Keyence ($6861 (-1,48%)) is not a classic hardware trade, but a structural bet on the total automation of global industry and its unstoppable need for efficiency.

Industrial automation is only the tool here. The real value comes from a unique fabless model, radical direct sales and unrivaled pricing power. pricing power.

Margin instead of mass, problem solving instead of product sales, cash flow instead of capital commitment.

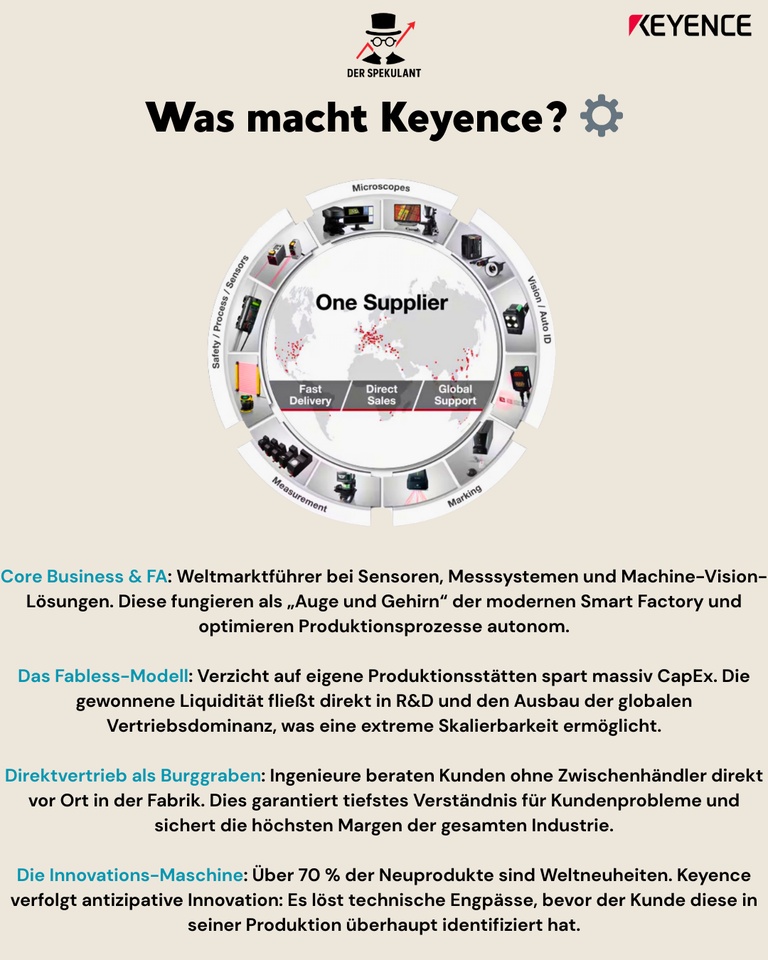

⚙️ What does Keyence do?

➡️ Core Business & FA (factory automation):

World market leader in sensors, measuring systems and machine vision solutions. Keyence provides the "eye and brain" of the modern smart factory. The products are essential for autonomous production.

→ Technology leadership + Indispensability.

➡️ The fabless model:

Keyence does not produce itself. By outsourcing production, the company makes massive CapEx savings and remains extremely agile. The capital flows primarily into R&D and sales.

→ Maximum scalability + asset-light structure.

➡️ Direct sales as a moat:

No middlemen. middlemen. Highly specialized engineers advise customers directly on site at the factory. This creates deep trust and secures the highest margins in the entire industry.

→ Deep customer understanding + enormous pricing power.

➡️ The innovation machine:

Over 70% of new releases are world firsts. Keyence anticipates industry problems before customers have even identified them themselves.

→ continuous competitive edge + high barriers to market entry.

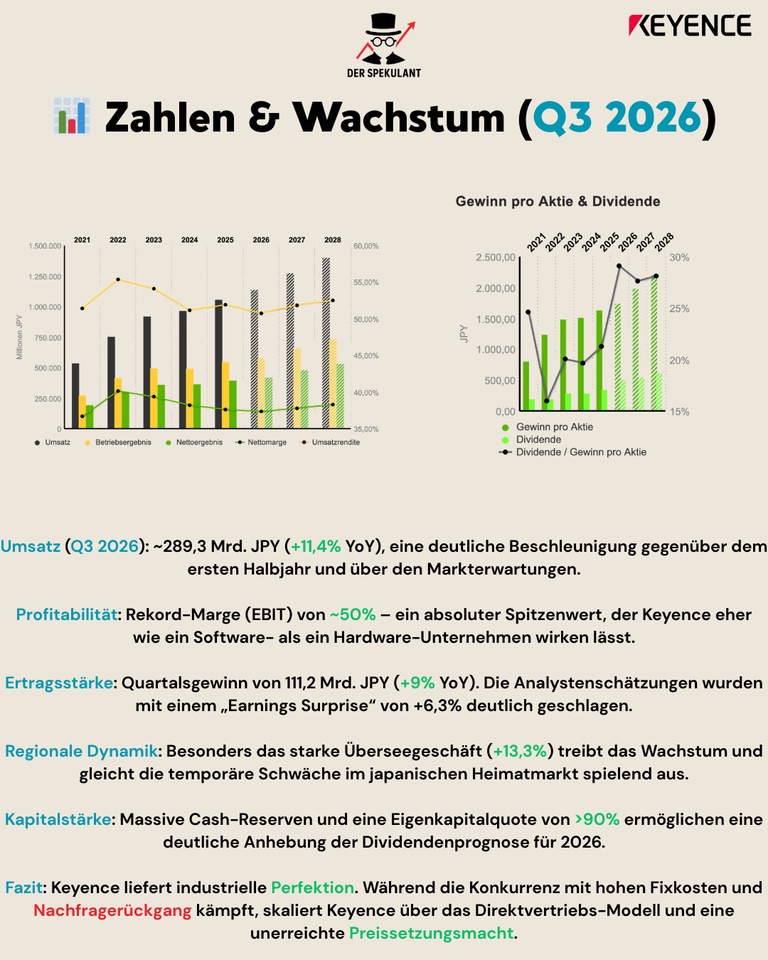

📊 Figures & growth (Q3 2026 - reported 29.01.26)

📈 Quarterly sales Q3:

~289.3 billion JPY (+11,4% YoY) → significant acceleration and outperformance compared to market expectations.

📊 9-month sales:

At JPY 834.6 billion (+7,7% YoY), the company is heading unerringly towards a new record year.

📈 Profitability:

Record operating margin (EBIT) of ~50% → An absolute peak value that makes Keyence look more like a software company than a hardware company.

👥 Regional dynamics:

The strong overseas business in particular (+13,3%) is driving growth and easily offsetting the temporary weakness in the Japanese domestic market.

💰 Capital strength:

Massive cash reserves and an equity ratio of >90% enable a significant increase in the dividend forecast for 2026.

Conclusion: Keyence delivers industrial perfection in numbers. While competitors struggle with fixed costs, Keyence scales through efficiency and desirability.

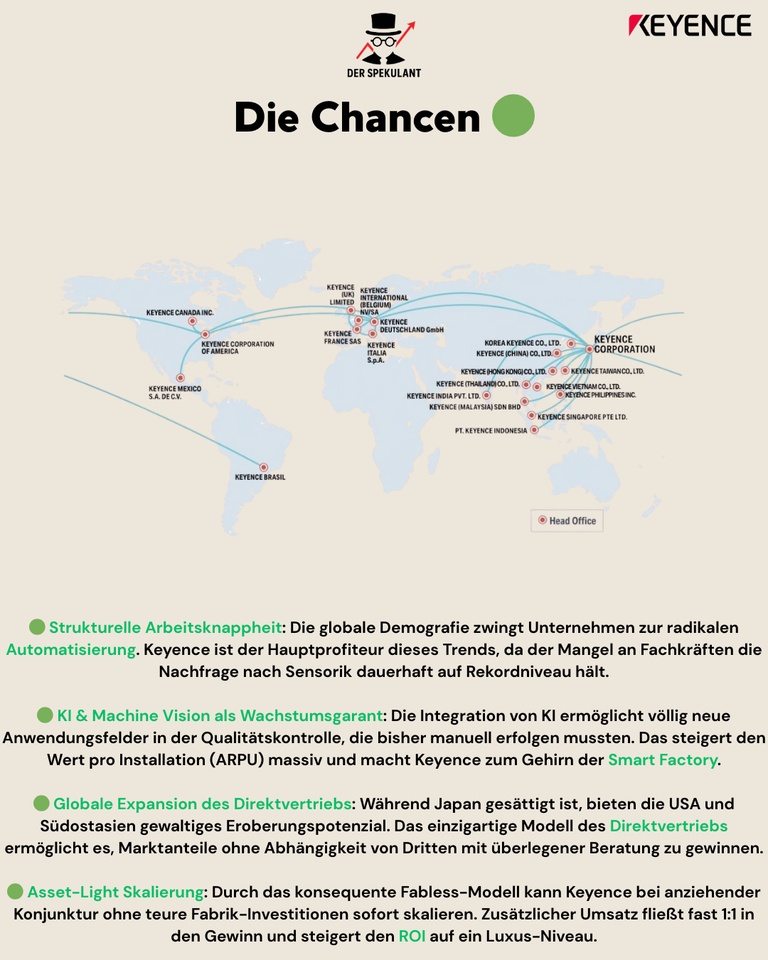

🟢 The opportunities

🟢 Structural labor shortage:

Global demographics are forcing companies to automate. Keyence is the natural beneficiary of the skills shortage in Japan, China and Europe.

🟢 AI & machine vision as a guarantee for growth:

New vision systems with AI support increase the value per installation (ARPU) and open up new markets in automated quality control.

🟢 Asset-light scaling:

During an economic upturn additional turnover flows almost 1:1 into the profit, as no expensive investments in own factories are necessary.

🟢 Global expansion:

The unique direct sales model still offers enormous potential for conquering traditional retail in the USA and South East Asia.

🔴 The risks

⚠️ Cyclical dependency:

Keyence depends on the investment cycles of the automotive and semiconductor industries. A global recession puts a direct brake on demand.

⚠️ Currency headwinds (yen):

As the majority of growth is generated outside Japan, a strong yen leads to negative translation effects. translation effects on earnings.

⚠️ China cluster risk:

A significant proportion of demand comes from China. Geopolitical

tensions or local phases of weakness have a direct impact on international momentum.

⚠️ Sporting assessment:

Quality has its price. The high

P/E RATIO leaves room for corrections in the event of the slightest operational disappointment or slower growth.

💡 Conclusion & outlook

Keyence is not a short-term hardware trade, but a structural bet on global automation of the next decade.

🔹 Short term:

Sensitive to the general valuation level (P/E ratio), global currency effects and market sentiment towards quality stocks.

🔹 Long-term:

ROI machine with a deep technological moatextreme pricing power and an operating marginthat is unparalleled worldwide.

🎯 Investment case:

Leverage on skills shortage + smart factory + AI sensor technology + maximum margin efficiency→ Structurally value-enhancing, operationally highly profitable, the gold standard for the portfolio in the long term.

💬 Community question:

👉 Japan's most profitable tech champion as a defensive anchor in the portfolio

or

👉 currently too expensive for a new entry at this P/E ratio?

I am curious about your assessment 👇