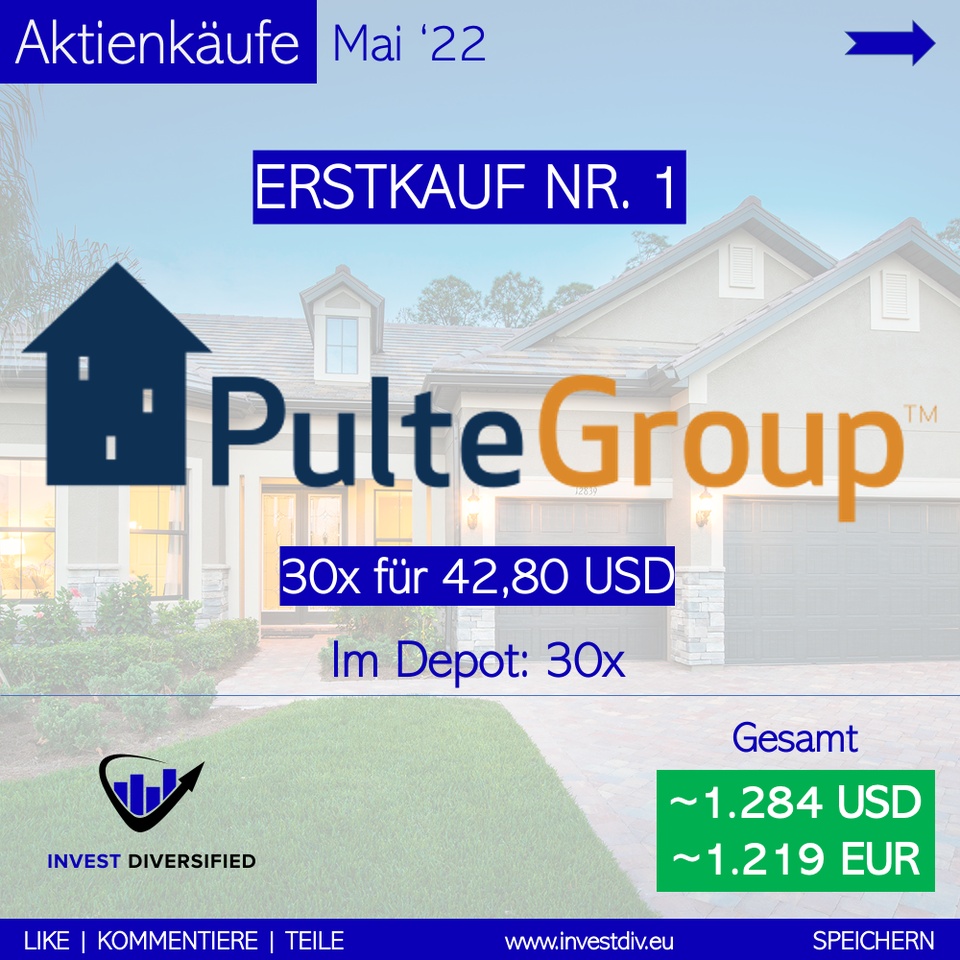

Last week, $PHM made it into my portfolio with a first tranche. I found it quite attractively valued, despite the cooling housing market ✌️.

As a home builder, PulteGroup operates in a very cyclical market and is more or less a plaything of supply and demand as well as the supply chain problems and the associated price increases for building materials.

The biggest risk lies in the development of the US housing market (hence only a first tranche). For example, how will this perform in a recession? All I know is that there is a massive housing shortage due to the last few years.

In terms of valuation, PulteGroup is ridiculously valued with a P/E ratio of 4. The dividend is not that important, but the share buybacks are even more important (4% in Q1'22 alone).

What is your opinion?