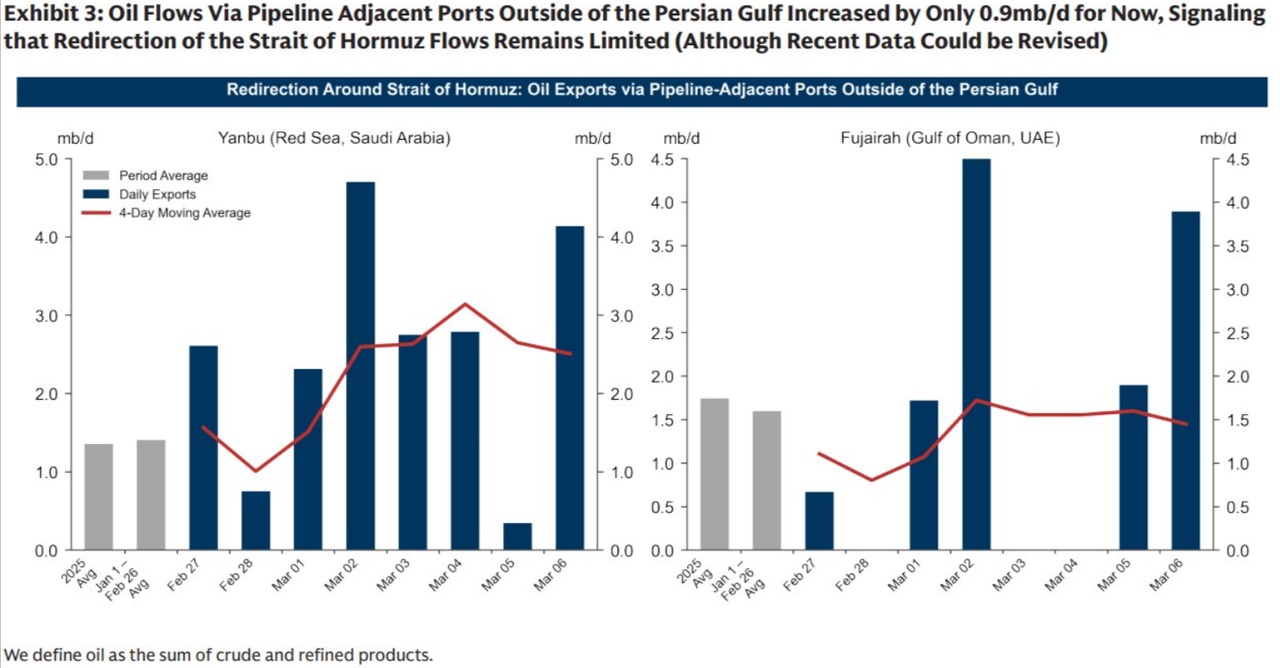

The geopolitical situation in the Middle East continues to deteriorate. According to General Cane of the US Department of War, the second phase of the war has now begun. Oil has (of course) reacted particularly to the second Iran war. In recent days, attempts have been made to transport the oil, which primarily flows through the Strait of Hormuz, via pipelines to ports such as Yanbu in Saudi Arabia or Fujairah in the UAE. The King Fahad Industrial Port in Yanbu is the largest exporter of crude oil, refined products and petrochemicals on the Red Sea with 34 berths and 10 terminals. It is used for $2222 as detour. Fujairah is a very good location for bunker oil and storage outside the Strait of Hormuz. The Fujairah Oil Terminal has 36 tanks with 1.2 million cubic meters of storage (approx. 18 million barrels) and 14 berths.

Currently, it can be stated that 4 mb/d was loaded onto VLCCs on Friday, giving a total of 8 mb/d. However, this is not in proportion to what is flowing through the Strait of Hormuz, 20 mb/d. They are currently trying to shift as much oil to ships to balance this out, but they are not succeeding. This is also due to the fact that oil storage facilities have now also become a target of the IRGC. On March 3rd, several drones hit the oil storage facility in Fujairah, which can be seen in the graphic, as no exports could take place and were still restricted on March 4th.

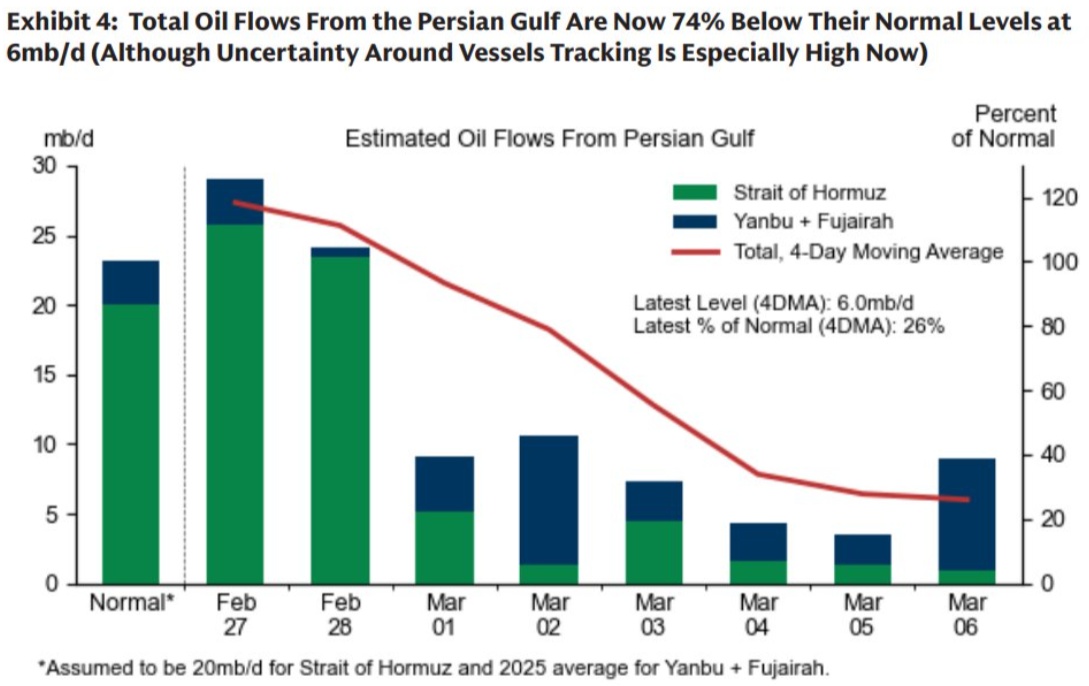

To see the extent of the current oil problem, an overview of total oil exports from the Persian Gulf is essential. This chart shows that flows have been reduced by 74%. Normally, around 20 mb/d flows through the Strait of Hormuz and 2.5 mb/d through the Yanbu and Fujaihra pipelines as a replacement/balancing valve. Due to the outbreak of war, the flow through Hormuz collapsed, partly due to fear of attacks by the IRGC and the closure by them on March 2nd (radio message).

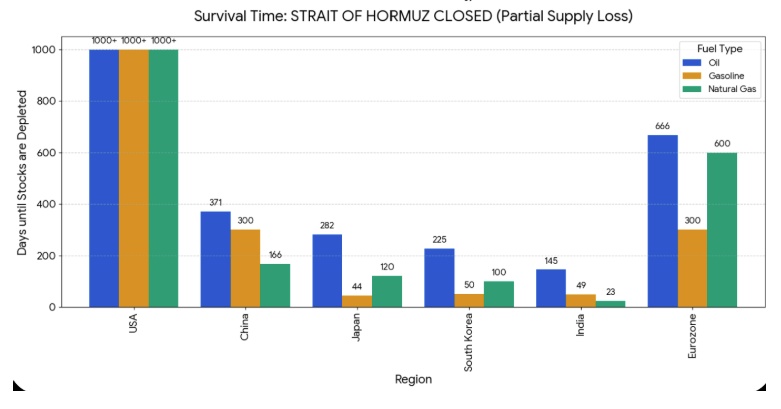

If you look at the strategic impact of a closure of the Strait of Hormuz, it hardly affects the USA, which can withstand +1000 days based on stocks. Countries in Asia, such as South Korea, Japan and to some extent China, are particularly affected, especially for gas. Europe is strategically moderately to well "prepared". The only problem is with gasoline. Those countries run the risk of having to buy expensive oil in order to maintain their normal operations.