Hello everyone!

Here is once again Raketentoni from Denmark with a game from the Scandinavian home market. Maybe finally something for @Multibagger

Today we are looking at a Swedish company that sits right at the interface between AI software and regulatory constraints. While many people only think of ChatGPT when they think of AI, Smart Eye $SEYE (+0,95%) provides the "eyes" for the automotive industry. With the massive tailwind of EU legislation, this could create leverage that hardly any other tech stock in this segment currently offers.

Small info: I am not invested yet, waiting for the prices of the Hunters List, see below.

1. what the company does

Smart Eye is the world market leader in the field of Driver Monitoring Systems (DMS). Their AI-based camera systems detect driver fatigue, distraction or discomfort in real time. Through the acquisitions of iMotions and Affectiva, they also cover behavioral research. The core, however, are the "design wins" at over 20 global car manufacturers.

2. key figures, data & facts (as at May 2026)

- Market capitalization (market cap): approx. SEK 2.1 billion

- Price/sales ratio (P/S ratio): approx. 4.8

- Sales growth (YoY): +26% (strongly increasing)

- Operating result (EBIT): SEK -31.2m (still negative)

- Share price: ca. SEK 85

3. core quality formula check

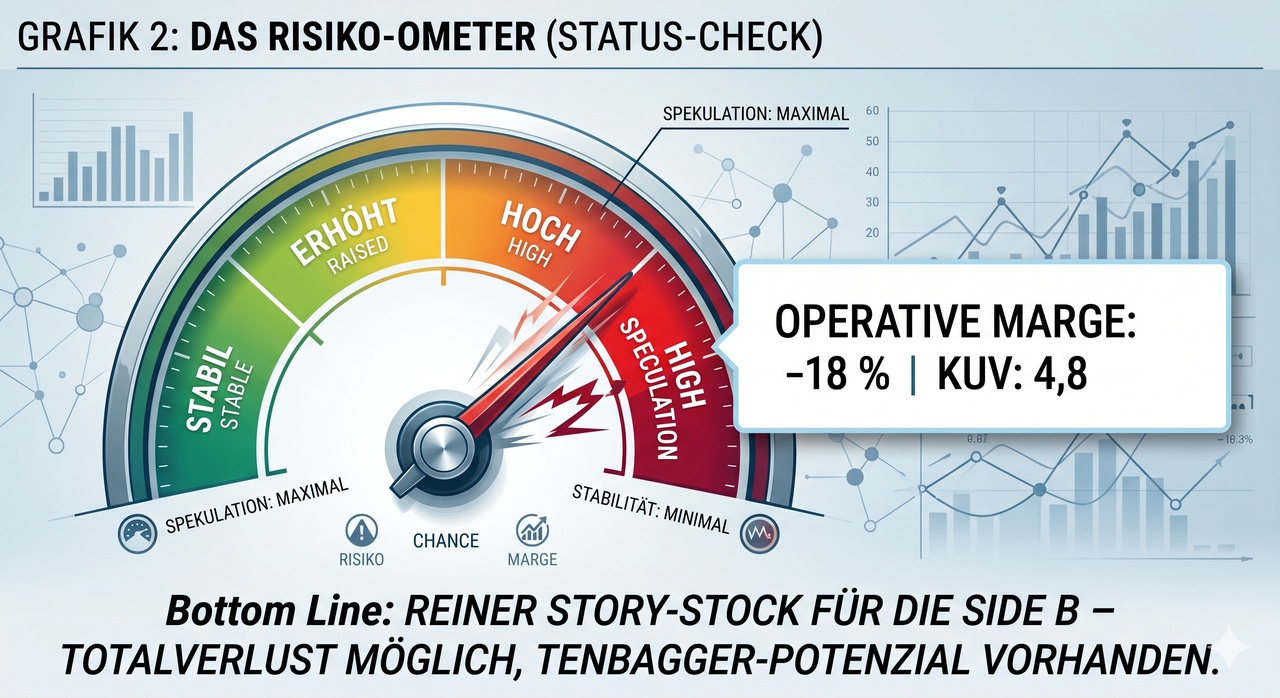

- Sales growth (26%) + operating margin (-18%) = score 8

- Verdict: With a score of 8, Smart Eye is well below the 15-point hurdle. It is currently a purebred story stockas profitability is still a long way off.

4. cash flow quality formula check

The operating cash flow is approaching zero, but is still negative due to high R&D investments. The company is currently scaling up production for the major car manufacturers - this is eating up money for the time being.

5th Dividend Filter Check0.0 % dividend.

Absolute fail for the income foundation. Smart Eye $SEYE (+0,95%) is a pure Side B resident.

6th Exclusion Rule CheckStory > Numbers.

As the operating margin is permanently below 5%, the share would be thrown out immediately according to conservative filters. Anyone who buys here is betting coldly on future scaling due to legal requirements.

7. future prospects & competition

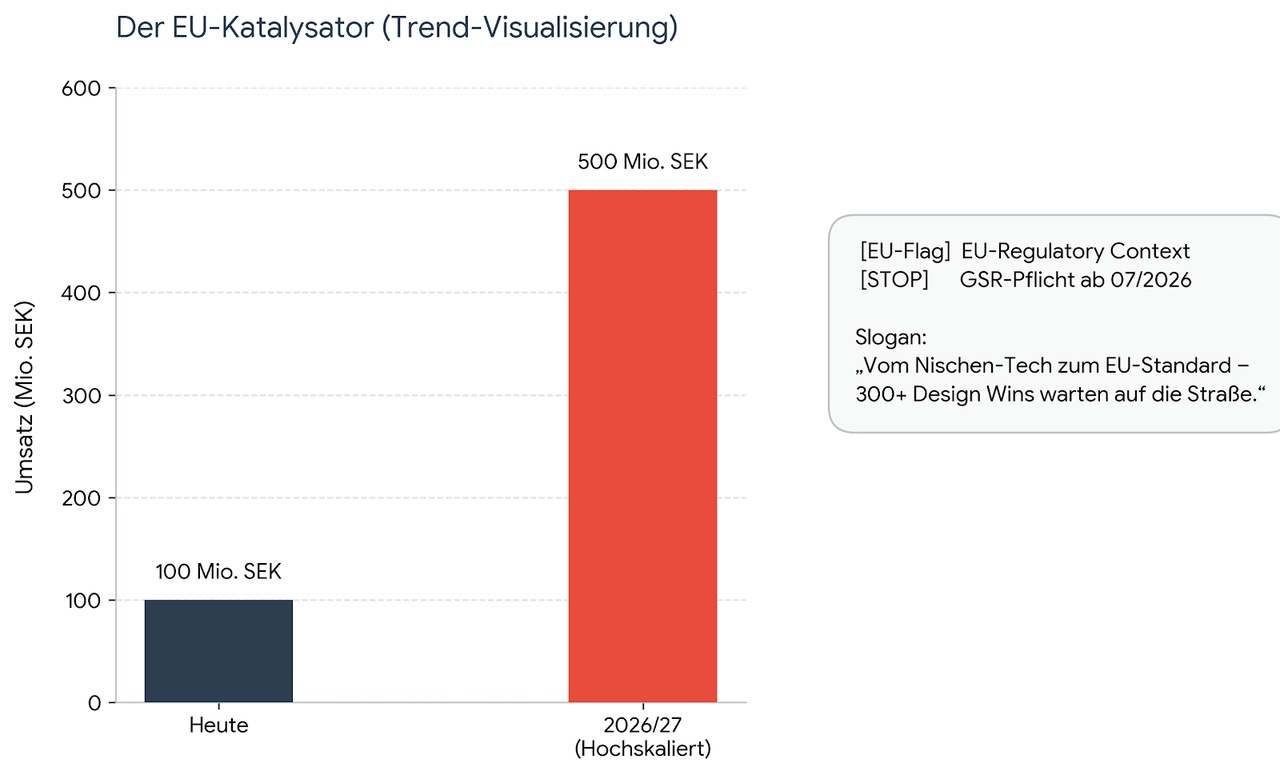

The joker is the EU General Safety Regulation (GSR). From July 2026, all newly registered vehicles in the EU must have DMS. Smart Eye already has over 300 design wins under its belt. Its main competitor is Seeing Machines from Australia, but Smart Eye is often ahead in terms of technology (especially when it comes to emotion AI).

8. chart analysis of the last few months

The share has been bottoming out for a long time. After the massive sell-off of previous years, the share price is currently stabilizing in the SEK 80-90 range. The downward trend has been broken and momentum is slowly building up again.

9 Special Entry Zones (Bargain Hunter's List)

- Zone 1 (Speculative entry): SEK 80.00 - SEK 85.00 (Current level).

- Zone 2 (Absolute bargain): < SEK 70.00 (Historical bottom).

10. perspective on future viability

DMS is no longer a "nice-to-have", but is becoming a "must-have" due to the EU. Future viability is almost guaranteed from a regulatory perspective. The risk lies in whether the management will actually reach break-even in 2026/27 or run out of steam (cash) before then.

11 Potential alternatives

- Seeing Machines: The direct pursuer. Similar risk profile.

- Mobileye: The giant for assistance systems (more expensive, but already profitable).

12. conclusion & profit margin outlook

Smart Eye is a lottery ticket with an announcement. As soon as the design wins go into mass production, the license fees flow almost without additional costs. The target is an operating margin of > 20 % by the end of the decade. Until then, it remains a high-risk momentum play for Side B.

13. voices of the CEO

The CEO and co-founder of Smart Eye, Martin Krantz, is consistently confident about the future of the company in recent quarterly reports and press releases. A central theme is the successful transition from the development phase to the production phase, as the secured 'design wins' are now flowing into series production at car manufacturers. Krantz consistently emphasizes Smart Eye's strong market position and technology leadership, particularly following the integration of strategic acquisitions such as Affectiva.

His tone is characterized by a focus on operational excellence and the conviction that Smart Eye will make a decisive contribution to road safety through the regulatory impetus in Europe (GSR) and at the same time generate significant growth. He sees the company on a clear path to profitability, driven by the scaling of the automotive business.

14. opinion of the analyses

The majority of analysts' opinions on Smart Eye AB are positive. Analysts who cover the company intensively (often specialized Swedish analyst firms) see Smart Eye as a clear beneficiary of the emerging wave of regulation.

- Main arguments for 'buy':

- Technology leadership: Smart Eye is seen as the technical benchmark in the DMS market.

- Regulatory tailwinds: The EU GSR obligation from 2026/27 is seen as a huge growth driver and revenue guarantor.

- Design wins: The high number of secured orders offers clear revenue visibility for the coming years.

- Challenges & discussion topics:

- Profitability timing: Discussion often centers on the exact timing of when 'break-even' will be reached, as cash burn for scaling and R&D remains significant.

- Valuation: Due to the high P/E ratio, the valuation is sometimes discussed as ambitious, making the stock prone to volatility on disappointment.

To summarize: Analysts see Smart Eye as a highly interesting growth company in a regulated future market, where the long-term potential outweighs the short-term risks of cash burn. Buy recommendations clearly dominate the picture.

Finally a gamble again! A tenbagger? What do you think?

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Stocktective

@Simpson

@WarrenamBuffet

@SAUgut777

@TradingHase

@PikaPika0105

@Derspekulant1

@NichtRelevant

@Klein-Anleger and of course everyone else :)