Here is an update on Kraken Robotics and my research into the takeover of the Covelya Group.

With the acquisition of the British Covelya Group for a total value of USD 615 million (financed by USD 480 million in cash and USD 135 million in shares), Kraken Robotics has made the leap from a specialized sensor manufacturer to a vertically integrated company in underwater technology. This takeover is accompanied by a dilution of around 21% of existing shareholders. I will briefly explain how this dilution is to be classified later and what exactly was taken over. I am primarily concerned with how the financial key figures, sales and profit targets and customer landscape have changed. But let's get started:

Who is Covelya? Brief overview

To understand the scale of this acquisition, you need to look at the Covelya Group portfolio. Covelya Group is a group of market-leading maritime technology companies with over 750 employees and twelve locations worldwide.

The subsidiaries include:

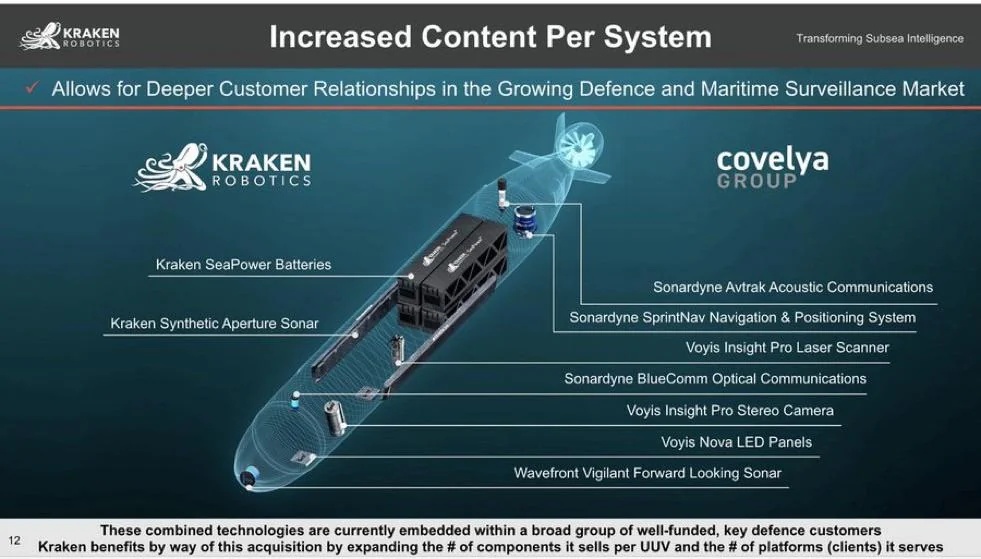

- Sonardyne: The heart of the group. Sonardyne is the global market leader in underwater acoustic navigation, positioning and communication. Its technology is the "gold standard" for the offshore energy industry and modern western navies.

- Voyis: Specialists in high-resolution optical sensors and laser scanners that create millimeter-precise 3D models of the seabed and underwater structures (e.g. pipelines).

- Wavefront Systems: Experts in sonar systems for obstacle avoidance and diver detection.

- EIVA: Provider of software and hardware solutions for efficient mapping and surveying of the oceans.

As Covelya is significantly larger than Kraken Robotics, the acquisition also brings numerous well-known customers on board. Covelya's largest customers include Shell, BP, TotalEnergies, ExxonMobile, the US Navy, the Australian Navy, the UK Royal Navy and companies such as Oceaneering. With this acquisition, Kraken Robotics now controls the entire value chain - from sonar/laser systems to maritime navigation and power supply through SeaPower batteries.

Significance - massive expansion of the moat

The market shares following the merger create an almost monopoly-like position in critical segments:

- Underwater Navigation: Kraken/Sonardyne now control an estimated 40% to 60% of the global high-end positioning market.

- Synthetic Aperture Sonar (SAS): (underwater sonar systems)Kraken is the dominant player here with OVER 70% market share.

- Precision inspection: The company now holds around 30 % to 50 % of global capacity in laser scanning.

To reiterate, Kraken Robotics now controls between 30% of the global market for laser scanners and over 70% (!) for sonar systems in all key areas of underwater technology!

After the takeover, there is no comparable company in the underwater technology sector with such a position. By integrating Covelya, Kraken Robotics has created a monopoly in the field of state-of-the-art technology for the oceans.

Although there are many companies that also market a certain part of this technology, there is no competitor that has such control over the entire value chain in this area. This is also reflected in the figures:

The figures: Turnover and profit development until 2028 (estimate)

While Kraken still reported revenue of around USD 70 million in 2024, the merger takes the company to a new level:

- 2025 (preliminary): Approx. USD 115 million (purely organic growth).

- 2026 (+acquisition): Expected turnover of USD 495 million after integration of Covelya. (Almost 300 million of the sales come from Covelya)

- 2027 (estimated): Increase to USD 620 million, driven by stronger integration of Covelya and major orders in the defense sector.

- 2028 (target): The company is targeting the USD 800 million sales mark.

-> from USD 70 million in 2024 to USD 800 million in sales by 2028 is more than a tenfold increase in sales in four financial years!

The EBITDA margin (including the acquisition) is set to rise from 22.7% in 2024 to 25% in 2026 and to over 31% by 2028 thanks to synergy effects of USD 15 million per year.

Despite the dilution caused by the capital increase, earnings per share (EPS) are forecast to double to around USD 0.12 by the end of 2027.

Takeover price

For a purchase price of USD 615 million, Kraken Robotics is securing a company that already generates stable annual sales of around USD 275 million and contributes a strong EBITDA margin of around 28% to its balance sheet. Just for comparison, Kraken Robotics itself did not even generate USD 200 million in sales last year and is not that profitable with a margin of 22.7%.

In terms of valuation, Kraken has benefited extremely here: At an EV/sales multiple of around 2.2x and an estimated takeover P/E of 14 to 16 (based on Covelya's net profit), the price is well below the multiples that Kraken itself has on the market. You have to imagine that.

Covelya is being acquired at a P/E of 14-16 - the stock market would certainly be willing to pay a P/E of 60-70 for the company's organic growth of over 20% and Kraken Robotics' management has recognized this. This valuation arbitrage effect means that Kraken buys "cheap" earnings, which are immediately revalued on the stock market at Kraken's higher growth premium. This not only buys the technology and market share, but also ensures an immediate increase in value.

Dilution of shareholders

In order to finance the acquisition of the Covelya Group, Kraken Robotics carried out a capital increase in March 2026, which resulted in the issue of around 47.4 million new shares. Together with the share component for the sellers, this increases the total number of outstanding shares by approximately 21%, which means a corresponding percentage dilution for existing shareholders. Management itself says that the acquisition is immediately accretive and that this move is considered "accretive" as the massive increase in revenue and EBITDA is expected to fully outweigh the dilutive effect as early as 2027. While the dilution is around 20%, Kraken's revenue will increase by several 100% as a result of the takeover! Although I am of course not super happy that my share in Kraken Robotics has decreased, I see far more opportunities than risks as a result of the massive expansion

Valuation

In terms of valuation, Kraken is currently trading at a P/E ratio (2026e) of approx. 125x (if Covelya's profit is not included). What initially seems high is put into perspective by the enormous profit growth and an EV/EBITDA ratio of around 20x, which in my opinion is justified for a market leader in the high-tech defense sector with well over 30% growth per year. And because profits are rising disproportionately due to the margin increase, the P/E ratio will fall significantly towards 60 in 2027...

Current drivers: situation in Iran

The current security situation, in particular the conflict in Iran and the associated threat to the Strait of Hormuz, has once again made maritime security a priority for NATO countries. The protection of critical infrastructure (pipelines, data cables) is no longer feasible without the autonomous technology of Kraken.

Iran has partially blocked the Strait of Hormuz with sea mines - the use of underwater robots is crucial for the removal of sea mines. This means that the navy soldiers are not exposed to immediate danger, but can defuse the sea mines from a distance...

Conclusion

The acquisition of Covelya makes Kraken Robotics an indispensable company in the western maritime world. With a stable balance sheet (USD 402.5 million gross proceeds from the last capital increase) and a dominant market position, the company is excellently positioned to benefit from the massive increase in investment in maritime sovereignty. Of course, a takeover is always accompanied by risk, as the integration could fail. In my opinion, however, the opportunities here clearly outweigh the risks and I am even more convinced of Kraken Robotics than before. The company is growing strongly and is positioned as a technological leader. I see prices of well over EUR 10 as likely in the near future and will continue to hold the share.

You can find my detailed analysis of Kraken Robotics and other shares in my profile and here:

Please let me know what you think about the takeover and whether I have forgotten anything important...

LG small investor 😊