Fanuc ($6954 (-3,81%)) is one of the world's leading automation and robotics groups - and a key strategic player in digital manufacturing, semiconductor equipment, e-mobility & logistics.

The Japanese company owns the largest installed robotics fleet in the world and dominate CNC & servo-based high-precision automation.

High barriers to entry - high moat.

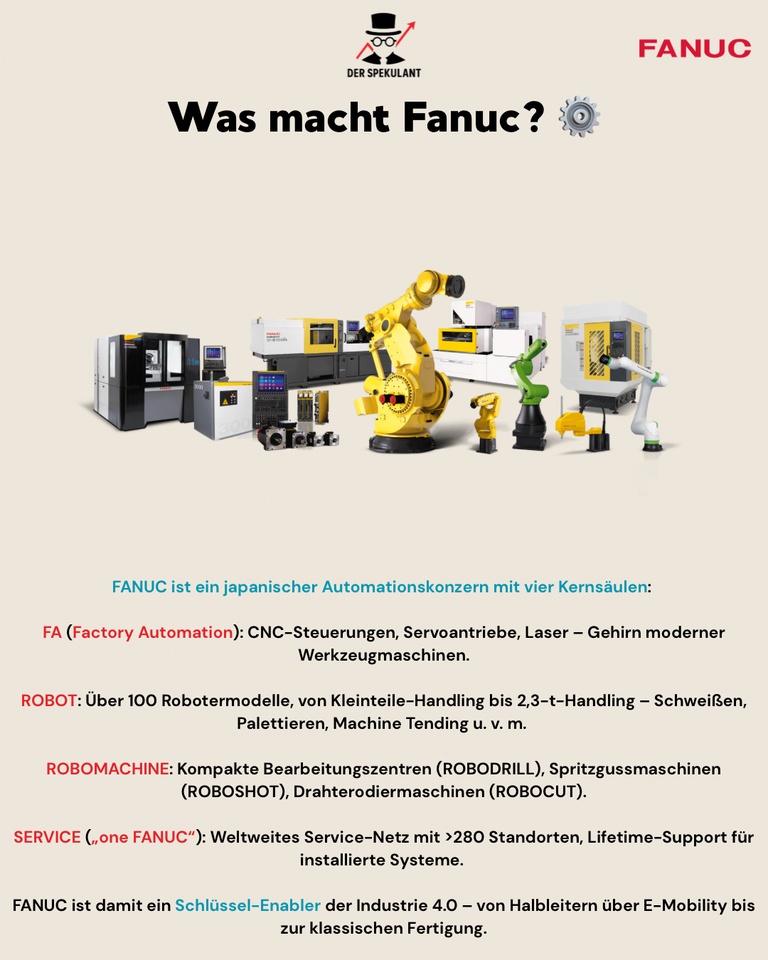

⚙️ What does Fanuc do?

➡️ Factory Automation (FA)CNC controls, servo drives, lasers - the brain of modern machine tools.

➡️ RoboticsOver 100 models - from small parts to 2.3 t handling, welding, palletizing, machine tending, etc.

➡️ RobomachineCompact machining centers (ROBODRILL), injection molding (ROBOSHOT), wire erosion (ROBOCUT).

➡️ Service - "one FANUC"Global, highly profitable lifetime service network → predictable sales.

System lock-in at the customer, as drive, controller & robot from a single source come from a single source.

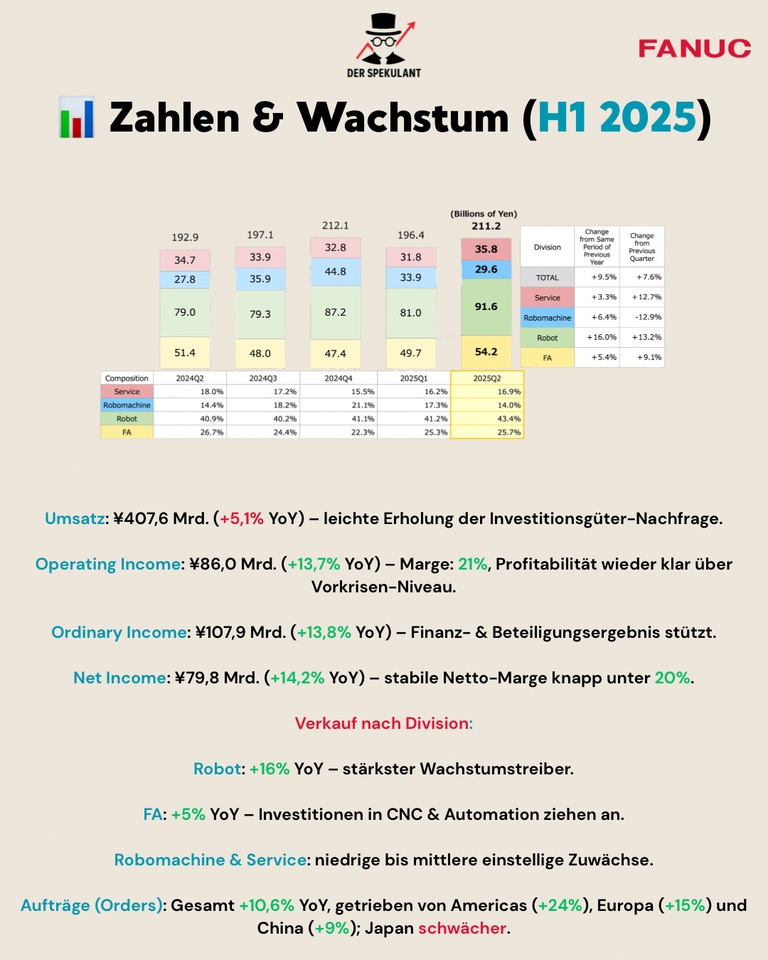

📊 Figures & growth (H1 2025)

📈 Turnover: ¥407.6 bn. (+5.1 % YoY)

Profitability picks up again significantly.

📈 Operating income: ¥86.0 bn. (+13.7% YoY) → 21 % margin

→ again clearly above pre-crisis level.

📈 Ordinary Income: ¥107.9 bn. (+13.8% YoY)

📈 Net income: ¥79.8 bn. (+14.2% YoY)

→ Net margin just under 20 %

📌 Segment driver

🔹 Robotics +16 % YoY

FA +5 % YoY

Robomachine/Service: low to mid single-digit growth rates

📌 Orders: +10.6 % YoY

Americas +24 % | Europe +15 % | China +9 % | Japan weaker

🟢 The opportunities

🟢 Automation supercycle

Labor shortage + reshoring + quality requirements → Robotics is booming.

🟢 Market leadership in robotics & CNC

Deeply integrated systems → strong customer loyalty & pricing power.

🟢 Scale & service leverage

Largest installed base worldwide → high service & spare parts share.

🟢 Exposure to high-growth sectors

Semiconductor, e-mobility, battery, logistics, consumer electronics.

🟢 Balance sheet quality

Net debt-free, high cash reserves → resilience + dividend strength.

🔴 The risks (clear & professional)

⚠️ Investment cycles in the automotive, electronics & semiconductor industries → sales & margins fluctuate.

⚠️ Project postponements lead to strong quarterly volatility.

⚠️ Regional dependency

China & Americas decisive → geopolitical risks included.

⚠️ Robotics competition

ABB, KUKA, Yaskawa & Chinese suppliers are putting pressure on prices.

⚠️ JPY risk

Strong yen can dilute profitability.

⚠️ Valuation

Quality blue chip → drop risk if growth disappoints.

💡 Conclusion & outlook

Fanuc remains a global automation champion - structurally extremely strong in the long term, cyclical in the short term.

Reshoring, AI fabs, e-mobility & logistics robots will drive growth well into the 2030s.

🎯 Long-term goal:

More service share + regional production → robust cash flows & stable margins.

📌 Investment case:

Technology leader with moat, clean balance sheet, global scale base.

But dependent on macro investment cycles in the industrial and semiconductor sectors.

💬 Community question:

Fanuc - Mandatory position in the automation portfolio or too cyclicalto be highly weighted?