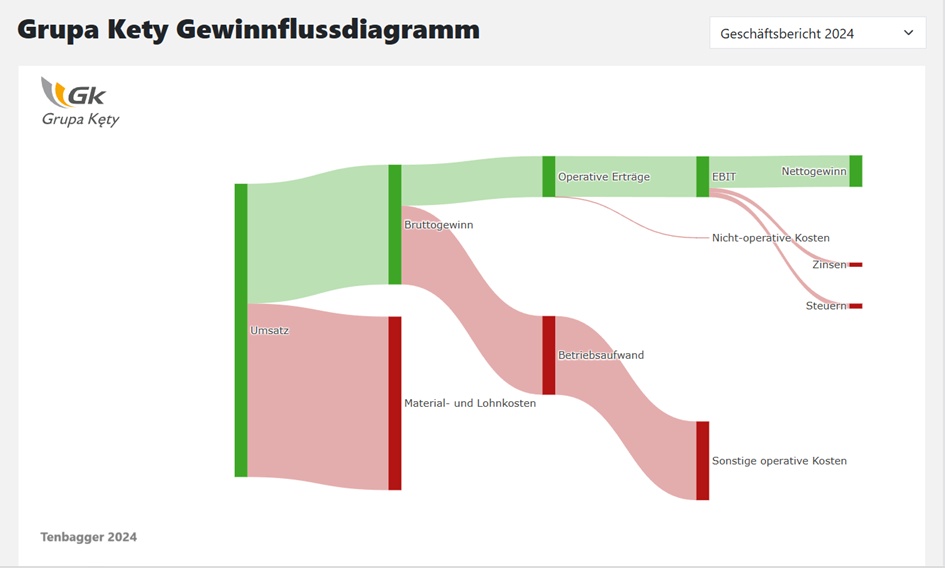

Focus on cash flows that ensure attractive dividends

Grupa Kęty conducts business in three operating segments that are active in markets with different characteristics. Diversification reduces market risk at Group level and increases the stability of the revenue generated. Growing profits and a stable dividend policy, which requires a dividend payment of 85% of consolidated net profit in accordance with the implemented 2021-2025 strategy, enable the financing of further development and profit sharing with its shareholders.

Foreign companies

Aluminum Kety EMMI Slovenia

Aluminum Kety EMMI offers advanced machining and surface treatment of aluminum profiles. It has a great ability to differentiate product ranges.

The Slovenian plant has been operating without interruption since 1946. Many years of experience and modern production infrastructure guarantee high precision and quality of treatment services.

The company supplies aluminum components mainly to European companies that manufacture household appliances, furniture and interior design products, as well as to car manufacturers.

EMMI's business activities are in line with the Extruded Products segment's strategy of building a strong brand on the European market, which is sought by manufacturers of specialized aluminium products.

A high proportion of export sales is possible thanks to Grupa Kęty's well thought-out trade policy.

Within the structures of the Extruded Products segment, there are three foreign representative offices of the company are active:

- Grupa Kety Italia s.r.l., Italy, Milan

- Aluminum Kety Deutschland GmbH, Germany, Dortmund

- Aluminum Kety CSE s.r.o., Czech Republic, Ostrava

Its aim is to support sales on the European markets and build strong business relationships at regional level. Grupa Kęty aims to provide its contractors with appropriately customized services.

COMPANY PRESENTATION

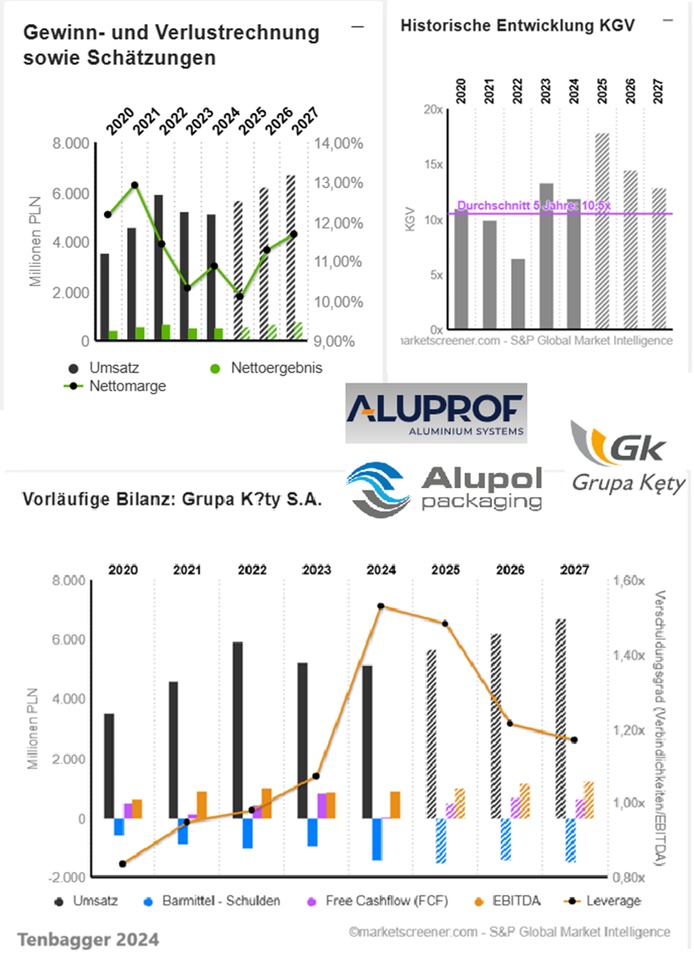

PLN in millions

Estimates

Year Turnover Change

2024 5.144 -1,43 %

2025 5.691 10,64 %

2026 6.222 9,34 %

2027 6.695 7,6 %

2028 7.307

2029 8.505

Year EBIT Change

2024 721 4,89 %

2025 791,9 9,83 %

2026 909,4 14,85 %

2027 990,1 8,87 %

2028 1.104

2029 1.231

Year Net result Change

2024 560,4 3,96 %

2025 575,2 2,64 %

2026 702,5 22,12 %

2027 782,3 11,36 %

2028 853,0

2029 945,0

Year Net debt CAPEX

2024 1.425 664

2025 1.529 231

2026 1.406 251

2027 1.467 359

Year Free cash flow Change

2024 43 -94,83 %

2025 526 1.123,26 %

2026 705 34,03 %

2027 669 -5,11 %

2028 747

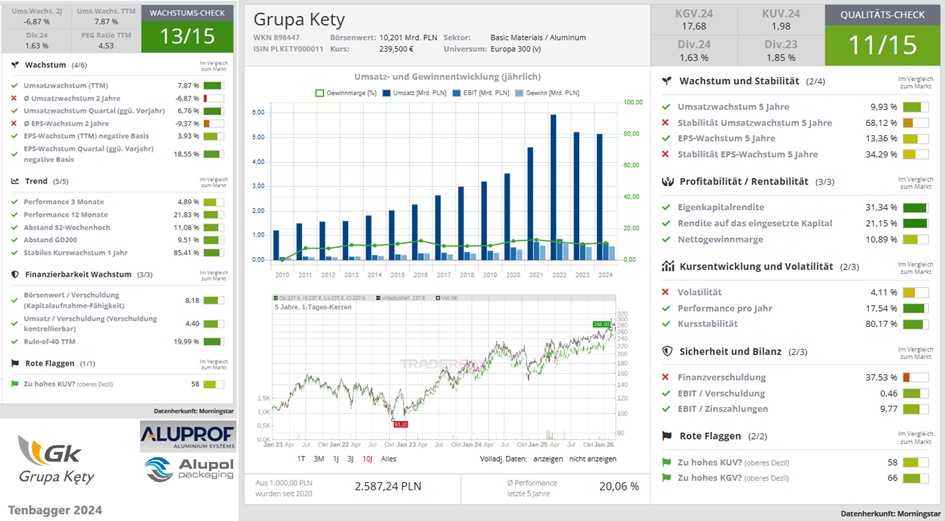

Year EBIT margin ROE Leverage ratio

2024 14,02 % 29,27 % 1,53x

2025 13,91 % 28,87 % 1,48x

2026 14,62 % 32,03 % 1,21x

2027 14,79 % 33 % 1,17x

Year Earnings per share Change

2024 57,59 3,1 %

2025 57,1 -0,85 %

2026 70,76 23,91 %

2027 79,26 12,01 %

2028 86,80

Year Dividend p share Yield

2024 55,4 8,12 %

2025 50,77 4,96 %

2026 53,97 5,28 %

2027 60,99 5,96 %

2028 67,80 6,30 %

Year P/E ratio PEG

2024 11.9x 3.84x

2025 17.9x -21.04x

2026 14.5x 0.6x

2027 12.9x 1.1x

Market value 10,067

Number of shares (in thousands) 9,841

Date of publication 27.03.2025