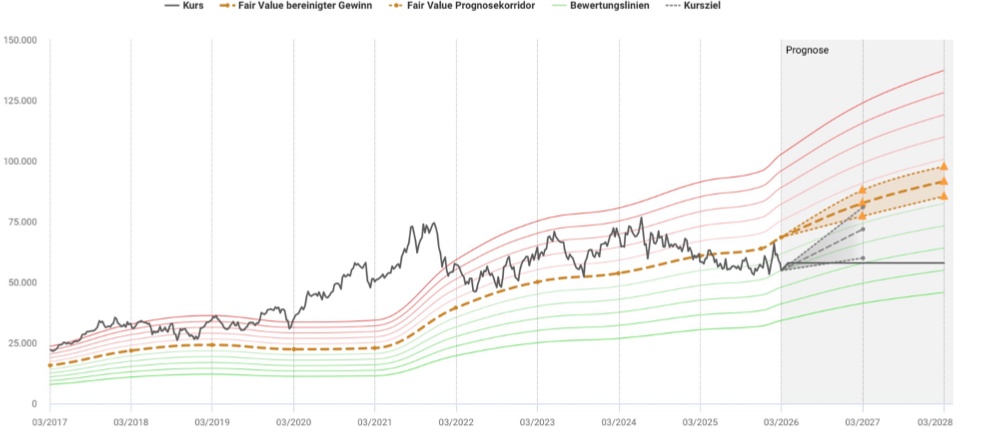

To answer this question, it is first worth taking a look at the chart.

The share has lost around 45% since its high of around €590 and is currently trading at €317. If the question arises as to why the share has been sold off so strongly, this is due to a real exaggeration on the upside, which in my view has caused an exaggeration on the downside. You can see how, according to the share finder, it was well above fair value for a long time. Recently, however, it has come back significantly.

1. the "fabless" miracle: assets without ballast

Keyence develops sensors, microscopes and vision systems for factory automation. Yet they do not own a single factory.

- The effect: they have almost no tied-up capital (asset-light). If the economy falters, they do not have to close any factories or lay off workers.

2 The direct sales monopoly

Normally, companies sell through intermediaries. Keyence does the opposite:

- On-site problem solvers: Keyence engineers go directly to customers' factories. They don't just sell a product from the catalog, but solve a specific problem (e.g.: "How do I detect this micro-crack at 200 km/h belt speed?").

- Pricing power: Since they offer a solution that saves the customer millions in downtime costs, the price of the sensor hardly plays a role. This leads to a gross margin of over 80%.

This is the biggest moat there is. They have a virtual monopoly in this area of automation and problem solving.

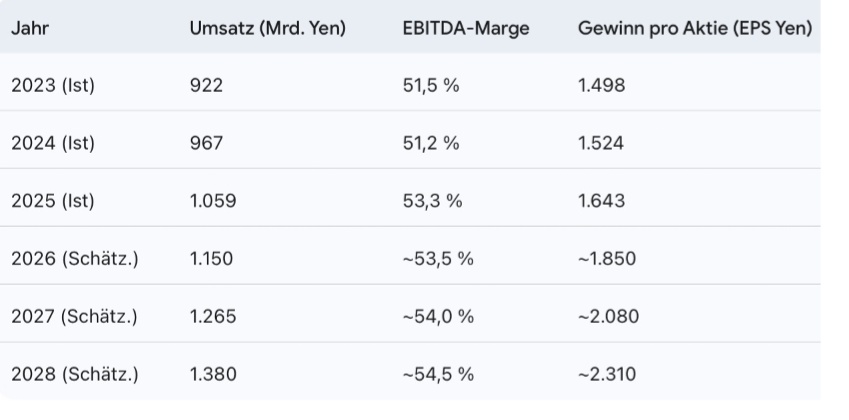

The EBIT margin is a legendary 53% and the net income margin is around 37%. This means that almost half of every euro of turnover remains as pure profit. And that for an industrial company.

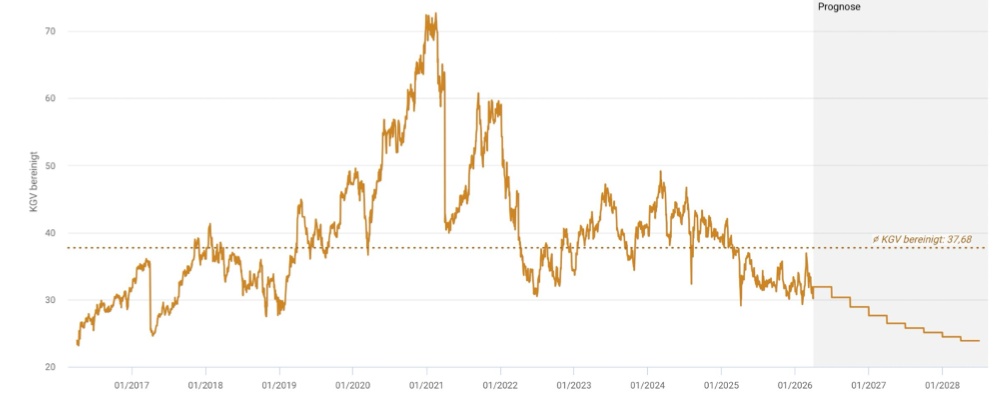

The current P/E ratio is around 30, which is 7.68 points below the historical average of 37.68 for the last 10 years. The 5-year average is even 45. From this perspective, the Keyence share appears to be reasonably valued.

favorably valued from this perspective.

Keyence is also sitting on a high cash mountain and is practically debt-free.

What about the risks?

China exposure & geopolitics

Keyence is heavily dependent on the global propensity to invest.

- Problem: A significant proportion of sensors end up in Chinese factories (e-car production, batteries, electronics). If the trade conflict between the USA and China escalates in 2026 or China makes access for foreign high-tech even more difficult, Keyence will be directly affected.

- Currency risk: The weak yen has visually inflated profits. If the yen appreciates massively in 2026 (e.g. due to interest rate hikes by the Bank of Japan), foreign income will be lower when converted into yen.

Opportunities:

The labor shortage.

This is the biggest opportunity for Keyence. In almost all industrialized nations (Japan, Germany, USA) and even in China, the working population is shrinking.

- From "nice-to-have" to "must-have": in 2026, companies will no longer automate just to save costs, but because they can no longer find people.

- Keyence advantage: As Keyence sensors are extremely easy to install, companies can automate their factories faster than with the complex individual solutions of the competition.

Scalability: Since Keyence has no factories, they can roll out software updates for their AI sensors worldwide and charge subscription fees or higher margins. This makes the business model even more "software-like".

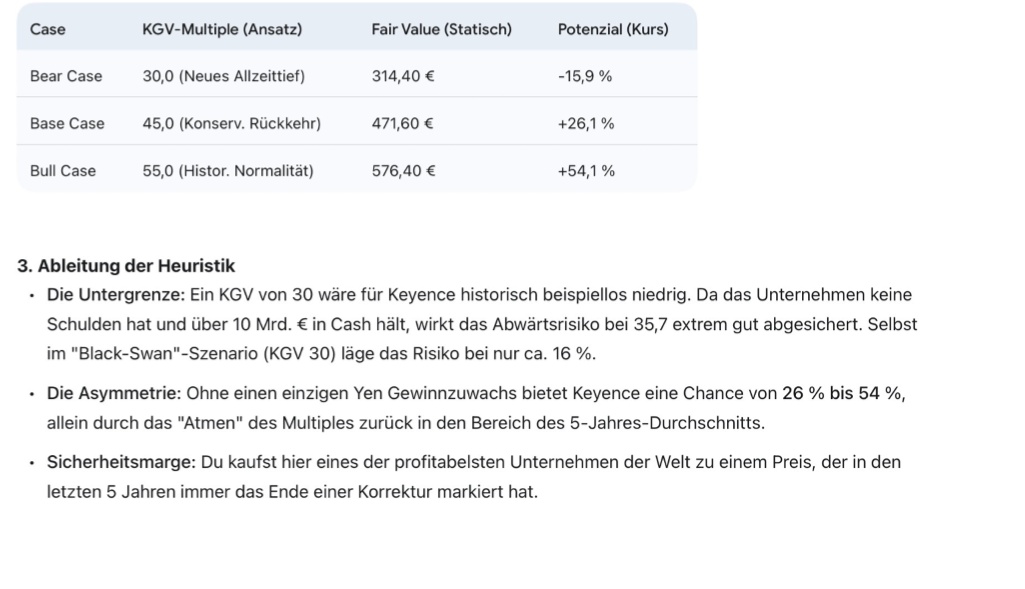

Finally, if we look at the heuristics, the following picture emerges.

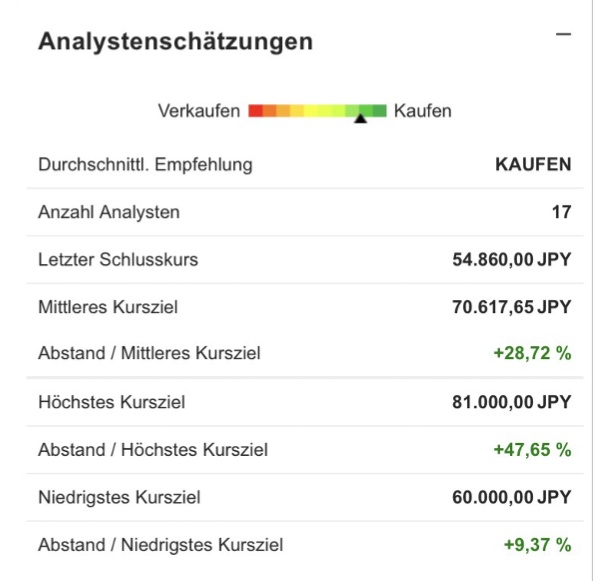

The majority of analysts also recommend buying with a premium of almost 30% to the average price target.

Conclusion: I personally see Keyence as a good stock for diversification. The margins are also outstanding and you are still buying a quality company at a high price, albeit well below its historical average. Looking at the heuristics, my model also shows a good risk/return ratio. I don't think you can do much wrong with the share, as the company has a huge cash reserve and also holds a monopoly-like position in Japan.

What do you think of the company? Are you already invested?

Feel free to write your opinion, also with regard to the current market risks.

@Tenbagger2024

@Get_Rich_or_Die_Tryin

@Raketentoni

@PikaPika0105 etc......