The real estate market is changing and one company is dominating the digital ecosystem more than ever: Scout24 SE $G24 (-2,3%)

While many are just staring at the interest rates, the Munich-based company is providing hard facts that speak for an investment.

Why is NOW a strategically smart time? Here are the 3 main reasons:

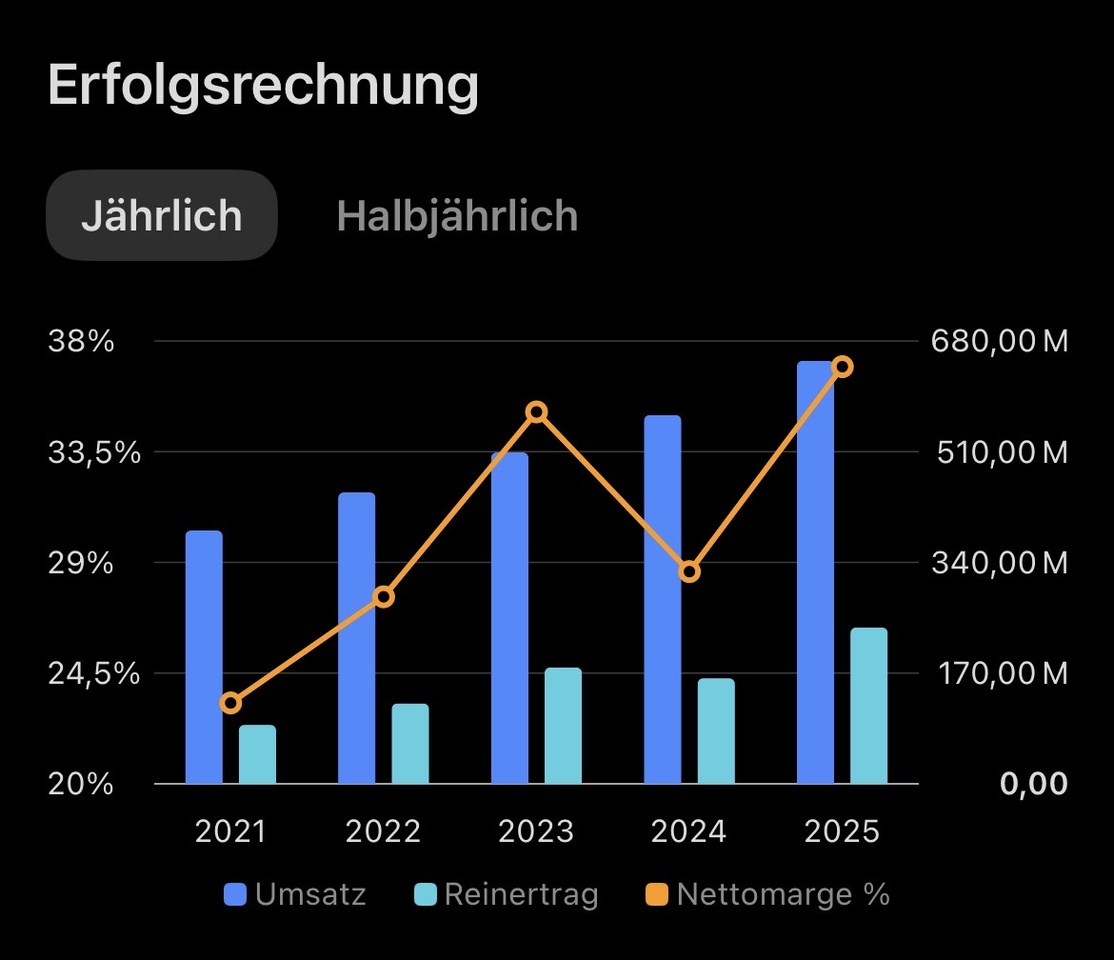

1. margin power at record levels 💰

In the latest Q1 report 2026, Scout24 reported an operating operating EBITDA margin of 60.1%. delivered. This means that for every euro of revenue, more than 60 cents are retained as operating profit. That is Software-as-a-Service (SaaS) excellence at its best.

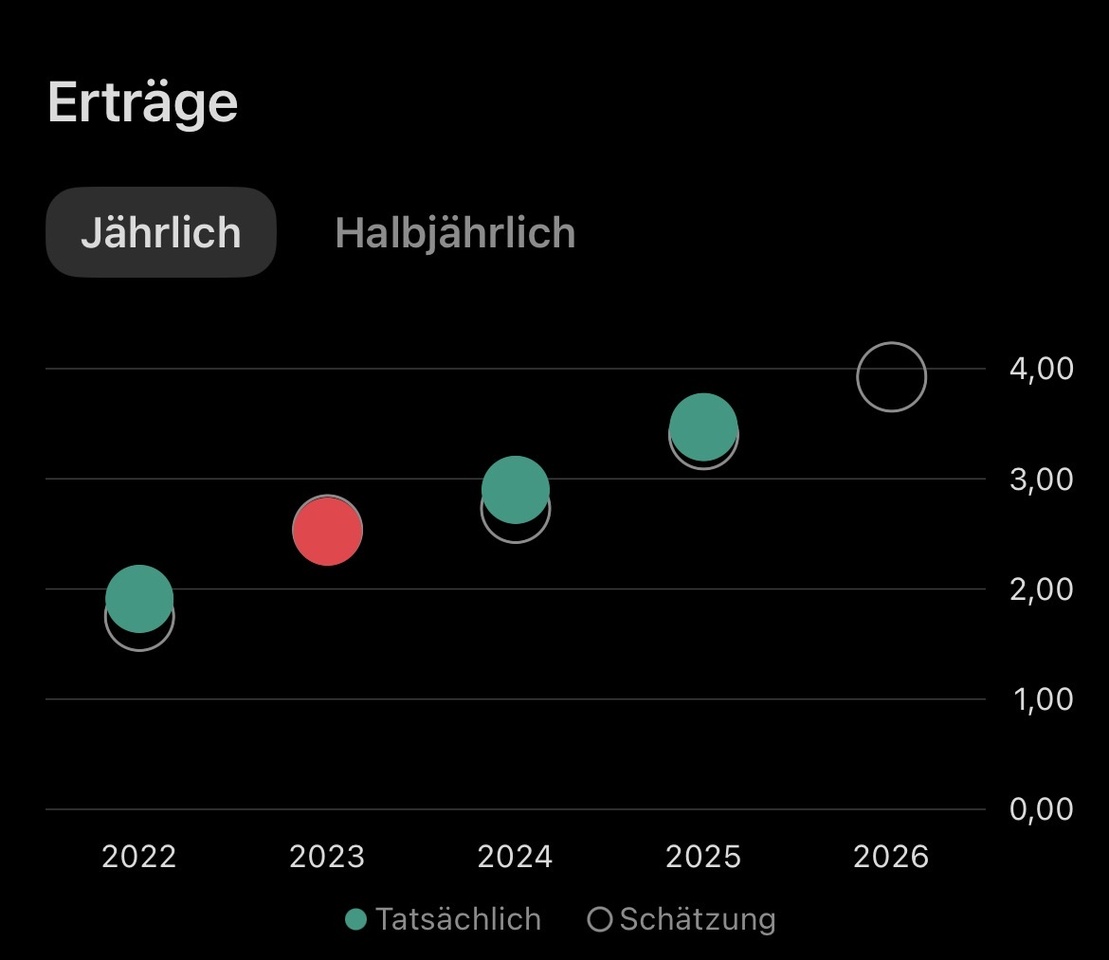

- Sales growth: Double-digit (+13.9 %).

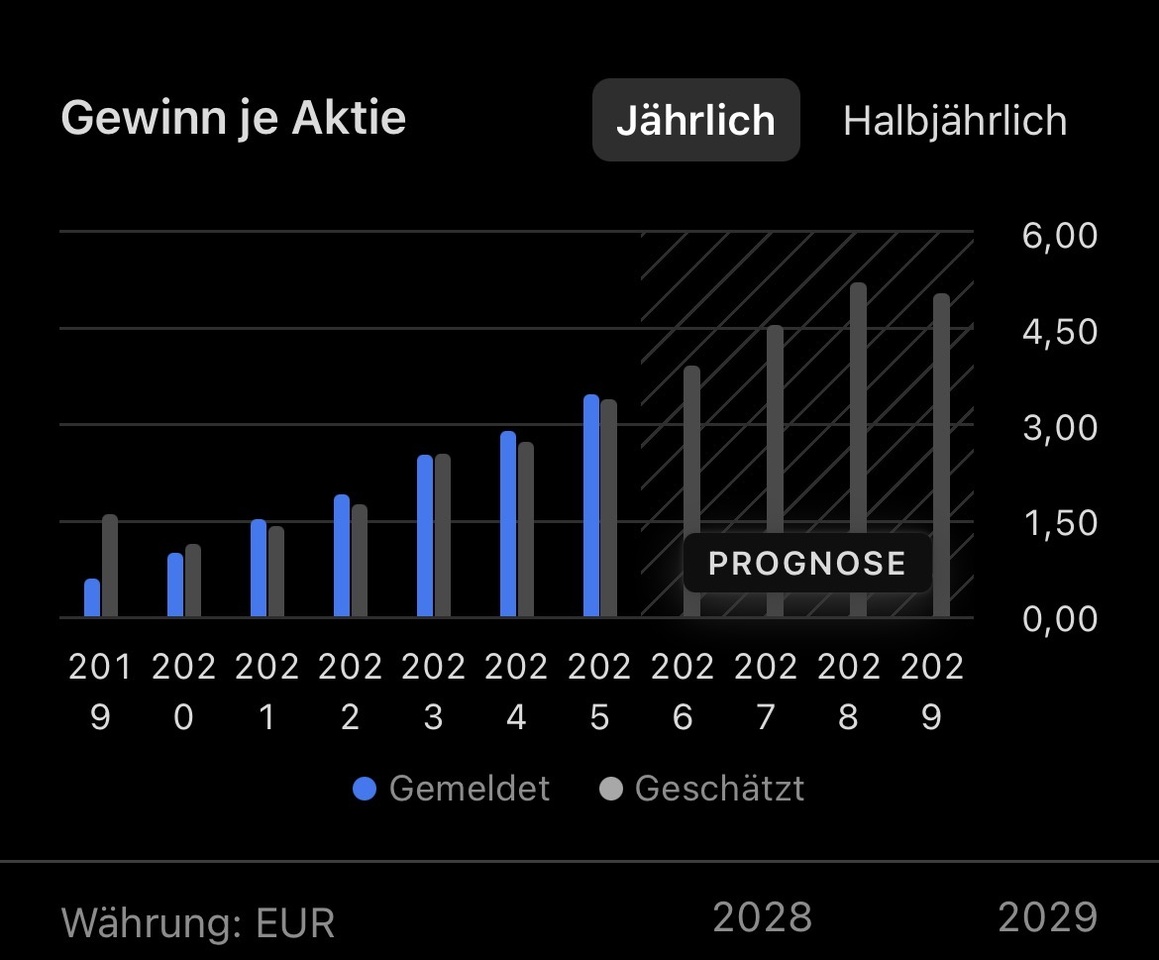

- EPS boost: Earnings per share growth of over 40% shows how efficiently the company is scaling.

2. the "operating system" of the real estate industry 🛠️

Scout24 is no longer just an advertising portal. Thanks to the deep integration of AI tools and CRM software for brokers (B2B), the platform has become indispensable.

- High switching hurdles: Once you manage all your processes via ImmoScout24, you will never leave.

- AI lead: With tools such as PropstackAI, Scout24 is securing its market leadership for the next decade.

3. shareholder value & buybacks 🔄

The management is serious: with a massive share buyback share buyback program of up to EUR 350 million the supply of shares is being reduced. For you as a shareholder, this means that your stake in the company will become more valuable without you having to invest a cent extra.

📉 Chart check & forecast

The share is currently consolidating at a healthy level (approx. EUR 70-75). If the trend continues, analysts see price targets of 90 EUR+ in the next 18 months.

Long-term investors (5 years+) are betting on market dominance in a recovering real estate environment.

Conclusion: Scout24 is the perfect mix of secure moat and dynamic growth.

#Aktien

#Börse

#Investment

#Scout24

#Immobilien

#Finanzen

#WealthManagement

#Aktienanalyse