Hello my dears,

More and more people are focusing on the topic of organ donation. And the importance and acceptance is growing.

This already started last year with the idea of $TMDX (+0,92%) the love @BamBamInvest recognized.

The company I am presenting to you today is more about the technology and the process.

I'm looking forward to your comments on how much potential you see in the company.

Juan already sees potential through the double-digit sales growth and the triple-digit profit growth.

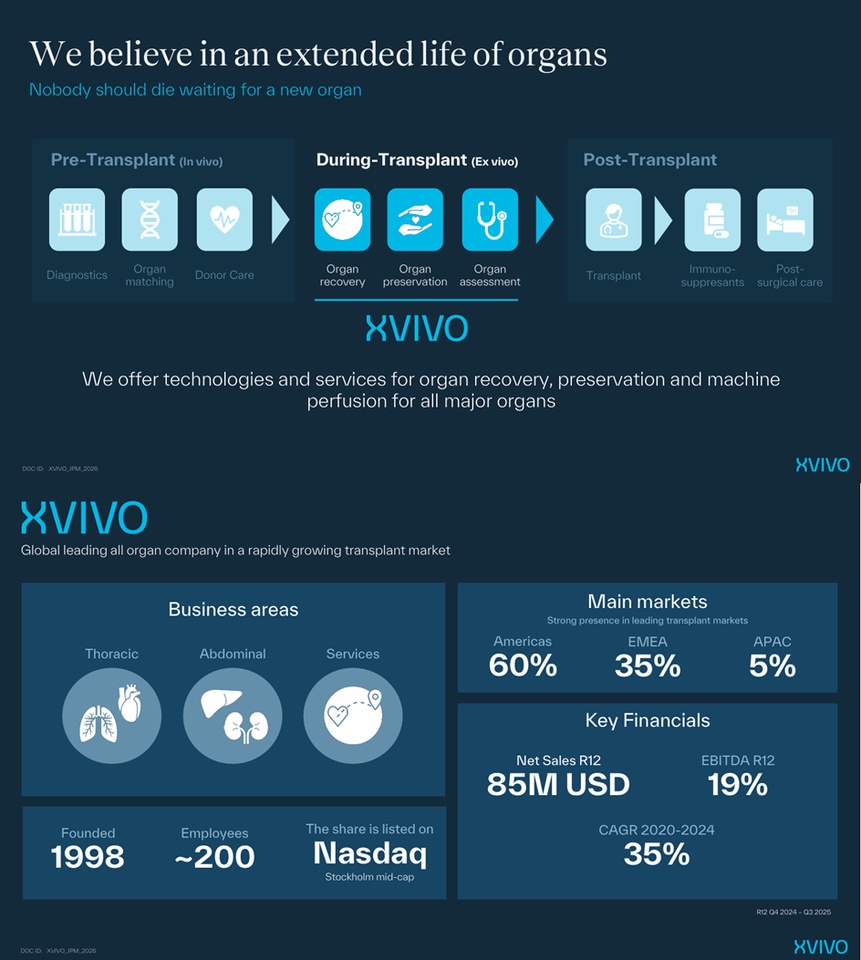

Xvivo Perfusion AB is a Sweden-based medical technology company focused on developing optimized solutions for organ, tissue and cell preservation in connection with transplantation. The company operates in two segments: Durable Goods and Non-Durable Goods. The Durable Goods segment includes sales and rental income from XVIVO Perfusion System (XPS) devices. The Consumer Durables segment includes revenue from the sale of products and services that are solutions and disposables. The Company's product portfolio consists of Perfadex, STEEN Solution, XPS, XPS Disposable Kit, XVIVO Lung Cannula Set, XVIVO Organ Chamber, XPS PGM Disposable Sensors and Silicone Tubing Set. The company distributes its products in Europe, Asia, the Middle East and North and South America.

Number of employees: 199

Founded: 1998

Headquarters: Gothenburg Sweden

Global market leadership

XVIVO is the global leader in lung preservation and perfusion and strives to be a global leader in heart, liver and kidney.

- The business unit Thoracic Surgery includes XVIVO's lung and heart transplantation products.

XVIVO is the global leader in lung transplantation with PERFADEX Plus for cold protection and XPS with STEEN Solution for mechanical perfusion.

For heart transplantation, the heart technology consists of a machine, a disposable unit and a perfusion solution with a nutritional supplement specially adapted for the heart.

(63 % of total sales in 2025)

- The area of Abdominal segment comprises XVIVO's liver and kidney technologies.

For liver transplants, XVIVO sells Liver Assist, the leading perfusion technology in Europe.

For kidney transplants, Kidney Assist and Kidney Assist Transport are used for mechanical perfusion.

In Italy, XVIVO also offers a perfusion service in which employed perfusionists support clinics in the use of the company's technologies.

(28% of total sales in 2025)

- Services

In the US, Xvivo Services optimizes the transplant process to help clinics perform more transplants. The business includes organ recovery and a digital communication platform, FlowHawk.

XVIVO's recovery team is available around the clock to recover thoracic organs and transport them to transplant centers. In October, XVIVO acquired FlowHawk - a HIPAA-compliant tool that enables real-time communication between transplant teams. It is now available on the US market.

(9% of total sales in 2025)

Strategy 2027

- Accelerate market leadership in the lung segment

- Change the paradigm of heart preservation

- Become the market leader in kidney perfusion

- Accelerate market leadership in liver perfusion

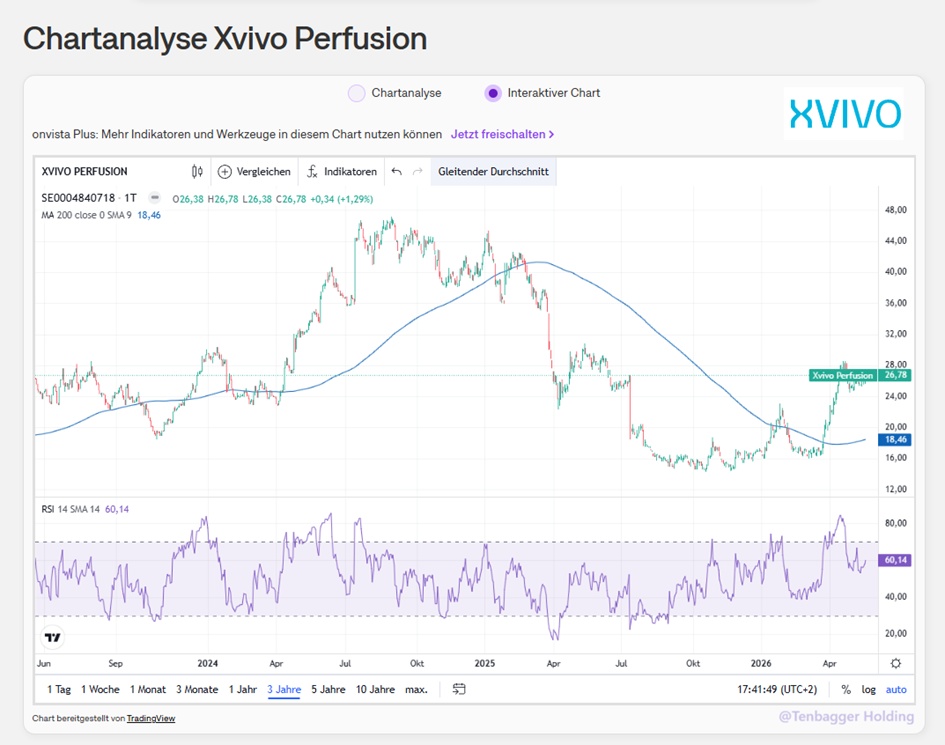

18/05/2026, 13:45

22,04,2026

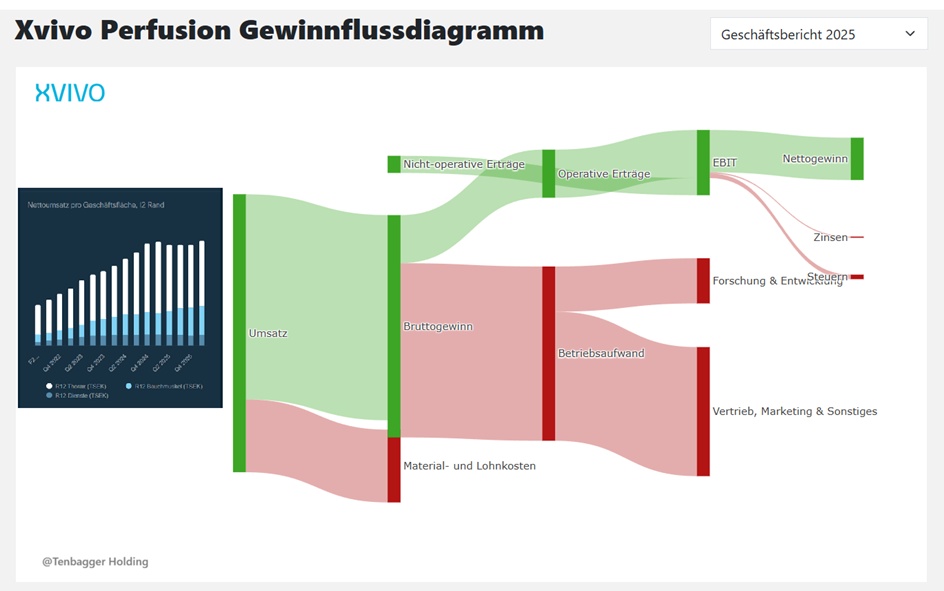

Distribution of sales by business division

2025 (SEK)

Thoracic 509 m

Abdominal 225 m

Services 77.53 m

Geographical distribution of sales

2025 (SEK)

U.S.A. 428 M

EMEA Excluding Sweden 306 M

Asia/Pacific and Oceania 49.2 million

North and South America 22.26 million

Sweden 6.69 million

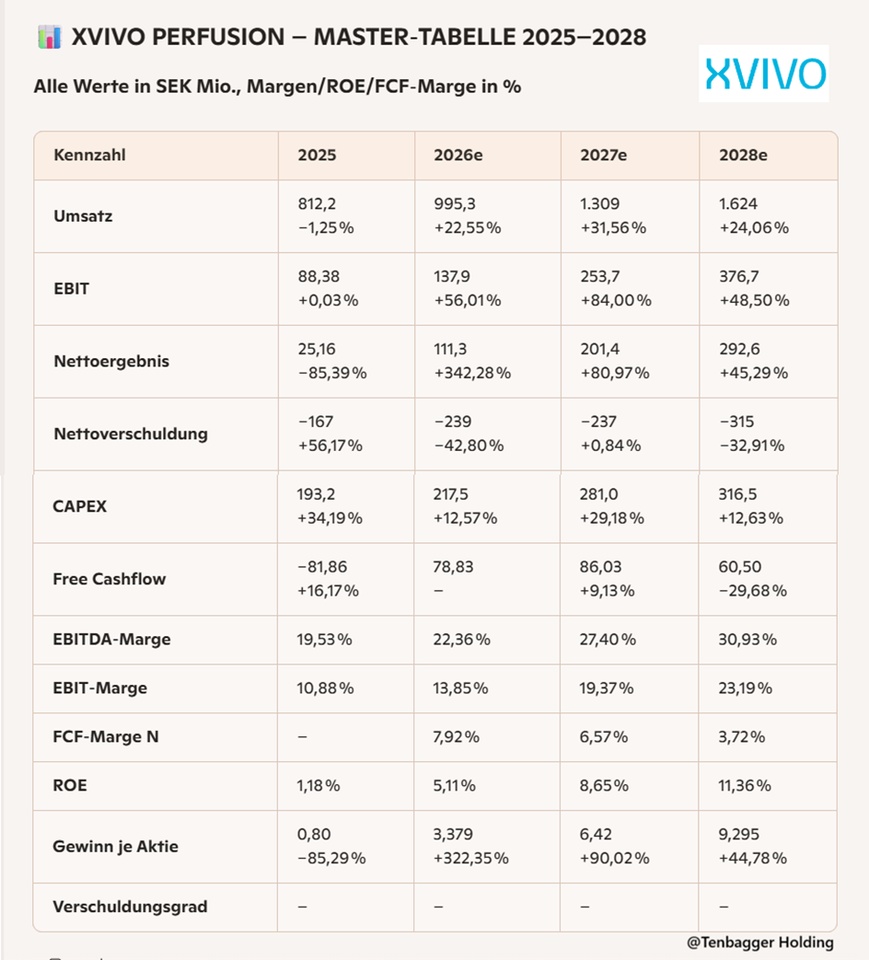

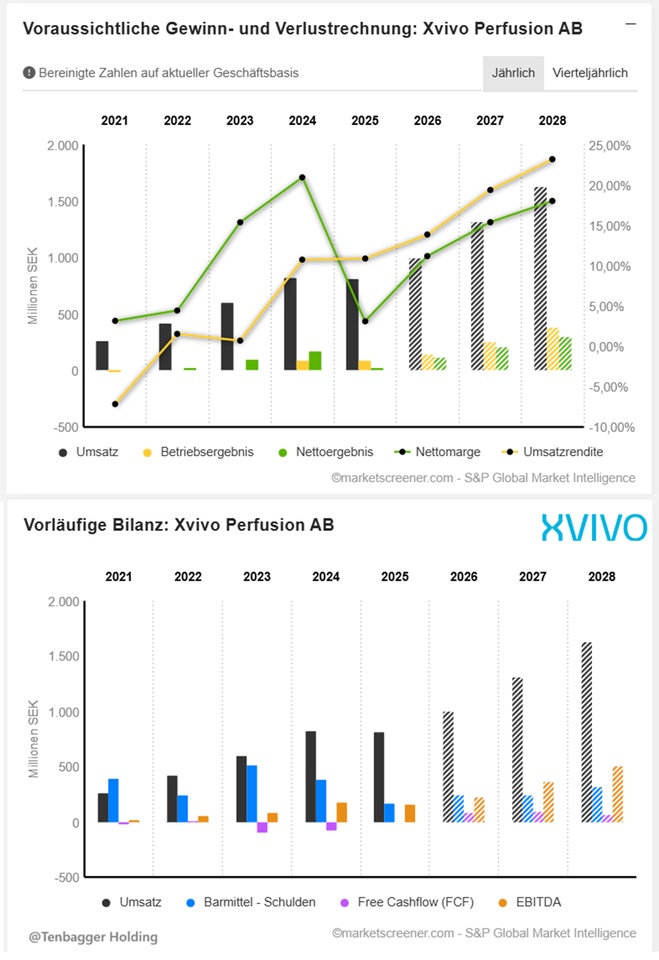

🧠 Juan's conclusion on the key financial figures

"These are exactly the kind of figures that make me pull my hoodie tighter and say:

Okay... something real is happening here."

- The triple-digit profit growth (2025 → 2026 → 2027) is not a coincidencebut a clear scaling effect: sales high, margins high, cost base stable.

- EBIT jumps massivelywhich shows that the business model is finally entering the phase in which every additional sales crown has a real impact.

- Net profit explodesbecause XVIVO is growing out of the "investment phase" and moving into the "harvest phase".

- ROE picks up cleanly - not yet high-ROE, but the trend is textbook.

- Net cash position provides security: growth without balance sheet stress.

- FCF will be positive from 2026which is a strong signal for medtech scale-ups.

In a nutshell:

XVIVO delivers exactly the pattern you want to see in a future quality compounder:

First sales, then margins, then profits, then cash flow.

If the execution holds, this is one of the cleanest turn-to-scale stories in medtech.

Market value 9,047

Number of shares (in thousands) 31,499

Date of publication 27,01,2026

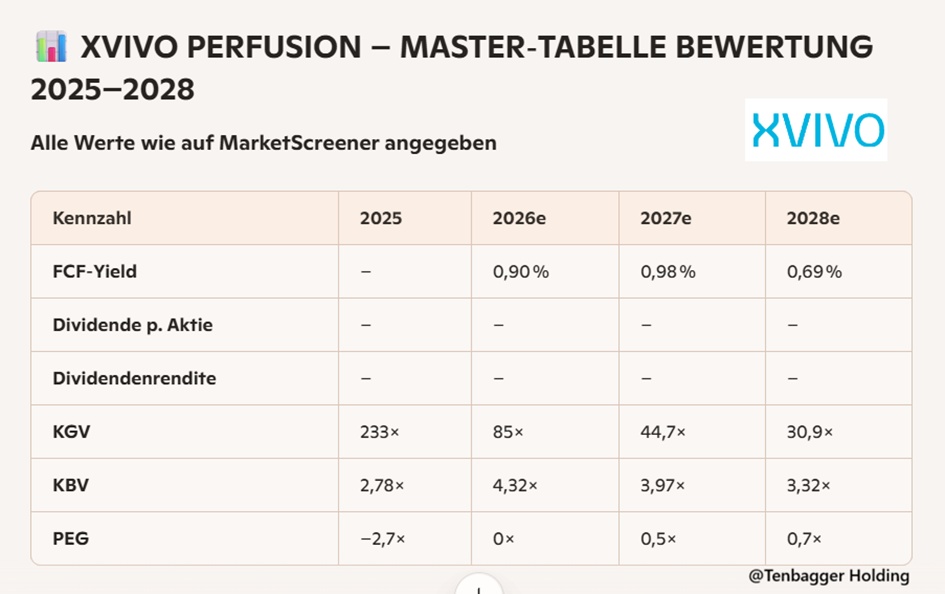

🧠 Juan's conclusion on the valuation ratios

"The valuation looks expensive at first glance - but it tells a story."

- P/E ratio falls from 233× → 85× → 44× → 31×. This is not a "cheap share", but a classic growth multiple compression case: Earnings grow faster than the share price - that's exactly what you want to see.

- PEG in the sweet spot from 2027 (0.5-0.7). This is the level at which quality growth suddenly looks attractive again.

- P/B ratio rises briefly in 2026, then normalizes. Typical for companies that grow into profitability.

- FCF yield positive from 2026, but still low. That's okay - XVIVO is a scale-upnot a cash cow business.

- No dividend - and that's a good thing. Every SEK goes into growth, not to shareholders.

In short:

The valuation is high, but it is falling fast - and for the right reasons.

If the profit story holds, XVIVO will become "cheaper" every year without the share price having to fall.

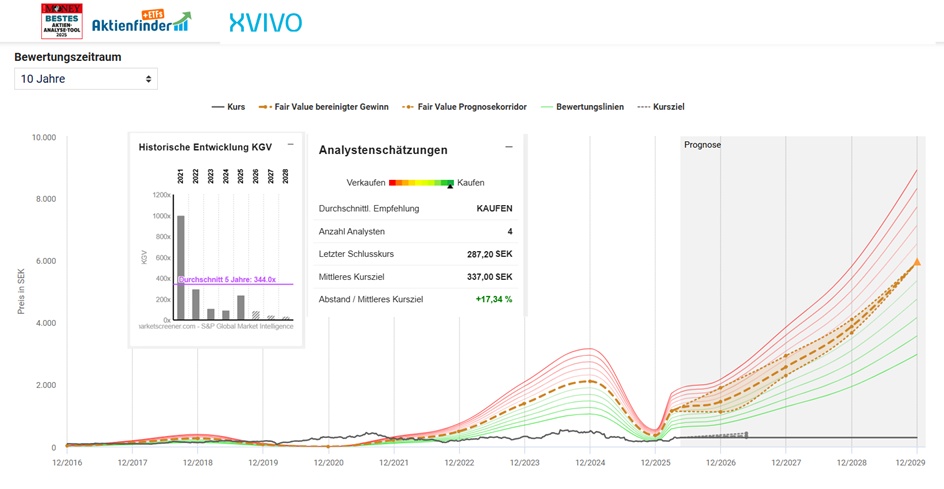

The key figure with the highest stability for the Xvivo Perfusion share is the adjusted profitwhich is used below for the valuation. The P/E ratio calculated from this key figure P/E ratio (price/earnings ratio) is 96.19 which is 286.98 points below the historical average of 383.17 for the last 10 years. From this perspective, the Xvivo Perfusion share appears to be favorably valued to be favorably valued

The fair value of the Xvivo Perfusion share is calculated over the 10-year valuation period selected above. The average P/E ratio in this case is 383.17.

Multiplied by the adjusted earnings per share of SEK 2.99 over the last 4 quarters, the Xvivo Perfusion share has a fair value of fair value of SEK 1,145.67. The current share price of SEK 290.83 is 74.6% below this fair value, which represents a strong undervaluation of the share.

22,05,2026

today, 11:43:16 -

gettex (EUR)

27,14 EUR

+0.36 EUR+1.34 %