Hello my dears,

Perhaps some of you noticed yesterday.

The two prompts Antonio and Augustus had a heated duel here.

Towards the end, I couldn't keep up either and lost my perspective. I'm sure many of you felt the same way, and my thought was that two business professors were engaged in a dialog.

That's why I tasked my little Prompt student Juan with making the analysis as comprehensible as possible for our community.

Constructive criticism is welcome in the comments, and Juan would be delighted.

But now to our presentation. If you think the AI revolution is only taking place in the USA and Asia, I'd like to prove you wrong today.

Although European companies are rarely cited as the first beneficiaries of the AI boom, Morgan Stanley sees a structural misjudgment of the market here.

The continent is particularly strongly positioned in upstream areas of the value chain - such as special materials for photonic chips, semiconductor packaging or long-haul optical networks between data centers.

The direct revenue share of these activities is still relatively small. However, as optical technologies become more widespread, these areas could become important growth drivers. This is precisely where the analysts see the opportunity for revaluations on the stock market.

Against this backdrop, Morgan Stanley names particularly interesting stocks, such as STMicro, which investors could use to position themselves in this trend.

Morgan Stanley ultimately prefers companies that are involved in the areas of silicon photonics, packaging and the broader network expansion. The US institute does this by recommending Nokia, Soitec, STMicroelectronics and Besi, which are seen as the most attractive listed opportunities to participate in the European optical technology market.

Photonic integration as a new growth driver

STMicroelectronics is another beneficiary of the trend towards optical data transmission. The focus here is on the PIC100 platform, which serves as the basis for photonic integration and should give the company access to the rapidly growing market for optical data connections.

Morgan Stanley expects particularly dynamic growth here. Sales of PIC and EIC components could grow at an annual rate of around 115% between 2026 and 2028.

Technologically, STMicroelectronics benefits from the use of modern 300 mm wafers, which offer significant advantages in terms of scaling and costs compared to older 200 mm standards. In addition, there are higher chip yields, better process control and lower costs per function - all factors that are crucial for hyperscalers.

STMicroelectronics

Is part of the megatrends data centers, humanoids and space!

I believe that the STMicro share can continue to establish an upward trend. With a PER27e of only 17.7 and a P/E ratio of 2, the valuation is moderate. Addressing three future megatrends at once offers the potential for surprises and thus the opportunity for further price increases based on the current valuation. 1. space: STMicro is a supplier to SpaceX. The BiCMOS-based radio front-end modules, which are installed in the Starlink user terminals and deliver high data rates in extreme environmental conditions, are particularly important.

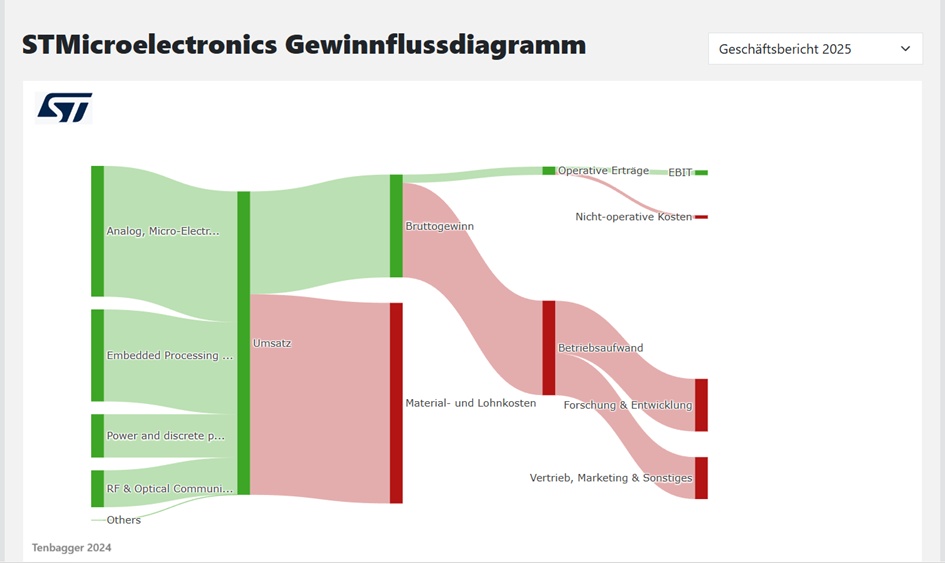

With over 48,000 semiconductor technology designers and manufacturers mastering the semiconductor supply chain in state-of-the-art manufacturing facilities, STMicroelectronics N.V. is an integrated device manufacturer working with more than 200,000 customers and thousands of partners to design and develop products, solutions and ecosystems that address their challenges and opportunities and the need to support a more sustainable world. The Group's technologies enable smarter mobility, more efficient power and energy management and the large-scale deployment of cloud-connected autonomous devices.

Number of employees: 49,157

STMicro: The new collaboration with AWS makes the chip manufacturer a beneficiary of the USD 200 billion capex offensive. Chart breakout!

09.02.26

New billion-dollar pact with AWS

The multi-year extension of the cooperation with AWS announced today marks a milestone. STMicro will act as a strategic key supplier for AWS' compute infrastructure, delivering a broad range of proprietary technologies. The focus is on specialized solutions for high-bandwidth connectivity, high-performance mixed-signal processing and advanced microcontrollers for intelligent management of the physical infrastructure. In addition, AWS integrates analog and power ICs from STMicro to achieve the necessary energy efficiency for the operation of huge server farms. These hardware deliveries are flanked by the optimization of design processes (EDA) in the cloud, which massively accelerates the market launch of new chip generations. The partnership is financially secured by a volume in the billions and the issue of 24.8 million warrants to AWS.

Nvidia enters into humanoid robot partnerships with European chip manufacturers

16,03,2026

US chipmaker Nvidia coordinated the announcements on the eve of the annual GPU Technology Conference in California, where efforts to become the "brain" or central computing platform for robots with its Jetson Thor processors are likely to be a focus.

- Nvidia partners with Infineon, NXP and STMicroelectronics for humanoid robot hardware

- The humanoid robot market is expected to sell over 50,000 units this year

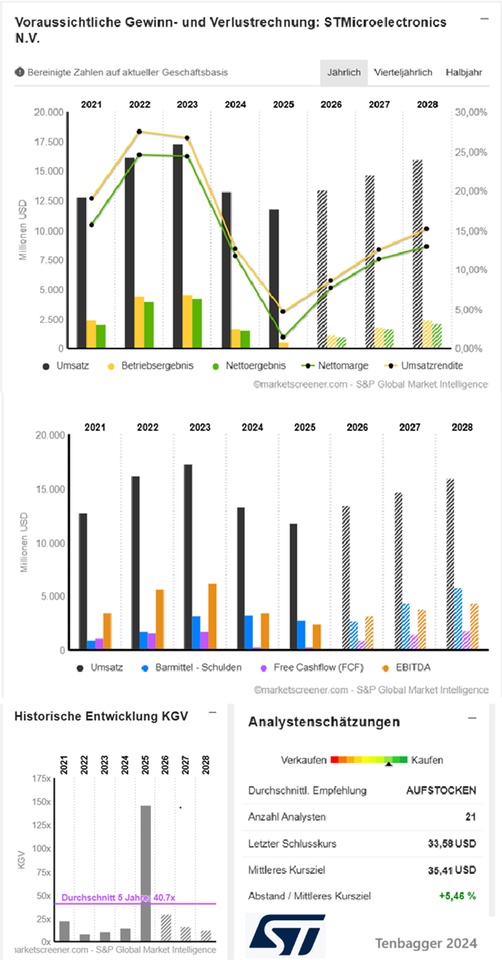

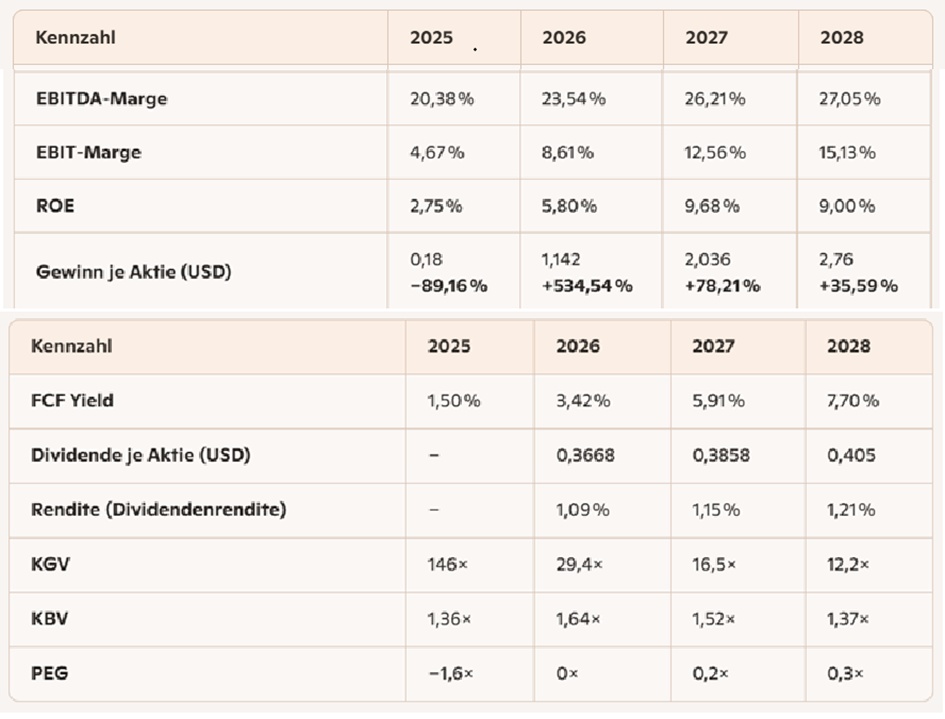

⭐ Overall assessment of key financial figures (2025-2028)

(Based on the MarketScreener forecasts)

🟩 1. growth: sales & earnings development

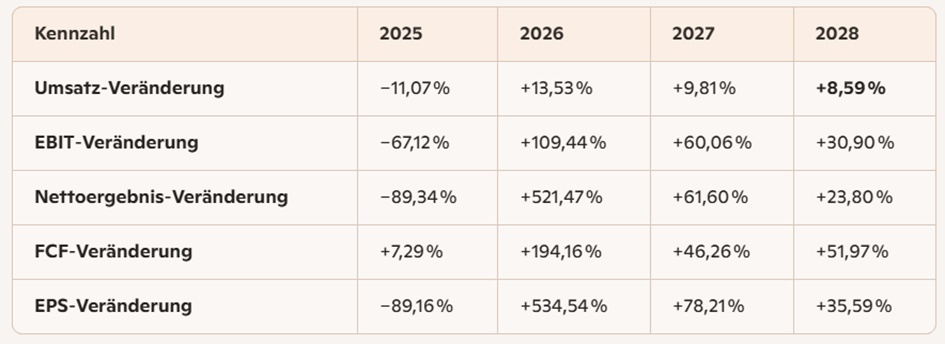

Turnover: 2025 → 2028: 11,800 → USD 15,976 million → Solid, steady growth.

EBIT: 2025 → 2028: 551 → USD 2,418 million → EBIT almost quadruples.

Net result: 2025 → 2028: 166 → USD 2,064 million → Extremely strong recovery after the cyclical slump in 2024.

🔍 Valuation

- The company is growing not only growing againbut disproportionately profitable.

- Margins are increasing in parallel → Quality growth, not pure sales growth.

- The growth in earnings is significantly stronger than the increase in saleswhich indicates operating leverage.

🟩 2. profitability: margins improve strongly

EBITDA margin: 2025 → 2028: 20,38 % → 27,05 %

EBIT margin: 2025 → 2028: 4,67 % → 15,13 %

🔍 Valuation

- The margins increase every year.

- EBIT margin triples → sign of:

- better capacity utilization

- higher quality product mix

- economies of scale

- For a semiconductor manufacturer, an EBIT margin >15 % is very strong.

(My dear, even if my two friends the prompts (@Raketentoni

@Get_Rich_or_Die_Tryin ), will tear the company apart because of the margins. I also see potential in the fact that there is still room for improvement).

🟩 3rd cash flow: FCF explodes

Free cash flow: 2025 → 2028: 309 → USD 2,020 million

FCF change: 2026: +194 % 2027: +46 % 2028: +52 %

🔍 Valuation

- The FCF grows faster than sales & EBIT.

- The company is becoming cash-strongwhich means:

- dividends

- share buybacks

- CAPEX

- Debt reduction supported.

- The FCF yield rises to 7,7 % → highly attractive.

🟩 4th balance sheet: net debt continues to fall

Net debt: 2025 → 2028: -2,789 → -5,858 million USD

🔍 Valuation

- STMicroelectronics is net debt-free and is further expanding its cash position.

- Negative net debt in this amount is a massive stabilizing factor.

- In a cyclical industry, this is a strategic advantage.

🟩 5. return on investment: ROE increases

ROE: 2025 → 2028: 2,75 % → 9,00 %

🔍 Valuation

- The ROE is rising continuously.

- 9% is solid, but not yet top class.

- However, the trend is clearly positive → Efficiency is increasing.

(Here, too, the prompts (@Raketentoni

@Get_Rich_or_Die_Tryin) not be so optimistic and crumble the ROE with the Hamer).

🔍 Rating

- Extremely solid balance sheet.

- Very low risk of interest rate rises.

- High flexibility for investments.

🟩 2nd P/E ratio falls dramatically - valuation becomes more favorable

2025 → 2028: 146× → 12,2×

This is one of the strongest positive points.

Why positive?

- A falling P/E ratio combined with rising profits means: 👉 The share is becoming fundamentally more favorablenot because it is falling, but because profits are exploding.

- A P/E ratio of 12.2× in 2028 is below average for a semiconductor manufacturer is below average.

PEG ratio improves significantly 3.

2025: -1,6× → 2028: 0,3×

Why positive?

- A PEG < 1 means: 👉 The earnings growth is higher than the valuation.

- A PEG of 0.3× is extremely attractive and indicates an undervaluation undervaluation.

🟩 4th dividend grows moderately and stably

2026 → 2028: 0.3668 → 0.405 USD

Why positive?

- STMicroelectronics remains dividend stabledespite the cyclical semiconductor industry.

- The payout ratio will fall to 14,7 %which means: 👉 The dividend is very well secured. 👉 Plenty of cash remains for growth and investments.

🟩 5th dividend yield increases slightly

2026 → 2028: 1,09 % → 1,21 %

Why positive?

- The yield increases even though the share price remains stable (reference price USD 33.58).

- This shows: 👉 The dividend is growing disproportionately to the share price.

(And of course the dividend will also fall through the cracks with Mr. Antonio Prompt). @Raketentoni

🟩 6th P/B ratio falls - share becomes more favorable in balance sheet terms

2025 → 2028: 1.36× → 1.37× (slightly rising, but low)

Why positive?

- A P/B ratio of 1.3× is unusually low for a semiconductor stock unusually low.

- This signals: 👉 The share is not overvalued. 👉 The market is pricing in risks that are not covered by the fundamentals.

🟩 1st FCF yield is rising strongly and continuously

2025 → 2028: 1,5 % → 7,7 % That is a massive leap.

Why positive?

- A rising FCF yield means: 👉 The company is generating more and more free cash flow per market capitalization.

- 7.7 % is very attractive for a semiconductor stock very attractive.

- This indicates operational strength and cash flow efficiency efficiency.

In sum: STMicroelectronics shows a combination of growth, cash flow strength and a declining valuationwhich is rare in the semiconductor industry.

⭐ Overall assessment:

STMicroelectronics shows between 2025-2028 an exceptionally strong foundation:

- Growth + margins + cash flow + balance sheet strength

- and at the same time declining valuation (P/E ratio, PEG, FCF yield).

This is a combination that is rarely seen in the semiconductor industry. rarely found in the semiconductor industry.