I wanted to rotate some of my industrial stocks so I started to put money in $DHL (+0,56%) and $LOG (-0,38%)

Both are European logistics powerhouses, but our engine is flagging them for two very different reasons. Here is the algorithm breakdown:

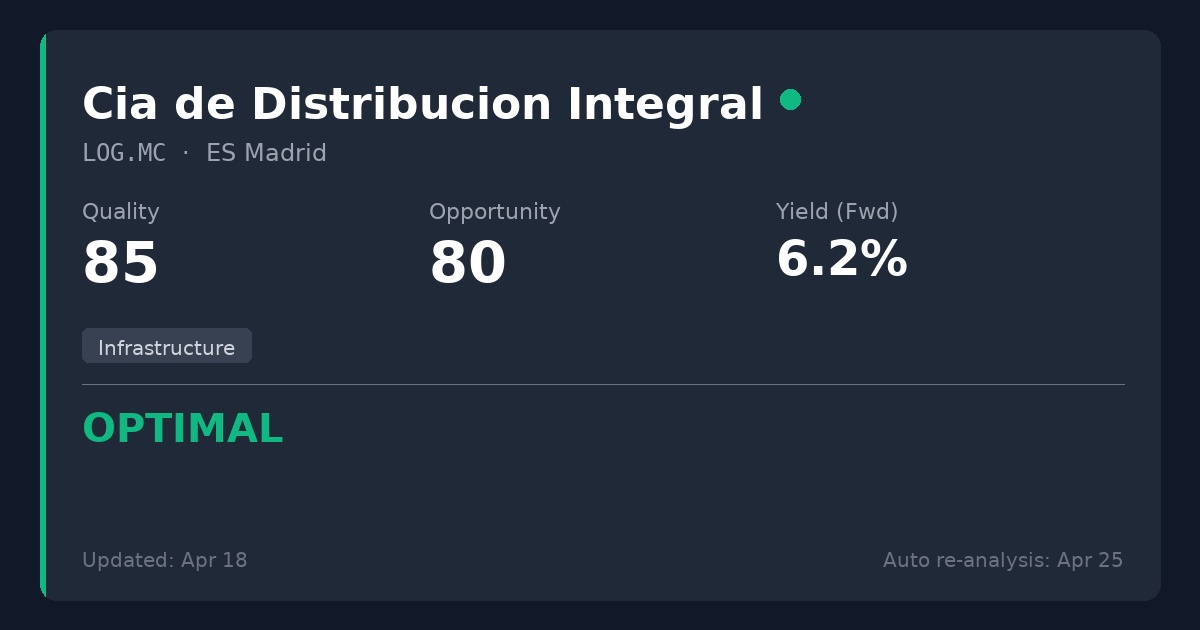

$LOG (-0,38%) (Logista):

🟢 OPTIMAL

Quality Score: 85.0/100

Opportunity Score: 80.0/100

Yield: 6.1%

P/E: 12.7x

Logista is showing a massive Opportunity Score. It trades at a highly attractive 9.9x P/FFO, putting it roughly 17% below the bottom of our fair value estimate.

It boasts a fortress balance sheet (negative Net Debt/EBITDA, meaning net cash) and a 6.1% yield that consumes only 45.9% of free cash flow. The recent collapse in global oil prices is an immediate, massive catalyst for their transportation margins.

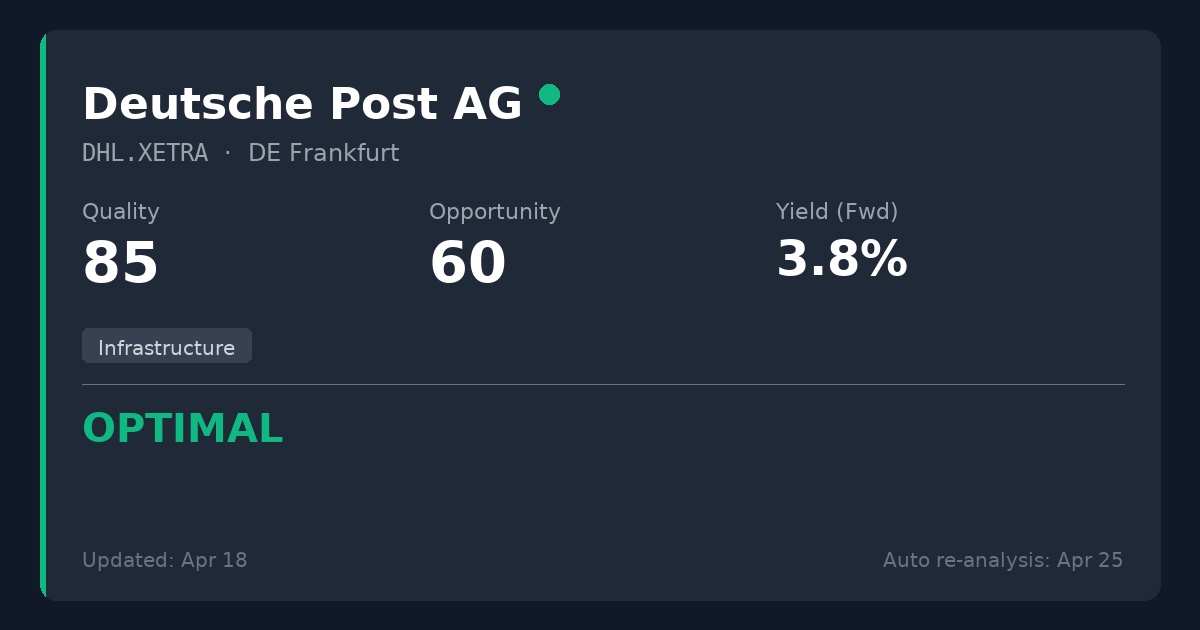

$DHL (+0,56%) (Deutsche Post):

🟢 OPTIMAL

Quality Score: 85.0/100

Opportunity Score: 60.0/100

Yield: 3.9%

P/E: 16.2x

Notice the split: the Quality is stellar, but the Opportunity score is just passing. You aren't getting a deep discount here, but you are getting a fair price.

Most screeners will warn you away from DHL right now because they show a terrifying 123% GAAP payout ratio. But when we contextualize the metrics, GAAP earnings are heavily depressed by non-cash items (D&A and remeasurements).

If we look at the actual operating cash, the FFO payout is only 16.6%. The dividend is extremely safe and well-covered by cash flow.

The market is pricing in temporary post-pandemic volume normalization and recent domestic operational complaints, suppressing the price just enough to make it a reasonable buy. You get a 3.9% yield on a global logistics oligopoly with virtually insurmountable barriers to entry.

Two logistics giants. One deep discount ($LOG), one fair price for extreme quality ($DHL).