What's actually going on with $AMD (+2,94%)

$NVDA (+1,47%)

$ASML (+2,45%) and all that? Started off strong today but faded badly

ASML

Ação

Ação

ISIN: NL0010273215

Ticker: ASML

NL0010273215

ASML

Price

Discussão sobre ASML

Postos

696

1Semana·

My next purchase?!

First, I’d like to officially @Tenbagger2024 officially welcome back from the sidelines! 🫡 It’s great to have you back!

I hope you were able to enjoy your time off, recharge your batteries 🪫, and return with new energy 🔋 and your usual strength 💪. The community has definitely missed a familiar name—without your insights and analyses, things here were almost a little too quiet. 🙇♂️

And what can I say: Your comeback came even faster than that of the German national soccer team after their latest setbacks—so the bar wasn’t set too high. 😂⚽

With that in mind: Welcome back, my friend! I’m excited to see which companies you’ll pull out of your sleeve this time and which candidates will once again be scrutinized mercilessly. 💀

————————————————————————-

While the market focuses its attention on the usual suspects, there are always companies that fly largely under the radar. One such candidate has been on my watchlist for quite some time and is now on the verge of making the leap into my portfolio.

Today, I’d like to show you why I consider this company (another stock from Japan) to be an extremely exciting investment candidate.

Today’s focus is on Hoya Corp $7741 (-0,21%)

HOYA Corp.: The Invisible Monopoly of the Optics & Chip World

While the stock market is fixated on $ASML (+2,45%) ASML’s EUV lithography machines or the mass production of wafers by $2330 , a Japanese heavyweight has established itself in the shadow of the tech giants—one without which not a single sub-3nm processor can be manufactured in the age of AI and semiconductors: HOYA Corporation. $7741 (-0,21%)

HOYA $7741 (-0,21%) does not manufacture finished microchips or hospital diagnostic devices. HOYA $7741 (-0,21%) supplies the physically perfect, high-precision materials upon which all global progress in the chip industry and medical technology is built.

The difference from ordinary suppliers is enormous: HOYA $7741 (-0,21%) combines the explosive, high-margin growth of the AI and semiconductor sectors with the crisis resilience of a global medical technology monopoly.

1. The Business Model: The Highly Profitable Dual Engine ⚙️👁️

HOYA $7741 (-0,21%) scales through a perfectly balanced two-pillar model that hedges the cyclical dynamics of the tech world with defensive healthcare cash flows:

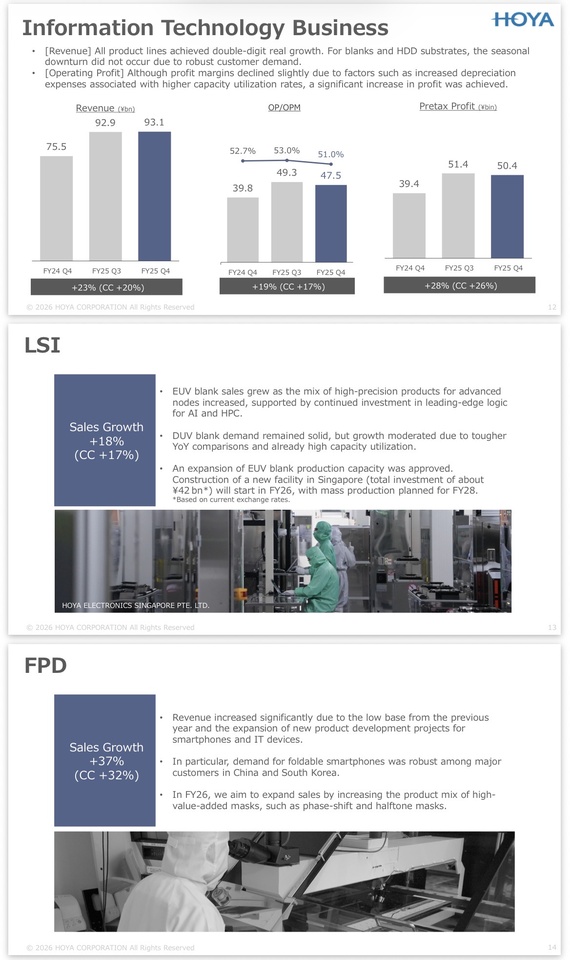

① Information Technology (IT) Segment (~46–48% of revenue):

- EUV Photomask Blanks: High-purity quartz glass blanks that serve as photomasks for the most advanced chip manufacturers (sub-3nm, high-NA EUV). HOYA $7741 (-0,21%) holds a virtual global monopoly in this sector (>80% market share).

- HDD Glass Substrates: Ultra-flat glass substrates for high-capacity hard disk drives in data centers. Glass enables higher storage densities than aluminum—essential for the data deluge generated by AI hyperscalers.

- Operating Margin: A staggering ~54.1%! This segment is a true money-making machine that benefits directly from the AI and semiconductor boom.

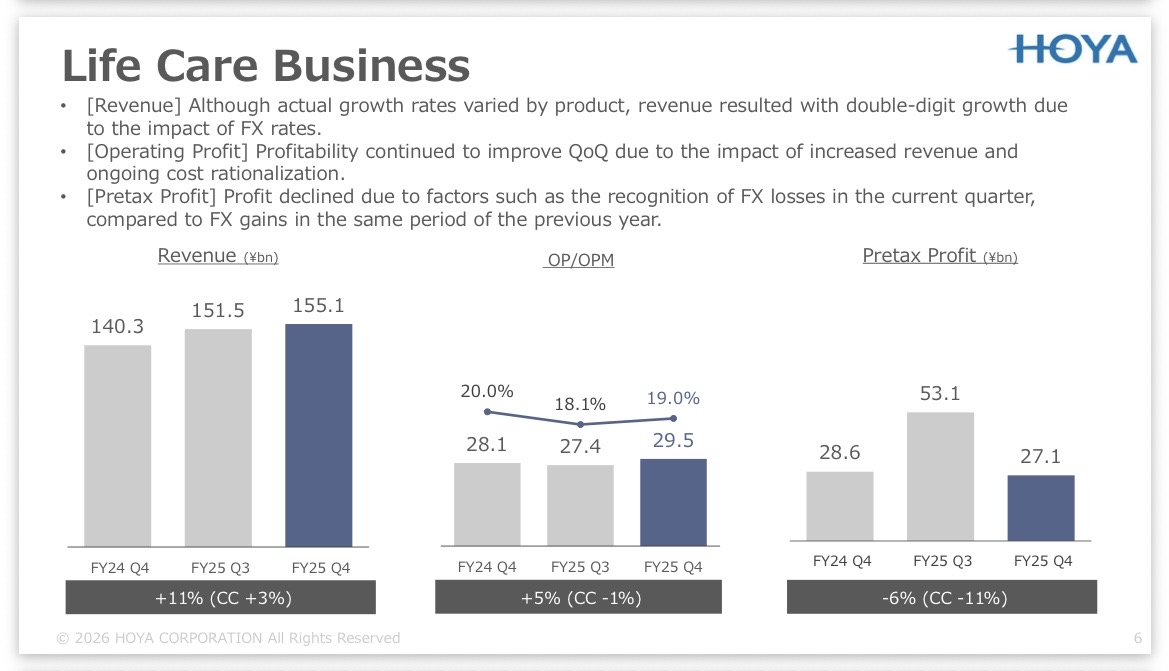

② Life Care Segment (~52–54% of revenue):

- Products: Optometry (eyeglass lenses, contact lenses) and MedTech (PENTAX endoscopes, intraocular lenses for cataracts).

- Operating Margin: Extremely solid ~18.1%.

- Competitive advantage: Provides a crisis-resistant, non-cyclical foundation. Even if the semiconductor industry stagnates, people will still undergo eye surgeries and purchase vision aids.

2. The Technology: Why Sub-3nm & AI Data Centers Would Fail Without HOYA

HOYA’s unique physical selling point $7741 (-0,21%) lies in its its mastery of glass and materials science at the nanometer scale. Two key drivers make HOYA $7741 (-0,21%) indispensable:

- EUV lithography & high-NA EUV: When exposing state-of-the-art chips with extreme ultraviolet (EUV) light, the photomask must be free of any molecular deviations. A tiny defect on the mask can ruin millions of chips. HOYA’s blank materials offer a defect density close to zero. Without HOYA, $7741 (-0,21%) , there would be no yield for $AAPL (-0,52%) Apple Silicon, $NVDA (+1,47%) Nvidia GPUs, or $AMD (+2,94%) AMD processors.

- HDD glass substrates for AI data centers: Cloud storage space is growing exponentially. Conventional aluminum platters in hard drives bend under extremely high rotational speeds and multiple layers. HOYA’s specialty glass is stiffer, flatter, and enables significantly higher storage capacities per hard drive.

The Validation Moat: Just as with tooling suppliers, the approval of a new mask blank or glass substrate at TSMC $2330 , Samsung $005930 or Intel $INTC (+2,11%) is a multi-year qualification process. The switching costs for chip manufacturers are immense.

3. Geographic Distribution: Global Players with Little Home Bias 🌍

HOYA $7741 (-0,21%) is listed in Tokyo, but generates just under 85–88% of its revenue abroad. This provides protection against Japan’s domestic demographic trends and yields massive currency advantages when the yen is weak:

REGION :

🇹🇼🇰🇷🇨🇳ASIA/China

Revenue share: ~35%–38%

Key drivers: semiconductor foundries (TSMC, $2330 Samsung $005930 ) IT packaging hubs

🇪🇺Europe

~28%–30%

Strong life care medtech business (eyewear & endoscopes)

🇺🇸North America

~20%–22%

Data center hyperscalers & U.S. chip design (EUV/HDDS)

🇯🇵Japan

~12%–14%

Medtech sales & optical R&D/manufacturing sites

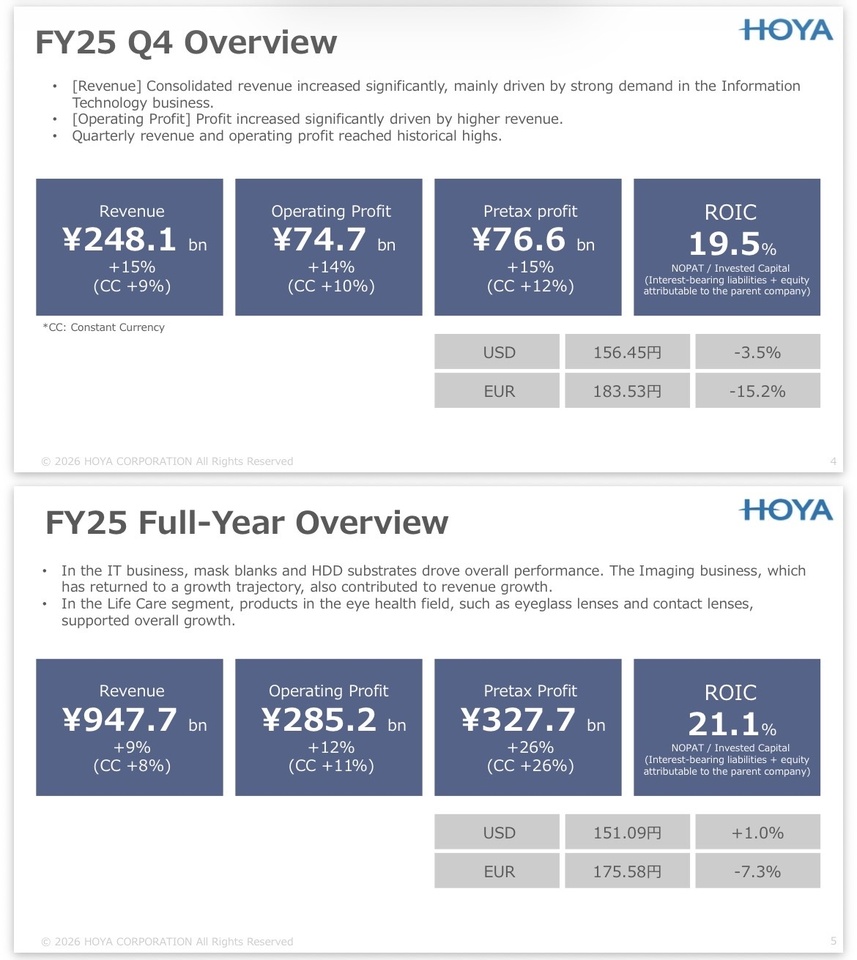

4. Key Financial Metrics (Fundamental Analysis & Financial DNA) 📊

- Market Capitalization: ~6.8 to 7.2 trillion JPY (approx. 42–45 billion EUR) – A true global tech/medtech mega-cap on the Tokyo Stock Exchange.

- Revenue Growth (Segment Dynamics):

- IT segment:

+36% YoY (strongly driven by EUV blanks and AI-driven HDD demand). - Life Care Segment:

+9% YoY (stable, non-cyclical anchor). - Consolidated EBIT margin:

~35–38% – Due to the IT division’s high profit contribution (54.1% margin), the overall performance is on par with the software sector. - Return on Invested Capital (ROIC):

>22% – Indicates excellent opportunities for reinvestment and high capital efficiency. - Free Cash Flow Margin:

>22% – HOYA $7741 (-0,21%) consistently converts operating profits into true FCF. - Balance Sheet Strength: Net debt/EBITDA is negative (net cash). HOYA $7741 (-0,21%) has an extremely large cash reserve and faces absolutely no refinancing risk.

5. Why is this stock exciting? 🚀

The undisputed “hockey stick” segment (EUV boom): As the chip industry switches to high-NA EUV machines from ASML, the demand for even more precise mask blanks is rising dramatically. HOYA $7741 (-0,21%) benefits from every technological leap in the semiconductor industry.

Defensive safety net: If the semiconductor market enters a cyclical correction, the defensive MedTech segment (Life Care) cushions the valuation and ensures rock-solid cash flows.

At the heart of the AI infrastructure hub: HOYA $7741 (-0,21%) benefits twice when it comes to AI: once through the production of logic chips (EUV) and once through the storage of massive amounts of AI data (HDD glass substrates).

6. Risks ⚠️

- Geopolitics in East Asia: Since the majority of the IT business is handled by foundries in Taiwan 🇹🇼 and South Korea 🇰🇷, there is a significant concentration risk in the event of a China-Taiwan conflict.

- U.S. Export Restrictions: Tighter U.S. sanctions against the Chinese chip industry could dampen shipments of high-end substrates and blanks.

- Exchange rate sensitivity (JPY): As a highly export-oriented company (85–88% of revenue from overseas), a sudden appreciation of the yen leads to foreign exchange losses on the balance sheet.

🎯 EARNINGS PREP: What to watch for in the next earnings report?

The upcoming quarterly results (Q1 of fiscal year 2027) from HOYA Corp. are just around the corner:

📅 Date:

Thursday, July 30, 2026 (or July 31, depending on the time zone)

⏱ Time: HOYA typically publishes $7741 (-0,21%) releases its results around 1:30 p.m. JST (approx. 6:30 a.m. German time).

📊 Reporting Period: Just-ended first quarter (3 months ending June 30, 2026).

💡 Analyst expectations (consensus)

Revenue: ~$1.55 to $1.57 billion (driven largely by continued demand in the IT/EUV segment).

Earnings per Share (EPS): ~$1.15

For the upcoming earnings update, the key metrics will primarily focus on the IT division and margin trends. The following points should be on your radar:

1.🎭 EUV & High-NA Blank Volume: Will the strong year-over-year growth in the IT segment (+36%) be confirmed? Pay attention to statements regarding the ramp-up of high-NA EUV photomasks at TSMC and Intel.

2.🏭 HDD Glass Substrate Demand (Hyperscaler Capex): Will call-off volumes for glass substrates continue to rise due to AI data center expansion? This is the second major driver in the IT sector.

3. 🤖Margin Stability in the IT Segment: Can the operating margin in the IT sector hold at the extremely high level of >54% , or will R&D costs for the next sub-2nm generations put pressure on profitability in the short term?

4.🩺 Life Care Stability Check: Will the MedTech segment maintain its steady currency-adjusted growth of ~8–9% YoY with an operating margin of just under ~18%? (Any deviation would indicate weaknesses in the end-consumer market for eyeglass lenses).

5. 💴Yen Effect (FX Tailwinds/Headwinds): To what extent does the exchange rate distort the reported JPY figures compared to organic growth abroad (85–88% of revenue generated overseas)?

My Personal Conclusion & Reaper Rating 🧐

I find that Hoya Corp. $7741 (-0,21%) has been incredibly exciting for quite some time now. To me, the company is the textbook example of a perfect hybrid model: On the one hand, it has a virtually irreplaceable monopoly business that supplies an essential key component for the world’s most advanced semiconductors. On the other hand, the strong, defensive medtech business, with its crisis-proof margins, provides stability that excellently cushions the cyclical fluctuations of the semiconductor sector.

It’s precisely this combination that makes Hoya $7741 (-0,21%) so extraordinary to me. The company combines enormous structural growth with a defensive quality that is extremely rare to find in this form.

Of course, Hoya $7741 (-0,21%) still highly valued, no question about it. However, the stock has already pulled back a bit from its ATH, thereby reducing part of its ambitious valuation. For me, this currently presents an exciting opportunity to gradually build a position in a company that’s been on my watchlist for a long time 👀🙇♂️

💀Jack’s Verdict:

Jack’s Take: “If you’re looking for the perfect CRV on the stock market, sooner or later you’ll end up at HOYA. While the masses, in search of the next hype, are chasing after every shovel seller, HOYA holds the monopoly on the specialty glass from which the shovels are forged in the first place.

With the AI and high-NA EUV boom in full swing, the IT division is raking in profits thanks to >54% margin , it’s printing money like a printing press. If the semiconductor cycle stutters briefly, HOYA remains completely unfazed and continues to sell millions of eyeglass lenses, endoscopes, and cataract lenses. You’re not buying a highly speculative tech bet here, but a highly profitable, net-debt-free fortress with a built-in airbag.”

- REAPER RATING: 🟢 BUY (Quality Compounder)

- REAPER SCORE:

8/10 · Anchor 7–9 (Monopoly-like dual compounder)

@Get_Rich_or_Die_Tryin

@Tenbagger2024

@Raketentoni

@PikaPika0105

@Stocktective

@schlimmschlimm

@Multibagger

@Dividendenopi

@Simpson and, of course, all the others ✌️

+ 5

2727

18 Comentários

1Semana

Hey Brian!

Great post and a top-notch analysis! You’ve definitely unearthed an absolutely fascinating stock that many investors haven’t even noticed on the market.

Since you’re explicitly asking for opinions, here’s my usual dose of straight talk:

I ran your theses through our data scanner and compared them with the raw financial statements.

Here’s the unvarnished feedback—what hits the nail on the head, where you’re looking through rose-colored glasses, and what the numbers really say.

### 👍 Where you’re absolutely spot on (The Praise)

1. **The moat is impressive:** Your description of the business model is spot on. With a market share of over 80% in EUV photomask blanks, Hoya effectively holds a global monopoly on sub-3nm processors. Anyone looking to shape the future of semiconductors (TSMC, Nvidia, Apple) simply can’t get around Hoya.

2. **The dual-engine principle:** The combination of a high-margin tech division (EUV & HDD glass) and a crisis-resistant medtech business (endoscopes, eyeglass lenses) is textbook perfect.

3. **A balance sheet as solid as granite:** Your statement on debt is exactly right. According to our current data, the net debt-to-total-capital ratio stands at **-6.2%**. The company is sitting on a massive cash pile and is completely debt-free on a net basis.

### ⚠️ The Reality Check (Where You’re Wrong / What You’re Overlooking)

As brilliant as the company is from an operational standpoint:

When looking at the valuation and current key metrics, I’m afraid I have to seriously rain on your parade.

You’re brushing off the valuation a bit too casually with *“come back a bit”*.

Here are the hard facts from the engine room:

* **The Valuation Monster (P/E ratio 33.6x):**

Hoya is currently trading at a **P/E ratio of 33.6** and a **price-to-book ratio (P/B) of a whopping 8.3x**.

The group’s overall growth on an LTM basis currently stands at **9.4%**. A P/E ratio of 33 for single-digit to just under double-digit overall growth is incredibly ambitious.

There’s absolutely zero margin for disappointment priced in.

* **Fair value points downward:**

Our data models (12 different financial models) currently indicate a fair value of **$137.49** for the stock.

At a current price of **158.03 USD**, this implies a downside potential of **-13.0%**.

In the quality check, the “Relative Value” score therefore only manages a meager **1.4 out of 5 points** (red zone).

* **Margin slightly overestimated:**

You mention a consolidated EBIT margin of 35–38%. The actual total figure currently stands at a very strong, but slightly lower, **32.4%**.

* **Significant underperformance within the sector:**

Looking at performance over the last 12 months, Hoya has **+20.45%**, but it lags miles behind its direct semiconductor and tech benchmarks (**+92.59%**).

Why?

Because the market clearly sees that, in terms of valuation, the stock is simply stuck at the upper limit.

---

### 🎯 RaketenToni’s Conclusion

Hoya Corp is the prime example of a **top-tier quality company with an outrageously expensive price tag**.

There’s no doubt you’re buying one of the world’s strongest material companies here. But at the current price of about $158, you’re not buying any margin of safety.

**My verdict:**

Anyone who goes all-in on Hoya now, ahead of the July 31 earnings report, is betting that the company will once again shatter the already extremely high expectations in the IT segment.

For the watchlist, this stock gets a solid 10/10.

For a direct purchase, I’d either start with just a tiny initial position or simply wait and see if the earnings release at the end of July triggers a pullback toward the fair value (135–140 USD).

Quality comes at a price—but you don’t have to pay for it at its absolute peak!

Great post and a top-notch analysis! You’ve definitely unearthed an absolutely fascinating stock that many investors haven’t even noticed on the market.

Since you’re explicitly asking for opinions, here’s my usual dose of straight talk:

I ran your theses through our data scanner and compared them with the raw financial statements.

Here’s the unvarnished feedback—what hits the nail on the head, where you’re looking through rose-colored glasses, and what the numbers really say.

### 👍 Where you’re absolutely spot on (The Praise)

1. **The moat is impressive:** Your description of the business model is spot on. With a market share of over 80% in EUV photomask blanks, Hoya effectively holds a global monopoly on sub-3nm processors. Anyone looking to shape the future of semiconductors (TSMC, Nvidia, Apple) simply can’t get around Hoya.

2. **The dual-engine principle:** The combination of a high-margin tech division (EUV & HDD glass) and a crisis-resistant medtech business (endoscopes, eyeglass lenses) is textbook perfect.

3. **A balance sheet as solid as granite:** Your statement on debt is exactly right. According to our current data, the net debt-to-total-capital ratio stands at **-6.2%**. The company is sitting on a massive cash pile and is completely debt-free on a net basis.

### ⚠️ The Reality Check (Where You’re Wrong / What You’re Overlooking)

As brilliant as the company is from an operational standpoint:

When looking at the valuation and current key metrics, I’m afraid I have to seriously rain on your parade.

You’re brushing off the valuation a bit too casually with *“come back a bit”*.

Here are the hard facts from the engine room:

* **The Valuation Monster (P/E ratio 33.6x):**

Hoya is currently trading at a **P/E ratio of 33.6** and a **price-to-book ratio (P/B) of a whopping 8.3x**.

The group’s overall growth on an LTM basis currently stands at **9.4%**. A P/E ratio of 33 for single-digit to just under double-digit overall growth is incredibly ambitious.

There’s absolutely zero margin for disappointment priced in.

* **Fair value points downward:**

Our data models (12 different financial models) currently indicate a fair value of **$137.49** for the stock.

At a current price of **158.03 USD**, this implies a downside potential of **-13.0%**.

In the quality check, the “Relative Value” score therefore only manages a meager **1.4 out of 5 points** (red zone).

* **Margin slightly overestimated:**

You mention a consolidated EBIT margin of 35–38%. The actual total figure currently stands at a very strong, but slightly lower, **32.4%**.

* **Significant underperformance within the sector:**

Looking at performance over the last 12 months, Hoya has **+20.45%**, but it lags miles behind its direct semiconductor and tech benchmarks (**+92.59%**).

Why?

Because the market clearly sees that, in terms of valuation, the stock is simply stuck at the upper limit.

---

### 🎯 RaketenToni’s Conclusion

Hoya Corp is the prime example of a **top-tier quality company with an outrageously expensive price tag**.

There’s no doubt you’re buying one of the world’s strongest material companies here. But at the current price of about $158, you’re not buying any margin of safety.

**My verdict:**

Anyone who goes all-in on Hoya now, ahead of the July 31 earnings report, is betting that the company will once again shatter the already extremely high expectations in the IT segment.

For the watchlist, this stock gets a solid 10/10.

For a direct purchase, I’d either start with just a tiny initial position or simply wait and see if the earnings release at the end of July triggers a pullback toward the fair value (135–140 USD).

Quality comes at a price—but you don’t have to pay for it at its absolute peak!

•

77

•

1Semana·

ASML: A Brilliant Quarter — But Is Now the Right Time to Buy?

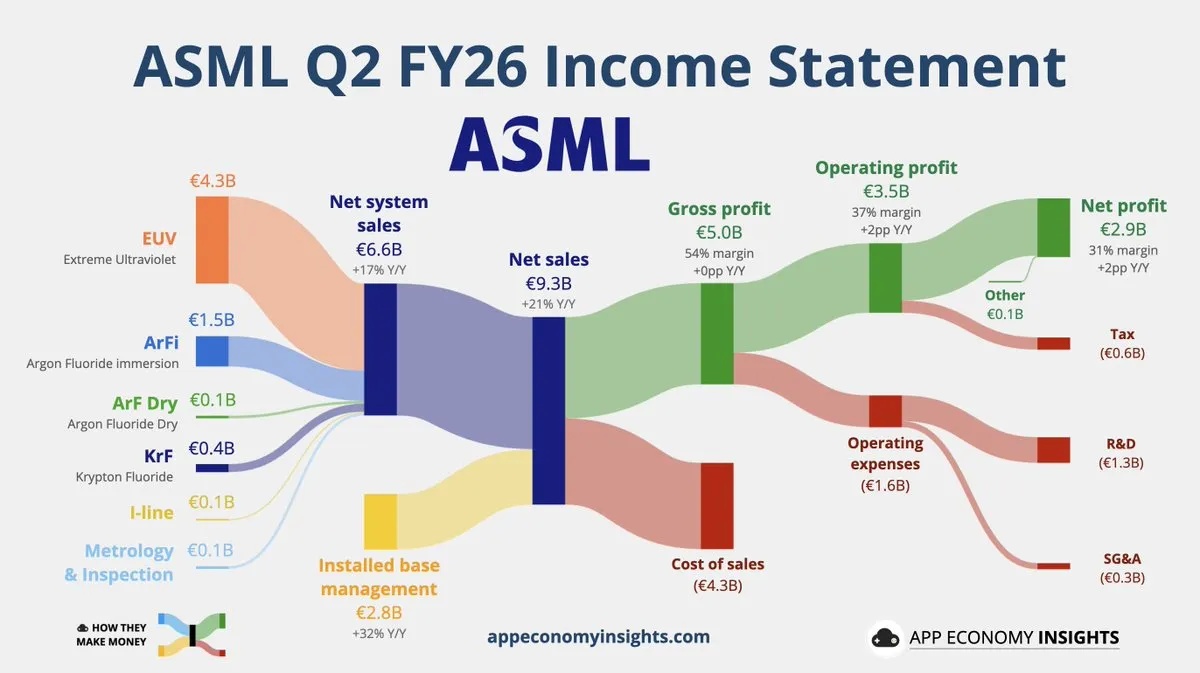

$ASML (+2,45%) has once again made headlines following the release of its Q2 2026 results, and for good reason. The Dutch semiconductor equipment giant — the world's sole manufacturer of EUV lithography machines — delivered a quarter that exceeded expectations across the board, reinforcing its status as Europe's most valuable listed company.

Record results, guidance raised for the third time

The numbers speak for themselves. ASML reported Q2 2026 revenue of €9.3 billion, comfortably ahead of the analyst consensus of approximately €8.4–9 billion, and net income came in at nearly €3 billion. Perhaps more significantly, management raised its full-year 2026 revenue guidance for the third time this year, now targeting €43–45 billion — a figure that stands well above the prior Bloomberg consensus of €39.3 billion. The company also announced plans to expand its production capacity for both EUV and DUV systems in order to address surging demand from chipmakers racing to build AI infrastructure.

The market responded positively: the stock rose approximately 7% in the sessions following the release, offering some relief after a turbulent July that had seen shares decline roughly 11% from their recent highs.

Does this make ASML a buying opportunity?

This is where the analysis becomes more nuanced — and more interesting.

Over the past twelve months, ASML's stock has risen approximately 141%, driven by the AI infrastructure boom and the company's unrivalled position in the semiconductor supply chain. The strong Q2 results largely confirm what investors already anticipated: that demand for ASML's machines is structural, not cyclical, and that the company's monopoly on EUV technology gives it extraordinary pricing power. In that sense, the results validate the euphoria that has built up around the stock — but they do not necessarily suggest that the next 12 months will mirror the last.

That said, dismissing ASML entirely would be a mistake. Several factors remain compelling. The SK Hynix order announced earlier this year — worth approximately €6.86 billion, the largest single order in ASML's history — loads the backlog further into record territory and provides multi-year revenue visibility. Memory chip demand, historically a secondary driver for ASML, has now overtaken logic foundries to represent 51% of new system sales, reflecting the scale of investment in AI-related HBM production. Furthermore, management's willingness to raise guidance three times in a single year signals genuine confidence in the demand outlook, not just short-term momentum.

The risk, however, is real. At current valuation levels, after a 141% annual gain, much of the good news is arguably already priced in. Growth-oriented stocks of this profile tend to stabilise following a period of exceptional re-rating, and any disappointment — whether from Chinese export restrictions, a slowdown in hyperscaler AI capex, or margin pressure on High-NA EUV adoption — could trigger a sharp correction. Options markets were pricing an 8.4% swing on earnings day, a level more than double ASML's historical average, suggesting that institutional investors were themselves uncertain about the near-term direction.

Bottom line

ASML remains one of the most structurally compelling stocks in Europe — arguably globally — by virtue of its monopoly position, record backlog, and the secular tailwind of AI-driven chip demand. It continues to hold the top spot in European market capitalisation at approximately $694 billion. However, for investors considering entry today, the question is not whether ASML is a great company — it clearly is — but whether the current price already reflects that greatness. There are almost certainly further gains to be made over a multi-year horizon, but the era of effortless 140% annual returns may be behind us, at least in the near term.

As always, position sizing and time horizon matter as much as stock selection.

Disclaimer: This text reflects personal analysis and does not constitute investment advice.

1111

1Semana·

China's new AI model, Kimi K3, challenges the U.S. AI industry's billion-dollar bill

China's AI company Moonshot unveiled its new flagship model "Kimi K3" —and in independent tests, it’s nearly on par with the best models from Anthropic and OpenAIin independent tests, which may have contributed to the sharp decline in AI stock prices.

What happened?

Moonshot AI, a Chinese AI company with a valuation of approximately $31.5 billion, has unveiled its new model, Kimi K3. By comparison, Anthropic and OpenAI are each projected to be valued at over $1 trillion —more than 30 times that amount.

Key figures:

Size: 2.8 trillion parameters (= the “adjustment screws” that store the model’s knowledge—roughly speaking: the more there are, the more powerful the model, but also the more expensive it is to run). This makes K3 the largest model ever to come out of China.

Open-Weight: Moonshot plans to make the model available for free download by July 27—companies could then run it on their own hardware without paying licensing fees to Moonshot. As of now, however, it’s only available through Moonshot’s paid interface.

Context: Capable of processing 1 million tokens at a time (tokens = text units; 1 million tokens correspond roughly to 750,000 words).

Unknown: The actual training costs. Anthropic also published evidence in February 2026 that Chinese labs had copied U.S. models via “distillation” (= a model learns by querying and imitating vast amounts of responses from another model). Whether and to what extent this plays a role in K3 remains unclear.

The comparison: How much do the models cost—and how smart are they?

Pricing is per 1 million tokens, broken down by input (what you send to the model) and output (what it responds with):

Kimi K3 (Moonshot): $3 input / $15 output – Intelligence Index: 57

Claude Fable 5 (Anthropic): $10 / $50 – Intelligence Index: 60 (1st place)

GPT-5.6 Sol (OpenAI): $5 / $30 – Intelligence Index: 59

Claude Opus 4.8 (Anthropic): $5 / $25 – Intelligence Index: 56

Grok 4.5 (xAI): $2 / $6 – the most affordable model among the top performers

DeepSeek V4 Pro (China): approx. $0.44 / $0.87 – low-cost segment, but index only 44

The Intelligence Index comes from Artificial Analysis, an independent testing provider that compares models across nine task areas (programming, logic, knowledge work) on a scale of up to 100.

Strengths – K3 trails the leader, Fable 5, by only 3 points, but costs only one-third as much per output token ($15 instead of $50) and half as much as GPT-5.6 Sol. In Artificial Analysis’s practical test, completing a task with K3 cost an average of $0.94—compared to $1.04 for GPT-5.6 Sol and $1.80 for Opus 4.8. When it comes to building web interfaces, K3 even took first place in blind tests with real developers.

Weakness – K3 isn’t quite as cheap as the headline suggests: It costs three to four times as much as its predecessor, is the most expensive model among its Chinese competitors, and, according to tests, “burns” up to 1.9 times as many tokens as GPT-5.6 Sol for the same task—so the cost advantage per token effectively disappears in practice. And the promised free model weights have not yet been released.

What could this mean for the market?

The AI stock boom hangs by a thread: U.S. labs like Anthropic, OpenAI, and xAI have committed to spending hundreds of billions of dollars—on chips, data centers, and electricity. Chip manufacturers, data center operators, energy providers, and construction companies have seen their stock valuations rise because this money is expected to flow to them. The plan is to refinance this through high prices for cutting-edge AI.

If a model now delivers nearly the same performance for a fraction of the price—and is soon expected to be available for free download—it could create the impression that the U.S. labs’ pricing power is crumbling (“commoditization of intelligence”: cutting-edge AI is becoming an interchangeable mass-market commodity). This wouldn’t immediately cost revenue, but it sows doubt about the business case behind the massive investments—and in overheated market phases, even a single doubt can trigger a chain reaction.

Opportunities – Cheaper AI could accelerate AI adoption overall: More adoption means greater demand for computing power for ongoing operations (inference)—and K3 is just as hardware-intensive in operation as U.S. models. Chip and infrastructure providers would benefit from this, regardless of which model is running.

The latest quarterly figures support this interpretation: On Tuesday, ASML raised its annual forecast for the second time (to €43–45 billion in revenue) and reported that its capacity is nearly fully booked through 2027. On Wednesday, TSMC increased its capital expenditure budget to a record-high $60–64 billion and stated that investments over the next three years would once again be significantly higher than those of the past three years—and that it is monitoring the construction progress of data centers to ensure its own chips do not end up in inventory. This can be interpreted as a sign that the demand side remains strong.

Risks – If price compression were to actually hit U.S. labs, training investments could be stretched out or cut back—which would eventually affect the recipients of this spending (chips, data centers, energy). Furthermore, those who train using distillation save precisely the billions in GPU costs that make the U.S. approach so expensive. The cost bases of the providers are therefore not directly comparable, but the price risk for U.S. labs still exists. A countervailing factor is that Chinese models are unlikely to be considered for security-critical U.S. applications (government agencies, robotics) due to potential backdoors.

Context

The bottom line, in my view, is that Kimi K3 is less a “DeepSeek moment 2.0” than a reality check for the valuation logic:

In 2025, the question was which chips China would use for training—now the question is whether cutting-edge intelligence permanently justifies premium prices.

The supply chain’s response (ASML, TSMC) has been clear so far: demand exists—the response at the model level is less certain.

Limitations

Initial benchmarks are partly based on manufacturer specifications = independent long-term tests are still pending.

Training costs and the potential distillation ratio for K3 cannot be verified.

Moonshot’s valuation ($31.5 billion) is from a private funding round; the trillion-dollar valuations of Anthropic and OpenAI are prospective—neither is directly comparable to market capitalizations.

Sources:

Artificial Analysis – Kimi K3 Benchmarks: https://x.com/ArtificialAnlys/status/2077832874183860404

OpenRouter – Kimi K3 Prices & Specs: https://openrouter.ai/moonshotai/kimi-k3

Anthropic – Official API Pricing Documentation: https://platform.claude.com/docs/en/about-claude/pricing

OpenRouter – Grok 4.5 Pricing: https://openrouter.ai/x-ai/grok-4.5

Price Comparison: Kimi K3 / Fable 5 / GPT-5.6 Sol: https://drawpie.com/blog/kimi-k3-vs-fable-5-vs-gpt-5-6-sol-price-benchmarks/

Decrypt – Cost per Task in Benchmark Comparison: https://decrypt.co/373716/china-kimi-k3-largest-open-source-ai-model-ever-beats-claude-fable-gpt-5-6-sol

The Decoder – K3 Classification & Price Level: https://the-decoder.com/kimis-open-model-k3-nears-gpt-5-6-sol-and-fable-5-while-signaling-the-end-of-super-cheap-chinese-ai/

ASML – Q2 2026 Earnings Call Transcript: https://www.investing.com/news/transcripts/earnings-call-transcript-asml-q2-2026-beats-guidance-as-ai-demand-lifts-outlook-93CH-4792156

TSMC – Q2 2026 Earnings Call Transcript: https://www.investing.com/news/transcripts/earnings-call-transcript-tsmc-lifts-2026-outlook-as-ai-demand-stays-hot-in-q2-2026-93CH-4794777

Anthropic – Report on Distillation Attacks (February 2026): https://anthropic.com/news/detecting-and-preventing-distillation-attacks

$NVDA (+1,47%)

$2330

$ASML (+2,45%)

$MSFT (+5,64%)

$AMZN (+2,99%)

$GOOGL (+0,79%)

1Semana·

+++ What weak signals are currently visible? 🔭 +++

Numerous companies in my DIBS investment universe have suffered significant losses in recent days. This affects not only individual stocks but also large segments of the AI infrastructure.

Following an exceptionally strong price performance, high valuations are now being scrutinized more critically. The market is taking a much closer look at margins, order intake, and the actual implementation of investment plans. At the same time, additional factors such as increasing competition or short-term disappointments are weighing on individual companies.

This is not an unusual development. Similar phases have also occurred in previous technology cycles. Sharp price increases are often followed by a phase in which the market once again distinguishes more clearly between vision and operational execution.

That is precisely why, in such market phases, I make a conscious effort to take a step back and not overinterpret every price movement.

That’s why, in such situations, I make a conscious effort to look not only at stock prices but also at the underlying signals. In doing so, I currently see both reasons for caution and indications that make me optimistic in the long term.

🔴 Selected “weak signals” that I view critically:

- Harmonic Drive Systems

$6324 (+1,92%) shows that high demand alone isn’t enough. The discussion surrounding margins and valuation has made the market significantly more sensitive. - SKF is intensifying competition in the robotics components sector through its acquisition of a Chinese precision robotics company. This could increase pressure on margins in the long term.

- Many companies continue to be valued at high multiples despite the correction. This leaves little room for operational disappointments.

🟢 Selected “Weak Signals” that make me optimistic:

- Micron $MU (+3,67%), TSMC

$TSM (+2%) and ASML

$ASML (+2,45%) have recently presented quarterly results and outlooks that continue to point to robust demand for AI infrastructure. - Micron

$MU (+3,67%) and Qualcomm

$QCOM (+0,71%) have signed a long-term supply agreement (LTA) for automotive AI. Such contracts provide planning certainty and suggest that key customers are planning their infrastructure beyond just the next few quarters. - The hyperscalers continue to invest billions in expanding their data centers. The focus is increasingly shifting from announcements to the actual implementation of these projects.

None of these signals on its own proves a trend reversal. But taken together, they help me continuously reassess my investment theses.

For my DIBS strategy, this does not currently imply an automatic decision to buy or sell. What matters to me is not whether a stock falls 30 or 40 percent in the short term, but whether the underlying bottleneck thesis has changed.

That’s why I scrutinize my investment universe particularly closely during such market phases. Not every investment thesis will ultimately pan out. At the same time, however, I currently see no convincing evidence that the fundamental technological bottlenecks in the AI infrastructure sector have already been resolved.

I will therefore continue to closely monitor developments, remaining equally open to both positive and negative signals. For now, I am not making any adjustments to my portfolio.

P.S. The photo of the observer fits the post. I took it years ago in Bonn. The figure can be found tucked away on the banks of the Rhine.

2222

11 Comentários

1Semana

I fundamentally agree with you, but the market always trades on the future, so while demand for and investment in AI may remain consistently strong at present, we are certainly (almost) at the peak.

As soon as a hyperscaler or an AI company reports weaker results, the market could take a significant downturn.

As soon as a hyperscaler or an AI company reports weaker results, the market could take a significant downturn.

•

33

•

2Semana·

ASML rises 4% after hiking sales forecast for second time this year on strong Al chip demand

ASML rises 4% after hiking sales forecast for second time this year on strong AI chip demand. Orders extremely strong. #ASML

#Semiconductors

$ASML (+2,45%)

44

2Semana·

𝐀𝐒𝐌𝐋: 𝐐𝟐 𝐁𝐞𝐚𝐭, 𝐑𝐚𝐢𝐬𝐞𝐬 𝐅𝐘𝟐𝟔 𝐎𝐮𝐭𝐥𝐨𝐨𝐤 𝐀𝐬 𝐀𝐈 𝐃𝐞𝐦𝐚𝐧𝐝 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐞𝐬

📊 𝐑𝐞𝐬𝐮𝐥𝐭𝐬

• Revenue: €9.33B (+6.3% QoQ)

• Gross Margin: 54.0% (+100 bps QoQ)

• Net Income: €2.92B (+5.8% QoQ)

• EPS: €7.59 (+6.2% QoQ)

• New Lithography Systems Sold: 86 (vs. 67 QoQ)

⠀

🎯 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

• Q3 Revenue: €11.0B–€12.0B

• Q3 Gross Margin: 55%–57%

• FY26 Revenue: €43B–€45B (raised)

• FY26 Gross Margin: 54%–56% (raised)

⠀

📌 𝐊𝐞𝐲 𝐓𝐚𝐤𝐞𝐚𝐰𝐚𝐲𝐬

• Q2 revenue and gross margin both exceeded guidance

• Strong AI-driven demand continues to accelerate customer capacity expansion

• ASML plans to increase Low NA EUV and DUV immersion capacity by 30% in 2027, with further expansion under evaluation for 2028

• Repurchased approximately €1.1B of shares during Q2 and announced an interim dividend of €1.88 per share

⠀

💬 𝐌𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭 𝐂𝐨𝐦𝐦𝐞𝐧𝐭𝐚𝐫𝐲

“Ongoing AI investments continue to strengthen semiconductor demand. Customer commitments across our portfolio provide increased visibility into long-term growth, supporting our decision to raise our 2026 outlook and expand production capacity.”

2929

2Semana·

New release

$ASML (+2,45%)

extrem starkes 2nd quarter

“Our order intake remained extremely strong in the first half of the year.”

einzig der Cash Flow hängt

88

2Semana·

RBC Capital has raised its price target for ASML stock based on the positive EUV demand forecast.

Ahead of the earnings report on July 15.

On Monday, RBC Capital raised its price target for ASML Inc. (NASDAQ:ASML) from $1,700 to $2,000 and maintained its “Buy” rating.

The stock is currently trading at $1,726, up 115% over the past year. However, analyses suggest that the stock is overvalued relative to its estimated fair value.

The company stated that demand for EUV lasers has improved since the last quarterly report, but that near-term growth potential is expected to be limited given the long lead times.

RBC Capital expects a more significant improvement in EUV shipments by 2027, to nearly 90 units (excluding Alaska and Hawaii), up from over 80 previously.

The analyst cited robust investment in AI technologies, tight DRAM availability, and increasing competition among leading contract manufacturers as drivers of strong EUV demand.

EUV is becoming a bottleneck, and the company said it is unlikely that the supply situation will ease over the next two to three years.

RBC Capital highlighted the record profitability of ASML’s customers and stated that the market environment is ideal for price adjustments that could accelerate revenue and margin growth.

The firm is convinced that positive market trends in terms of unit volumes and product mix are sufficient to further boost the company’s above-average performance.

The analyst noted that a potential acquisition of Terafab could further improve the company’s future prospects. According to Tips, ASML remains a major player in the semiconductor and semiconductor equipment industries.

In other recent news, there has been significant activity related to ASML’s financial outlook and operational strategies.

Bernstein raised its price target for ASML to $2,623, citing increased demand driven by expansion in the field of artificial intelligence.

This has also led to higher revenue forecasts and expectations regarding the growth of EUV shipments in the coming years. Meanwhile, BofA Securities reaffirmed its “Buy” rating with a price target of $2,268and highlighted ASML’s forecast for 2030, which projects potential revenue of between 44 and 60 billion euros with gross margins of 56 to 60 percent.

2323

Títulos em alta

Principais criadores desta semana

Dados tempo real da LSX · Dados financeiros e EOD da FactSet