Reading time: approx. 3-4 minutes

Amazon barely reported any profits between 2010 and 2015. The P/E ratio was in the three-digit range, at times not even meaningfully calculable. Anyone who looked at traditional valuation ratios avoided the share. And yet $AMZN (+0,86%) delivered one of the strongest returns in the entire US market during this phase.

What was actually working there?

Not the distribution, there was none. Nor was it a simple revaluation. Above all, something more fundamental: the market priced in profit growth that was not yet visible but was then delivered, driven primarily by AWS and the margin shift in the retail business. Those who understood this early on did not look at the current P/E ratio. They asked what the company would earn in five years' time.

That sounds simple. It is not.

Profit growth as a driver of returns only works under certain conditions.

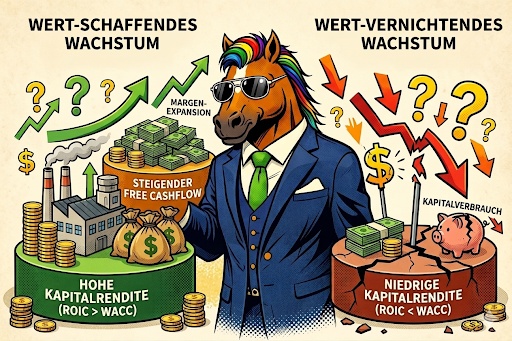

The most important one is that the return on invested capital must be above the cost of capital. Growth without this condition does not create value, it destroys it. That sounds trivial. But it is surprisingly often ignored.

Then there is the question of the margin structure. Expansion must be built into the business model, not into the economic upswing.

And the addressable market must be large enough to keep the growth window open. Short-term growth in a small market is not a profit driver.

Amazon fulfilled all three conditions. Between $META (+1,76%) between 2022 and 2024, it was a different path, but the same mechanism. No long reinvestment cycle, but a hard efficiency cut. The operating margin rose from under 20 percent to over 35 percent in two years. Free cash flow has more than doubled. Multiple expansion has helped, but the key driver has been a massive increase in profits.

The opposite is just as instructive.

$SNAP (+2,28%) had real user growth. The revenue curve was impressive. But the company never structurally achieved a return on capital above the cost of capital. The growth consumed capital without increasing it. Today, the share is trading well below the IPO price. $ZAL (+5,59%) is the European equivalent. Sales multiplied, return on capital sobering, free cash flow weak, share price sideways for years.

Both companies have grown. Neither has created value.

Before I invest in a company where profit growth is a key driver of returns, I go through a few questions.

Is the ROIC above the cost of capital, ideally over 15% in my estimation?

Is the free cash flow growing faster than sales, which indicates operating leverage?

Is the margin path concretely comprehensible or only vaguely promised?

And is the addressable market sufficient for at least five to ten years?

On the other hand, if sales are growing but free cash flow is stagnating, this is a clear warning signal. The same applies if ROIC remains below the cost of capital despite years of investment, or if growth is financed through dilution.

The key figures themselves are public.

Something else is more difficult: trusting the mechanism in a situation like Amazon 2012 or Meta 2022 when it is barely visible in the current figures. This is not a question of analysis. It is a question of conviction.

The next article is about what happens when neither profit growth nor multiple expansion clearly dominate. And why understanding the cycle makes all the difference in such phases.