Good morning, my dears,

I don't want to write many words of introduction today. And go straight to the introduction.

As always, we look forward to many comments.

On March 24, Jensen Huang, CEO of NVIDIA, said on the Lex Fridman podcast, "I think we're there now. I think we've reached AGI." In terms of this scenario, I find Fabrinet exciting. If we take Huang's outlook as a basis, then I see 3 reasons why it makes sense to buy into Fabrinet shares right now: Autonomous AI agents and the future outlined by Huang require huge GPU clusters. The absolute bottleneck of these data centers is no longer just the chip itself, but the communication between the tens of thousands of GPUs. Fabrinet is the undisputed world market leader in the high-precision manufacture of optical transceivers and communication components. Without the optical connections manufactured by Fabrinet, the data streams required for AGI-like workloads simply cannot be transported.

Huang predicted chip demand of USD 1 trillion by 2027 in the wake of his AGI statements. Fabrinet is a primary contract manufacturer for NVIDIA's optical networking solutions, albeit with a much more moderate valuation than many chip designers. The P/E ratio for the 2027 financial year is 4.1 and 37.

With the rapid increase in computing power, conventional cables in data centers are finally reaching their physical limits. The future belongs to silicon photonics and co-packaged optics, in which light is brought directly onto or extremely close to the chip for data transmission. The packaging of these components requires incredible precision on a microscopic level. Over the years, Fabrinet has built up a large technological moat in this highly complex niche. This creates long-term customer loyalty.

Darum sehe ich bei Fabrinet mittelfristig weiteres Potenzial!

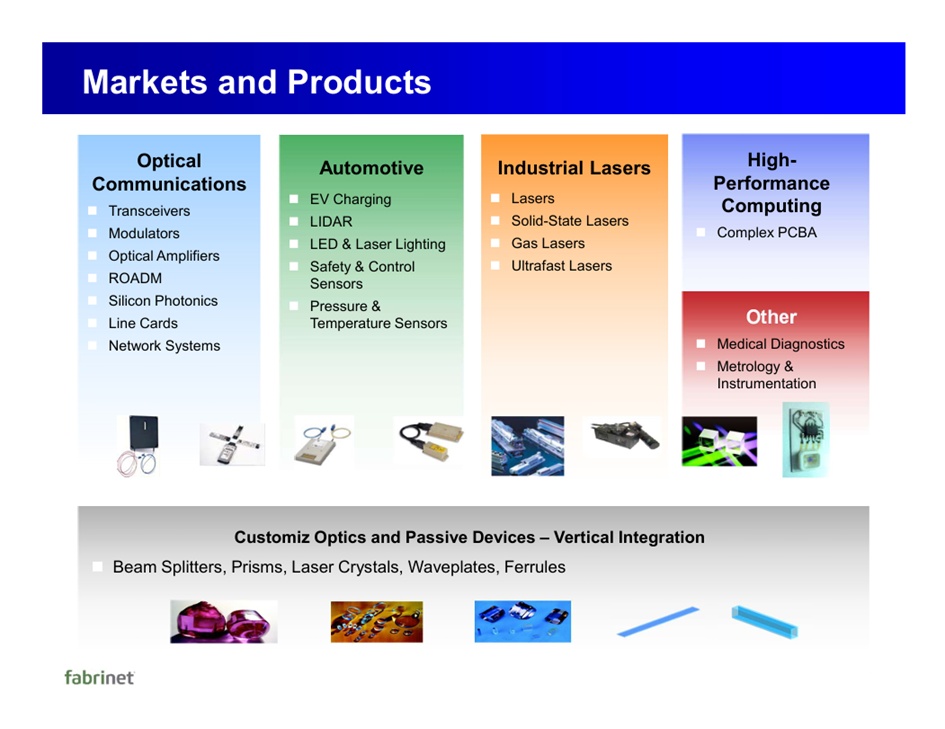

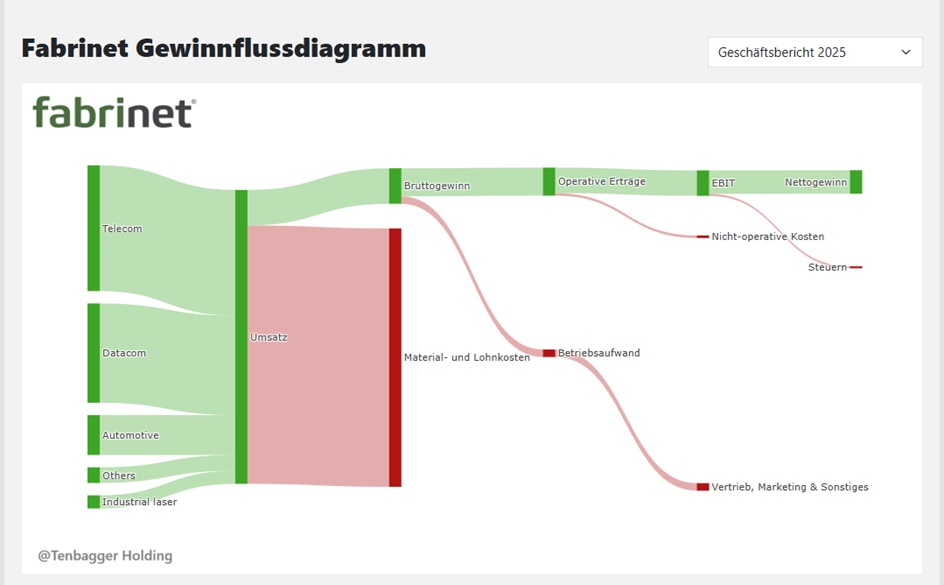

Fabrinet is a provider of advanced optical packaging and precision optical, electromechanical and electronic manufacturing services to original equipment manufacturers of complex products such as optical communication components, modules and subsystems, automotive components, industrial lasers, medical devices and sensors. The company offers a range of advanced optical and electromechanical capabilities across the entire manufacturing process, including process design and development, supply chain management, manufacturing, complex PCB assembly, advanced packaging, integration, final assembly and testing. The company focuses primarily on low-volume production of a variety of highly complex products. In addition, the company designs and manufactures application-specific crystals, lenses, prisms, mirrors, laser components and substrates (custom optics) as well as other custom and standard products in borosilicate, clear fused silica and synthetic fused silica (custom glass).

Number of employees: 16,457

05,05,2026

Brief summary of the report

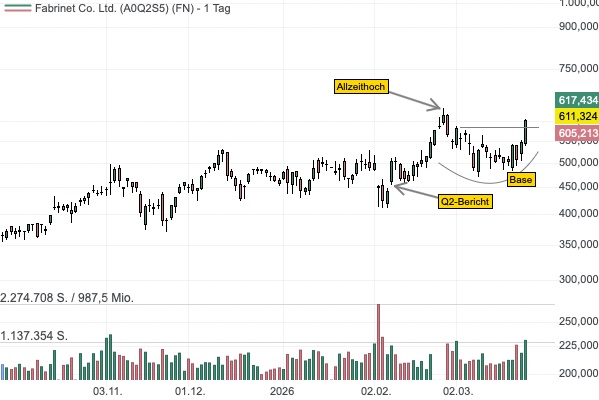

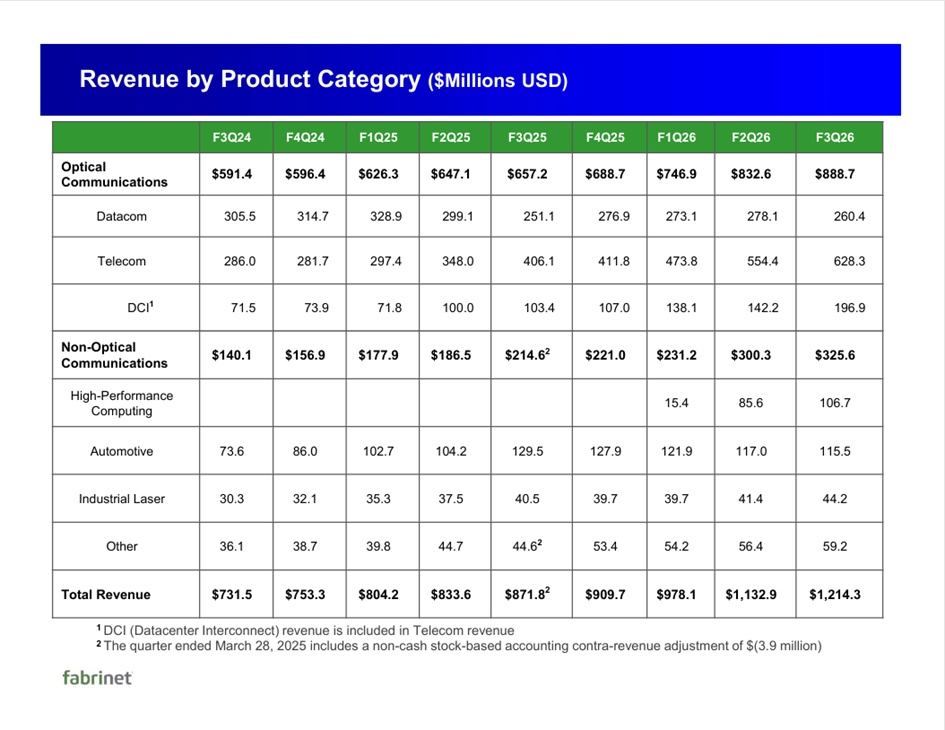

The Fabrinet share has fallen despite better than expected sales in Q3 by 12.88 % in Q3. The company reported:

- Turnover: USD 1.21 billion → +39 % YoY, +7 % QoQ → USD 37 million above analyst estimates

The strong driver was the telecommunications segment:

- +55 % YoY, +13 % QoQ

- Particularly strong: Data Center Interconnect → 197 million USD, +91 % YoY, +39 % QoQ

Why is the share still falling?

The outlook for Q4 disappointed. Reason: continuing supply bottlenecksthat are slowing down growth.

- Around 150 million USD HPC turnover will be postponed to the next quarter.

- Datacom and HPC were weaker than expected.

What do analysts say?

Barclays:

- Positive Q3, but Q4 outlook limits potential.

- Supply bottlenecks remain the main problem.

Rosenblatt:

- Price target raised: USD 715 → 750

- Very optimistic for OCS and CPO

- Fabrinet makes targeted investments in advanced packaging

- Minority stake in Raytek Semiconductor strengthens position in CPO ecosystem.

Wolfe Research:

- Results positive overall

- But: Decline in Datacom segment could disappoint investors

- Highlighted: new hyperscaler deals, Amazon order, expansion of production capacities

May 04, 2026

Fabrinet gibt Finanzergebnisse für das Geschäftsjahr 2026 für das dritte Quartal bekannt

Microsoft PowerPoint - Fabrinet Investor Deck May 2026 v2.pptx

Geographical distribution of sales:

2025 (USD)

U.S. 1.47 billion

Israel 993 million

India 324 million

U.K. 156 million

Hong Kong 101 million

Other Europe 81.69 million

Thailand 57.37 million

China 56.36 million

Singapore 52.54 million

Germany 43.89 million

Japan 37.54 million

Malaysia 32.4 million

Other North America 6 million

Other Asia-Pacific and Oth 2.94 million

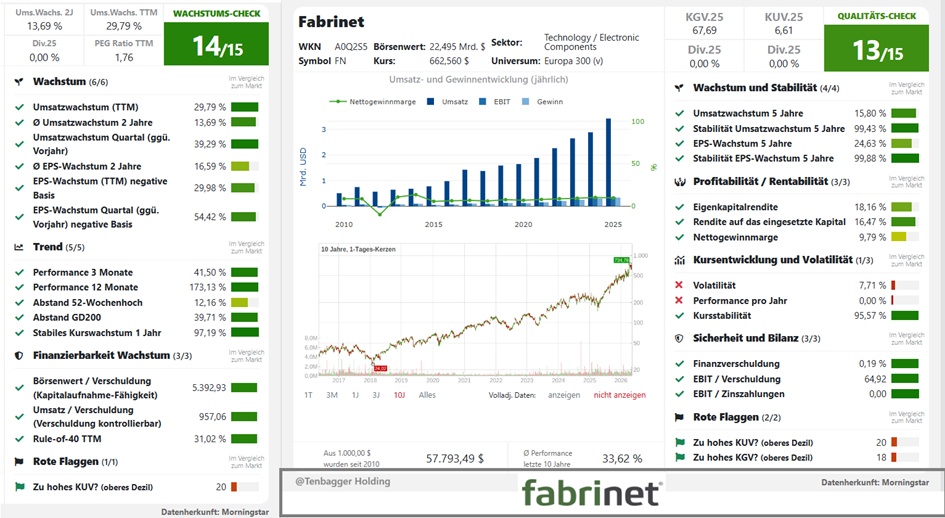

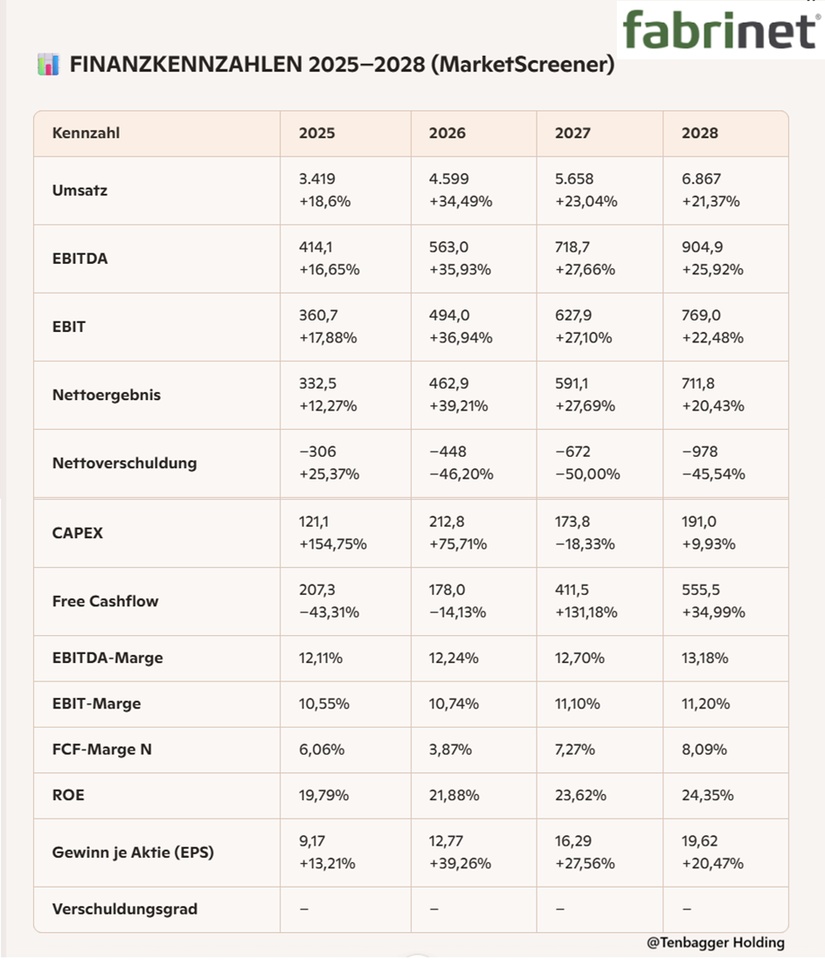

🧑💻 Juan conclusion on the key financial figures 2025-2028

Fabrinet delivers a number setup here that looks almost outrageously clean. The store is not only growing - it is accelerates. Turnover, EBITDA, EBIT, net profit: everything is growing at double-digit rates year after year, and 2026 is set to be a real turbo boost.

The margins? Stable, strong and slightly increasing. This is rare with such high growth.

The free cash flow jumps brutally upwards from 2027 - exactly the pattern you want to see in future compounders.

The net debt? Actually none. Fabrinet is building more net cash every year. That's like a built-in safety belt for the valuation.

ROE increases continuously → management knows how to scale capital

EPS grows cleanly in double digits → shareholder value machine.

In short: Fabrinet looks like a company that is simultaneously growing, becoming more efficient and becoming financially stronger. To me, that screams: "high quality compounder in the making". Hoodie-approved."

Market value 22,260

Number of shares (in thousands) 35,830

Date of publication 18,08,2025

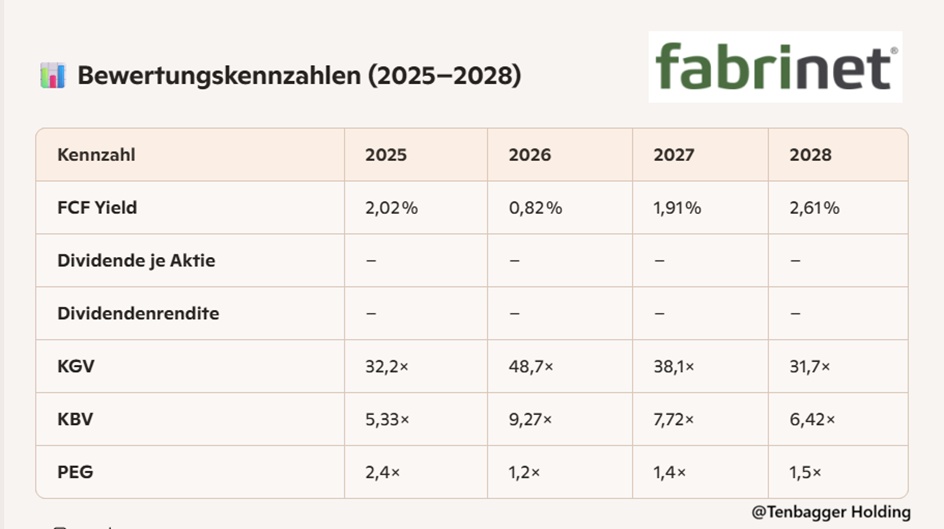

🧑💻 Juan conclusion on the valuation ratios

"So... Fabrinet's valuation is a bit like a high-end chip: expensive, but not without reason. The P/E RATIO seems crisp at first glance, but the EPS growth justifies much of it.

The PEG between 1.2 and 1.5 shows: This is no bargain, but neither is it overheated hype - rather Quality growth at a fair price.

The P/B RATIO rises briefly, but then falls back again cleanly, which shows that equity is growing strongly. The FCF yield is low in 2026, but rises sharply from 2027 - exactly the pattern you want to see in a future compounder.

In short: Fabrinet is not "cheap", but highly highly valued, but with a clear fundamental underpinning. A classic case of: Quality costs - and delivers."

Performance:

1 week -12.07 %

1 month +1.82 %

6 months +38.33 %

1 year +198.55 %

3 years +564.54 %

5 years +628.77 %

7 years +953.73 %

10 years +1,701.33 %

PRICE: 548.60€ 12.05.2026 at 9:42 a.m.