Hello my dears,

In 2023, after a very long break, I ventured back into the lion cage stock market. A lot had changed and it took me months to find my way back in.

So I also made a mistake at the beginning, which I would like to warn you about.

"Buy because of a story"

A major stock market magazine saw a lot of potential here due to the advancing e-mobility. Of course, I also saw this because of the great story. And I immediately bought a larger position in ElringKlinger shares via my new app. Without checking any valuations or fundamental key figures. After all, these were not listed in the story.

As you can see from the chart, the e-mobility story has been a long time coming. And today I am 70% down on the share 😭.

Of course, there was one good thing about it:

"You learn from your mistakes"

Why am I introducing you to the company today?

Because after this experience I looked at fundamental key figures.

And these show me today that ElringKlinger could be a turnaround candidate.

And the momentum of the last few weeks shows us that investors could also see it that way.

My dear shareholders,

so have fun with our family company today. Which in 2028 with an attractive dividend yield of 7.30 % to show that we are back.

I look forward to your opinions in the comments.

About ElringKlinger

As an independent supplier with a global presence, the ElringKlinger Group is a strong and reliable partner to the automotive industry. Whether passenger cars or commercial vehicles, whether electric motors, hybrid technology or combustion engines, they offer innovative product solutions for all drive types and thus contribute to sustainable mobility.

The company positioned itself early on as a specialist in electromobility - with pioneering battery and fuel cell technology as well as associated components and assemblies, including plastic housings and metal stamped and formed parts.

Customized lightweight design concepts from ElringKlinger reduce vehicle weight, which increases the range of electric vehicles and reduces fuel consumption and CO2 emissions in diesel or gasoline engines.

They are continuously developing their sealing technology for a wide range of applications. Their shielding systems ensure optimum temperature and acoustic management throughout the vehicle. Drive components from ElringKlinger are used in all types of drive systems.

Tool technology and products made of high-performance plastics for the automotive industry and other sectors round off the portfolio. With their components and systems, they are also continuing to grow successfully in the non-automotive sector.

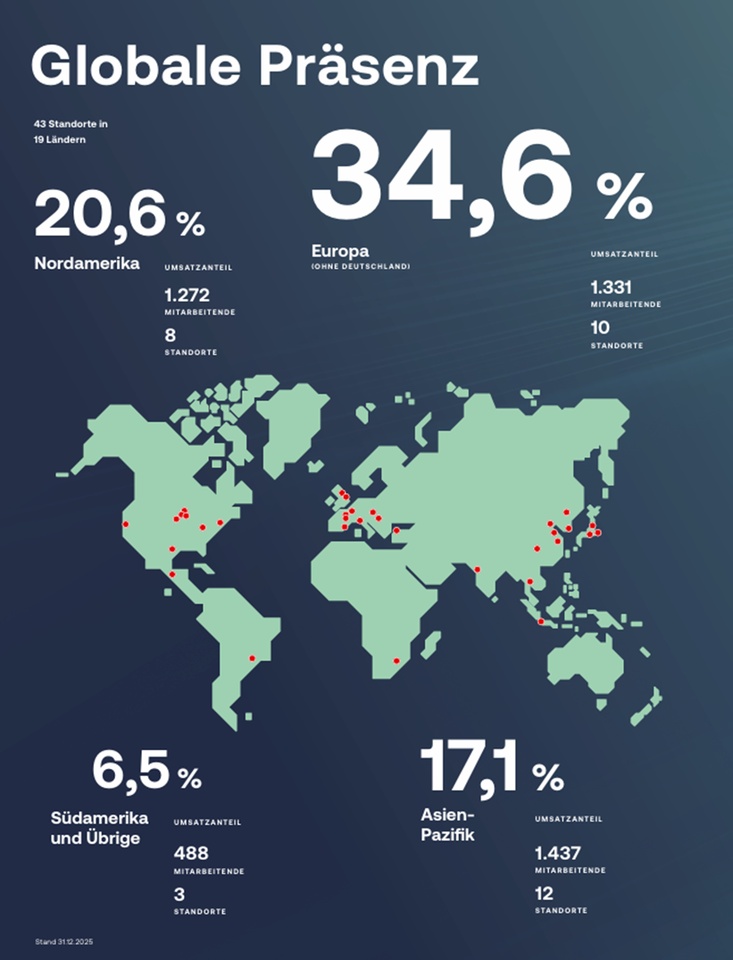

In total, the ElringKlinger Group employs around 8,600 people at some 40 sites worldwide.

Between April and September 2024, the automotive supplier's share price halved. The main reasons for this were the high upfront costs associated with the strategic realignment towards electromobility, which weighed heavily on margins, and the weak macroeconomic environment, including high energy and inflation costs. However, there are now increasing signs that the company has bottomed out and is on the verge of a turnaround. The driving forces behind this turnaround are the two transformation programs.

Elringklinger [WKN: 785602, ISIN: DE0007856023] like many suppliers, is suffering from the structural upheaval in the automotive markets. However, the Group has done its homework with measures to streamline its product range and an ambitious efficiency program in order to initiate an operational turnaround.

Now that the cost-cutting measures have been completed, the Group has a high potential for surprises

With an earnings margin adjusted for one-off costs of almost 6%, Elringklinger has not only exceeded analysts' estimates but also its own forecast for the year. Elringklinger should soon be able to realize a decent increase in net profit again.

In the 2026 financial year, the cost measures introduced should have a full-year effect. With sales of over EUR 1.7 billion and a margin of over 6%, Elringklinger could generate earnings per share of over EUR 1 from 2027 at the latest. With this EPS, the company could also return to a double-digit share price.

ElringKlinger: SHAPE30 on track

Even if the bottom line is still clearly in the red: The transformation of automotive supplier ElringKlinger is making good progress. A dividend will therefore be paid out again at the next AGM. This goes down well on the capital market.

Thursday, 02 Apr 2026

Normally, it would be rather inappropriate to propose a dividend for an annual loss of EUR 10.62 million - corresponding to earnings per share of minus EUR 0.10. However, the automotive supplier ElringKlinger will not be deterred, however, and is putting an unchanged dividend of EUR 0.15 on the agenda for the Annual General Meeting on May 12, 2026. This is formally possible, as the AG balance sheet, which is decisive for the dividend payment, allows for this step. Ultimately, however, there is much more behind it in terms of a signal. On the one hand, the high extraordinary expenses incurred in the course of the company's transformation into a provider with strong expertise in the fields of battery and drive technology obscure the fact that ElringKlinger is making good progress in operational terms.

This can be seen, among other things, in the earnings per share adjusted for extraordinary expenses, which rose from EUR 0.70 to EUR 0.88 in 2025. "This shows that the Group is properly positioned operationally and is essentially successful," says CEO Thomas Jessulat. However, the fact that the Lechler family around the former founder of the company with a stake of just over 52 percent is probably more in favor of a continuous dividend payment. Be that as it may, the ElringKlinger story has been much better received on the stock market in recent weeks. But of course, compared to previous levels of more than EUR 20 and even EUR 35 at its peak (October 2013), the share price is still quite low. The Management Board team still has to prove that the "SHAPE30" strategy communicated in 2024 will actually bring the desired success and increase the share of revenue generated with products outside of traditional combustion technology to more than 50 percent by 2030.

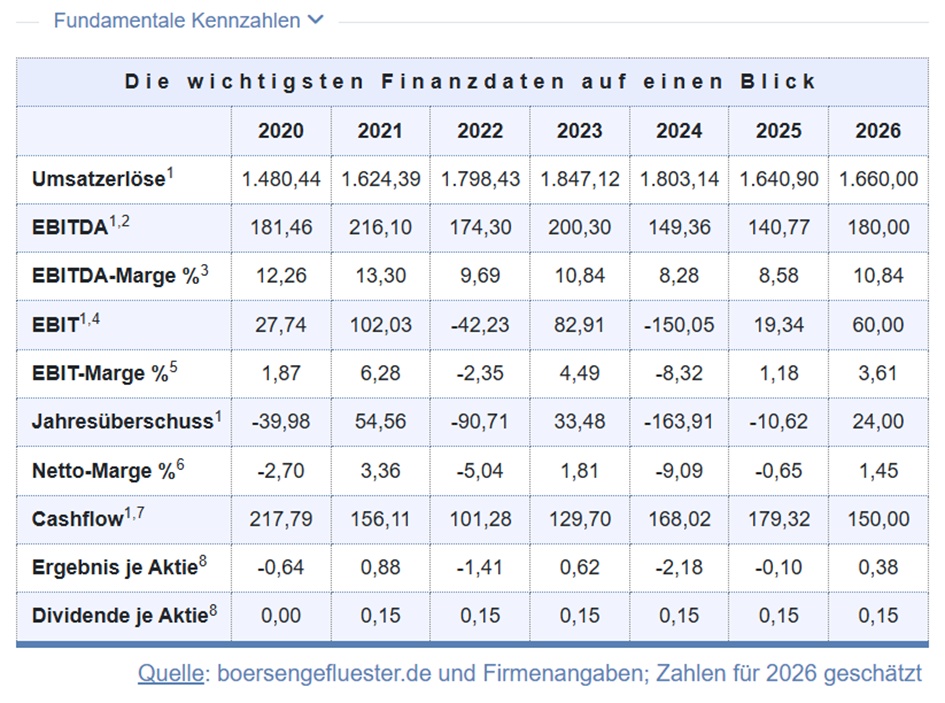

For the current year, the Executive Board expects a slight increase in revenue and an EBIT margin adjusted for special effects of between 6% and 7%. By way of comparison, ErlringKlinger reported an adjusted operating margin of 5.4 percent for 205. Even if it is currently difficult to estimate what adjustments the company will have to make by the end of the year as part of its transformation. At the moment boersengefluester.de considers a turnaround based on the figures actually reported to be a realistic scenario. The operating free cash flow is also expected to be slightly positive - after around EUR 33 million for 2025. In balance sheet terms, the company is still in a pretty good position with an equity ratio of 35.2% and net financial liabilities of a good EUR 287 million. After all, net debt is only around twice the EBITDA reported for 2025.

This ratio is set to fall even further in the medium term. At present, however, ElringKlinger is well on track in this respect. Nevertheless, the loss-making years of the recent past have not been without consequences. In 2021, the equity ratio was a much more comfortable 47 percent. On balance, investments in Investments in the shares of automotive suppliers certainly remain a risky bet. However, ElringKlinger is currently heading in the right direction. In addition boersengefluester.de the company's valuation is comparatively moderate. On a debt-free basis (including pension provisions), ElringKlinger is trading at just a factor of 5 on the EBITDA reported for 2025. The discount of around 45 percent on the current book value of EUR 9.40 per share is also remarkable. The dividend yield of 2.8 percent is also quite attractive.

ElringKlinger: SHAPE30 im Plan · Die beste Seite für Deutsche Aktien · © boersengefluester.de · 2026

ElringKlinger: profit to double by 2028

31.03.2026

The analysts at DZ Bank view ElringKlinger's figures for 2025 as positive.

ElringKlinger: Gewinn soll sich bis 2028 verdoppeln | 4investors.de

March 26, 2026 | IR release

Geschäftsjahr 2025: ElringKlinger steigert Profitabilität und treibt Transformation voran

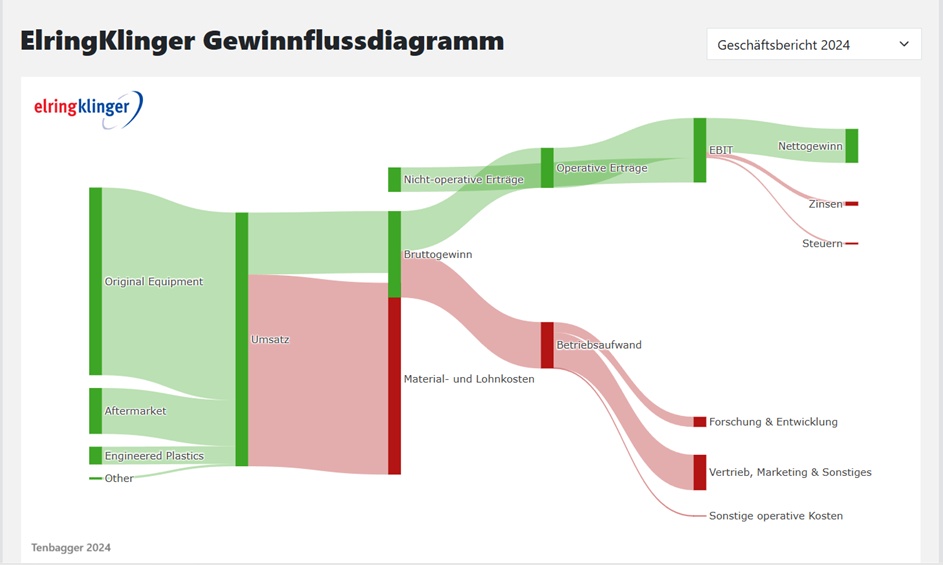

Group sales at EUR 1.641 billion (2024: EUR 1.803 billion, reference level[1]2024: EUR 1.643 billion), organic growth of 2.3%Adjusted EBIT margin increased to 5.4% (2024: 4.9%), adjusted EBIT at EUR 88.6 million (2024: EUR 87.6 million), operating free cash flow...

ANNUAL REPORT 2025

elringklinger-gb-2025-de-geschuetzt_rgb__2_.pdf

elk-2025-hgb-jahresabschluss-de__1_.pdf

elk-2025-hgb-jahresabschluss-de__1_.pdf

ElringKlinger in transformation mode: e-mobility growing rapidly, margins rising - is the turnaround coming now?

26,03,2026

ElringKlinger AG sends a clear signal for 2025: the transformation course is taking effect. Despite a decline in revenue at first glance, the operational picture is more stable and increasingly profitable. For investors, this could be the start of a revaluation.

Decline in sales is deceptive - business is growing operationally

At first glance, sales of € 1.64 billion appear significantly weaker than in the previous year. However, this decline is mainly due to technical factors:

- Sales of parts of the company

- Currency effects

Adjusted for these effects, this results in organic growth of +2.3 %.

This is crucial: ElringKlinger is growing again - despite the difficult market environment within the automotive industry.

Margins rise - profitability improves

Even more important for investors is the earnings trend

- Adjusted EBIT margin: 5.4 % (previous year: 4.9 %)

- Adjusted EBIT: slightly increased

- Target range achieved or exceeded

This shows that the transformation is already having an impact on earnings.

Although one-off effects (including restructuring costs) had a negative impact on the reported result, the company is clearly becoming more profitable in operational terms.

E-mobility explodes - growth driver of the future

The biggest driver is clearly the e-mobility business:

- Turnover: +40.8% to € 144 million

This was due to the ramp-up of a high-volume series order for a global battery manufacturer.

ElringKlinger is thus increasingly positioning itself as a supplier to the e-mobility sector - a decisive step away from the traditional combustion engine business.

Aftermarket and plastics technology also grow

In addition to e-mobility, other areas are also showing strength:

- Spare Parts: +12,5 %

- Plastics technology: +11,2 %

The spare parts business in particular ensures more stable income - an important buffer in a cyclical market.

Tough cuts - but with clear prospects

However, the transformation is not a sure-fire success:

- Site closures

- Sale of subsidiaries

- "STREAMLINE" cost-cutting program

These measures led to special effects of around € 69 million in 2025.

However, this is offset by annual savings of around € 50 million which should have an increasing effect from 2026.

Stable cash flow, debt under control

The financial side also remains solid:

- Free cash flow: € 33.1 million

- Net debt: within target range

- Working capital: significantly improved

This shows that financial stability has been maintained despite the transformation.

Dividend remains constant

Important for investors: the dividend will remain stable at 0.15 per share per share.

This signals confidence in the company's own development - despite the restructuring phase.

Forecast 2026: Margins continue to rise

ElringKlinger is forecasting a further improvement for the current year:

- slight organic revenue growth

- EBIT margin: 6% to 7%

- long-term: around 8%

Drivers should be:

- ramp-up of e-mobility projects

- Savings from STREAMLINE

- Effects from the SHAPE30 strategy

Classification: Traditional automotive supplier in transition

ElringKlinger is exemplary for many European automotive suppliers:

- Decline in traditional business

- Development of new technologies (e-mobility, hydrogen)

- Focus on efficiency and profitability

The difference: concrete progress can already be seen here - both in terms of growth and margins.

Conclusion: transformation is taking effect - share with turnaround potential

ElringKlinger will deliver exactly what investors want to see in 2025:

- organic growth

- rising margins

- clear strategic progress

The transformation is not yet complete - but the direction is right.

If the momentum in the e-mobility segment continues and the cost effects take hold, the share could be on the verge of a real turnaround phase.

ElringKlinger im Umbau-Modus: E-Mobility wächst rasant, Margen steigen – kommt jetzt die Trendwende?

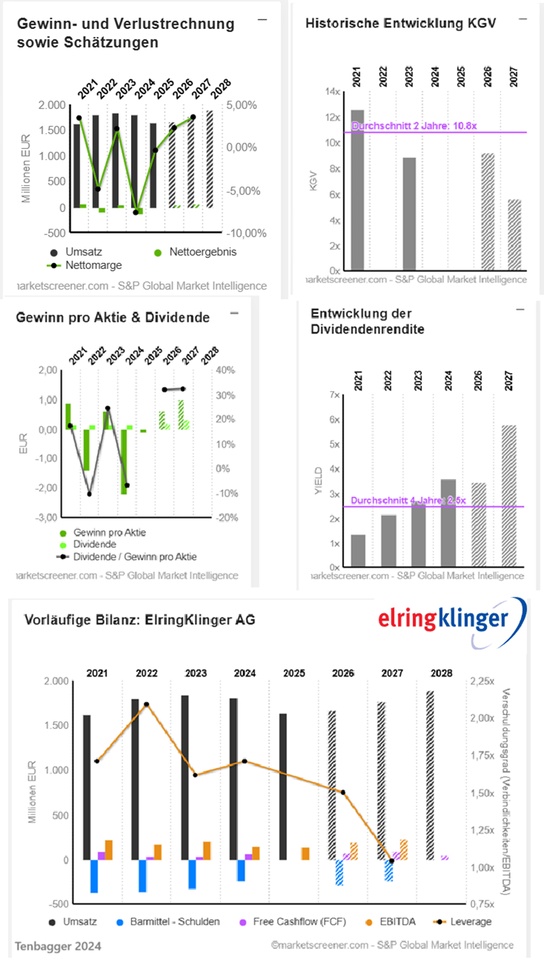

EUR in millions

Estimates

Year Turnover Change

2025 1.641 -9 %

2026 1.665 1,5 %

2027 1.771 6,32 %

2028 1.886 6,51 %

Year EBIT Change

2024 87,55 5,6 %

2025 88,65 1,25 %

2026 89,44 0,9 %

2027 125,5 40,27 %

Year Net result Change

2024 -137,8 -450,64 %

2025 -6,146 95,54 %

2026 38,05 719,1 %

2027 62,6 64,52 %

Year Net debt CAPEX

2024 246 108,3

2025

2026 286 91,35

2027 242 89,6

2028 85

Year Free cash flow Change

2024 58,41 57,86 %

2025

2026 72,35

2027 91,8 26,88 %

2028 47 -48,8 %

Year EBITDA margin EBIT margin ROE

2024 7,99 % 4,86 % -18,63 %

2025 8,58 % 5,4 %

2026 11,48 % 5,37 % 6 %

2027 13,15 % 7,08 % 9,14 %

Year Debt-equity ratio

2026 1,5x

2027 1,04x

Year Earnings per share Change

2024 -2,18 -451,61 %

2025 -0,1 95,41 %

2026 0,6008 700,83 %

2027 0,9889 64,59 %

Year FCF Yield

2026 11,4 %

2027 15,5 %

2028 13,4 %

Year Dividend Yield

2024 0,15 3,57 %

2025 0,15 3,48 %

2026 0,1913 3,46 %

2027 0,3194 5,78 %

2028 0,40 7,30 %

Year P/E ratio PEG

2024 -1.93x 0.42x 0x

2025 -43.1x 0.5x

2026 9.2x 0.53x -0x

2027 5.59x 0.48x 0.1x

2028 4,18 0,55

Market value 350.4

Number of shares (in thousands) 63,360

Date of publication 29.03.2026

Performance

1 week -0.54 %

1 month +23.99 %

6 months +31.04 %