Hello my dears,

Thanks to his many trips abroad, Juan is now very well connected and has made some good investors as friends worldwide. Who, of course, are always inspired by our company ideas.

Curious about the two value stocks from the med-tech sector, we received a call directly from Italy.

On the phone was investor friend Matteo. His first question was whether Juan had been reading too many Buffet books. Or why the sudden switch from momentum to value stocks is now taking place. There was also a comment on this yesterday at the Terumo presentation. The poor performance was criticized here.

My dears, the weakness in the Med. Tech sector has been going on for some time now. And since the last virus, the stocks are probably no longer so popular. We are now seeing dream P/E ratios for some stocks.

What do you think, do we need a new virus first, or should the stocks slowly regain investor interest even without a virus?

Matteo has also noticed that we have arrived in the med-tech sector and have therefore ended up in the value sector rather by chance.

Therefore, the sector was probably the reason for his call with the tip:

The Italian pharmaceutical industry is the second largest in Europe after the Swiss pharmaceutical industry with a total turnover of 56 billion euros in 2024. But according to Focus Money not yet in the focus of investors.

And so Matteo gave us the hint to take a look. $DIA (-0,75%) take a look.

Ladies and gentlemen, I hope you enjoy reading this while enjoying a glass of Doppio Passo or a cup of espresso.

And keep writing comments for Matteo.

DiaSorin S.p.A. specializes in the development, production and marketing of reagents for in-vitro diagnostics. The products are used in the treatment of infectious and viral diseases, thyroid diseases, cancer, etc.

It specializes in particular in infectious diseases, bone and mineral metabolism, endocrinology and oncology. DiaSorin offers tests and instruments that are used in hospitals, reference laboratories and other medical institutions.

In recent years, DiaSorin has also focused on the field of molecular diagnostics, further expanding its presence and relevance in the diagnostic community.

With 27 Group companies, six production sites and five research and development centers, DiaSorin S.p.A. is active worldwide. It is distributed through its own global network and independent distributors. DiaSorin was founded in 1968 as a division of Sorin Biomedica S.p.A. The company is headquartered in Saluggia (Vercelli), Italy.

At the end of 2025, the Group had 9 production sites in Italy, the United States (4), Canada, Germany, the United Kingdom and China.

Net sales are distributed geographically as follows: Italy (15.2%), Europe (24.9%), North America (51.8%) and other markets (8.1%).

Number of employees: 3,242

Consumables business is a clever sales model

According to Frank Fischer from Shareholder Value Management, the provider of tests for metabolic disorders has a "clever sales model" that is similar to that of Nespresso with its coffee capsules.

With the acquisition of US molecular diagnostics company Luminex in 2021, DiaSorin has entered a new dimension and strengthened its position in the US, its largest single market.

In addition to Italy, DiaSorin has production sites in the UK, the USA, Canada and Dietzenbach in Hesse.

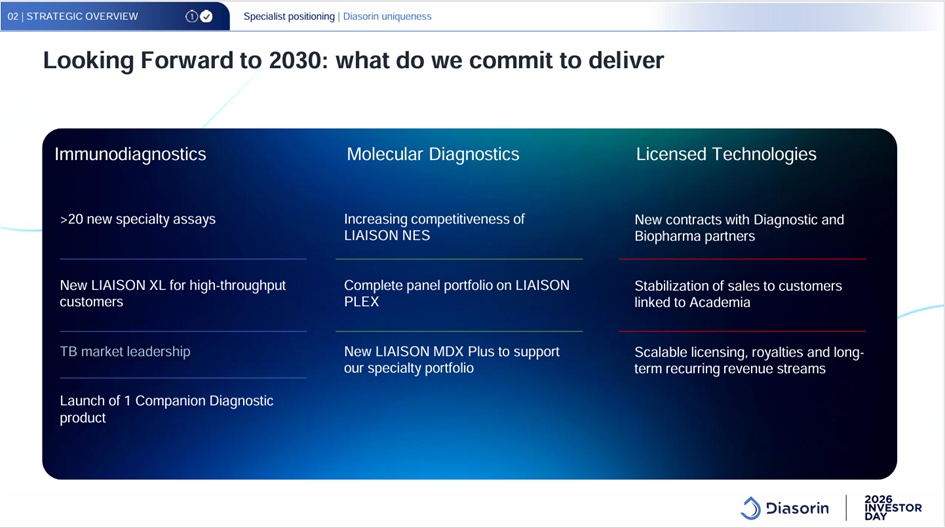

Diasorin's unique positioning: What does it mean to be a diagnostics specialist today?

Diasorin is a unique company because:

- It is not only active in a unique clinical specialty, but in all areas where specialized tests are needed.

- It is flexible in the face of competitive pressures and new emerging clinical opportunities.

- - Luminex strengthens R&D power in genomics, proteomics and clinical diagnostics

- - Strong market position through proprietary LIAISON® platforms

- - Growing demand for fast, precise multiplex tests

- - Stable healthcare exposure: less cyclical, high demand

- - Technology licensing business as an additional growth driver

- - Clear sustainability narrative strengthens institutional interest

- LIAISON® platforms as a scalable, high-margin core ecosystem

Diasorin Investor Day 2026-2030.pdf

19/03/26 - 9:47

Diasorin signs strategic distribution agreement with McKesson Medical Surgery to expand access to LIAISON NES molecular point-of-care platform

24/02/26 - 7:06

Diasorin partners with QIAGEN to launch next generation LIAISON QuantiFERON-TB Gold Plus II assay for the US

29/01/26 - 7:03

Diasorin has been granted de novo approval in the US for the first fully automated laboratory test for Hepatitis Delta Virus (HDV) on the LIAISON XL

26/01/26 - 7:09

Diasorin signs an exclusive distribution agreement for the LIAISON NES® molecular point-of-care platform and the Influenza A/B, RSV AND Covid-19 panel

DiaSorin: Decline in sales in the first quarter, annual forecast nevertheless confirmed

08,05,2026

DiaSorin - Q1/2026 report (short version)

Sales weaker, forecast remains unchanged - transitional quarter with clear negative factors.

1) Overall picture

- Sales in Q1/2026 -3 % (cc) resp. -8 % (reported).

- Earnings per share 0,85 $, slightly below expectation.

- Share reacts with -1,7 %.

- Annual forecast 2026 confirmed: Sales growth 5-6 % (cc), EBITDA margin 32-33 %.

2) Main reasons for the weak start to the year

- Strong currency effectEUR/USD significantly below plan; every cent costs € 6-8 million in sales.

- ChinaSales -20 % due to VBP price pressure.

- Mild flu season: Burdens molecular diagnostics.

- Timing effects for Licensed Technologies.

3) Segment performance

Immunodiagnostics

- Basic business ex-China +1 %.

- China -20 % (VBP).

- US hospital strategy is going well.

Molecular diagnostics

- Total -12 %.

- Automated multiplexing -1 %.

- Non-automated -50 %.

- Bright spot: Special tests +40 %.

Licensed Technologies

- -7 % due to weak life science demand and high basis for comparison.

4) Profitability

- EBITDA margin 31 % (previous year 34%).

- EBIT margin 20 % (previous year 23%).

- Net result -28 % to € 38 million.

- Gross margin stable at 65 %.

5) Balance sheet & cash flow

- Net debt increases to 711 million (previously € 580 million).

- Working capital +€ 18 million.

- Operating cash flow 58 million (previous year € 71 million).

- Equity decreases to 1,497 million.

6) Outlook for 2026 (confirmed)

- Sales growth 5-6% (cc).

- EBITDA margin 32-33 % → Clear improvement compared to Q1.

- Growth driver from H2/2026:

- LIAISON NES Rollout

- New PLEX panels (GI panel expected in H1/2026)

- Normalization of volumes

- Stabilization China

7) Risks

- Currency effects (EUR/USD).

- China price pressure (VBP).

- Geopolitics / possible tariffs.

- Dependence on flu season until GI panel is approved.

- 8) Ultra-short Juan conclusion

- "Weak Q1, but no structural damage: Currency, China and flu weigh - but platform story (NES + PLEX) remains intact and H2/2026 should be much stronger."

Key statements

- DiaSorin expects sales growth of 5-6% in 2026.

- For 2026-2030 the company is forecasting a average annual growth rate (CAGR) of 6-8% . in prospect.

- The adjusted EBITDA margin should

- 2026: 32-33 %,

- by 2030: 34-35% reach.

- Between 2027 and 2030 DiaSorin plans to generate cumulative free cash flow of around € 1 billion.

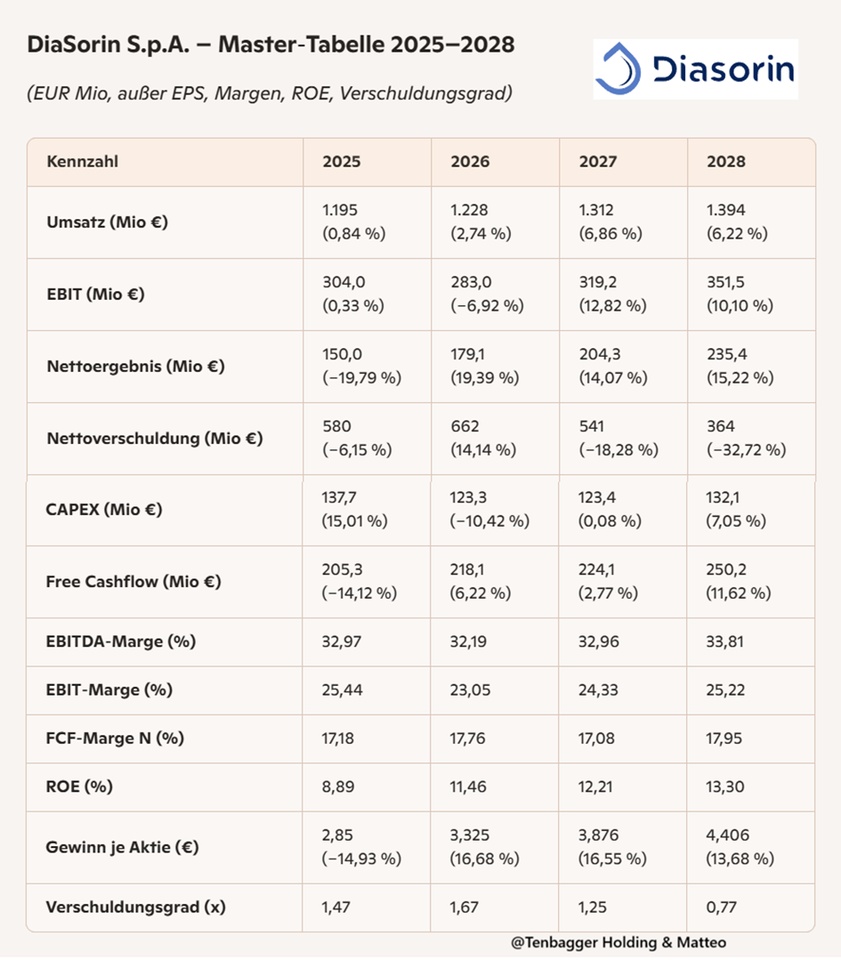

Juan's conclusion (short & sweet):

"DiaSorin delivers clean, steady numbers: Sales are growing steadily, margins remain strong, cash flow is picking up and debt is falling significantly - a quality MedTech with a clear recovery curve."

Market value 3,424

Number of shares (in thousands) 53,001

Date of publication 20.03.2026

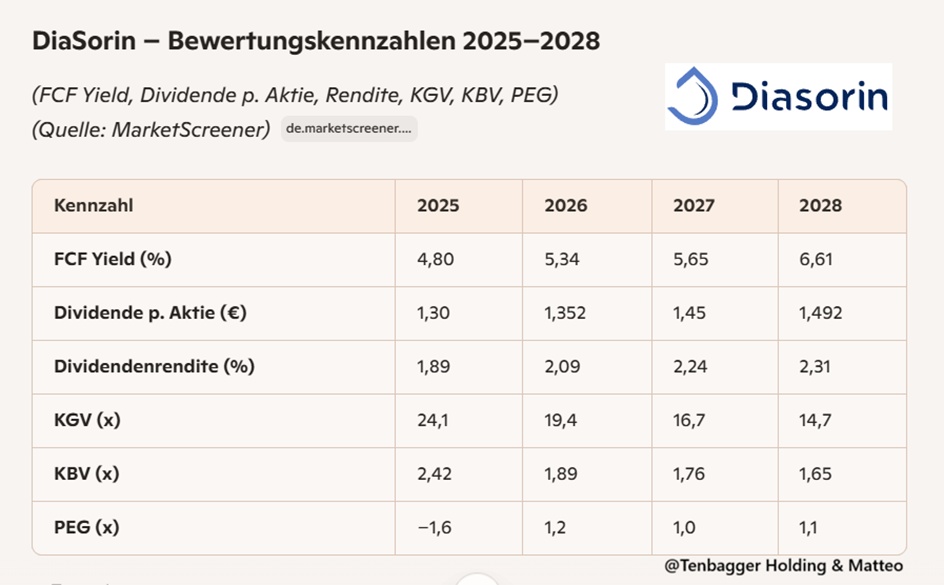

Juan's conclusion on the valuation ratios:

"Valuation is getting cheaper every year, cash flow yield is rising cleanly, dividend is growing steadily - DiaSorin is slipping from expensive to fairly valued and at the same time delivering quality that you don't normally get so cheaply."

IT DOESN'T GET ANY CHEAPER

The key figure with the highest stability for the Diasorin share is the operating cash flowwhich is used below for the valuation. The KCV calculated from this key figure KCV (price/cash flow ratio) calculated from this ratio is 11.22 which is 8.86 points below the historical average of 20.08 for the last 10 years. From this perspective, the Diasorin share appears to be favorably valued to be favorably valued.

The fair value of the Diasorin share is calculated over the 10-year valuation period selected above. The average KCV in this case is 20.08.

Multiplied by the operating cash flow per share of EUR 5.81 over the last 4 quarters, this results in a fair value for the Diasorin share of fair value of EUR 116.69. The current share price of EUR 64.60 is 44.6% below this fair value, which corresponds to an undervaluation of the share.

(Source share finder)

22.05.2026, 22:02:49 -

Tradegate BSX (EUR)

64.38 EUR