21.10.2024

iPhone 16 gets off to a strong start: Apple registers 20% more sales in China + SAP is too valuable for the German stock exchange + DAX outlook: 20,000-point mark remains firmly in sight + 11 DATEs that will be important this week + Jefferies lowers Munich Re to 'Hold' - target 485 euros

Apple $AAPL (+0,65%) can score points in China with a successful launch of the new iPhone 16. According to a Bloomberg report based on data from Counterpoint Research, sales in the first three weeks after the market launch were 20 percent higher than the previous year's model, with the more expensive versions of the new iPhone doing particularly well. Sales of the Pro and Pro Max models increased by 44 percent. According to Counterpoint analyst Ivan Lam, the start of production of the iPhone 15 last year was still characterized by supply bottlenecks, which slowed down the initial sales figures. These problems have largely been overcome with the iPhone 16.

The software company SAP $SAP (-0,4%) was the first to reach the new DAX cap of 15 percent. What now? Over the past year, the value of the German software group SAP has risen sharply. The company is currently valued at 212 euros per share on the Dax. Twelve months ago it was less than 130 euros.

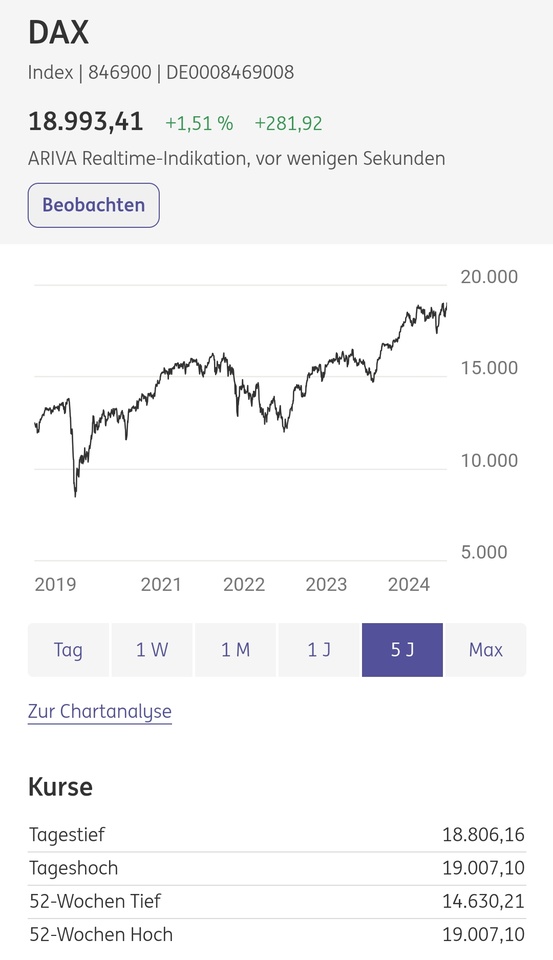

With an increase of around 0.4 percent to 19,657 points, the DAX $GDAXI went into the weekend last Friday. This means that the stock market barometer could launch another attack on the 20,000-point mark in the coming week. Investors can find out which topics could influence the price trend in the DAX outlook. Do you think the 20,000 points will fall?

The analyst firm Jefferies has Munich Re $MUV2 (-0,5%) from "buy" to "hold" and lowered its price target from 495 to 485 euros. In a study published on Monday, analyst Philip Kett mentioned that the reinsurer's share price had reached record highs despite Hurricane Milton. He reassessed his estimates and came to the conclusion that there was hardly any room for rising market expectations. His price target had already been exceeded.

11 DATES that will be important this week

1 China's central bank cuts key interest rates

The People's Bank of China is likely to ease its monetary policy further. Analysts expect it to lower its reference rates for 5-year and 1-year corporate loans to 3.65% (currently: 3.85%) and 3.15% (3.35%) respectively. This expectation is not only fueled by the announcement of comprehensive economic policy measures to stimulate growth, but also by statements made by central bank governor Pan Gongsheng. According to reports in the Chinese local media, he held out the prospect of a reduction of 20 to 25 basis points at an event.

>>> Monday, October 21, 2024; 3:00

2nd IMF hardly changes growth forecasts - focus on government debt

Economists and politicians are meeting in Washington for the annual meeting of the International Monetary Fund (IMF) and World Bank. The agenda initially includes the publication of the current World Economic Outlook (3.00 p.m.) and the Global Financial Stability Report (4.15 p.m.) on Monday, followed by the Fiscal Monitor on Tuesday (3.00 p.m.). The opening speech by IMF chief Kristalina Georgieva indicates that the IMF will primarily discuss the high and rising level of public debt and look for ways to strengthen economic growth in order to improve debt sustainability. There will also be no shortage of calls for austerity. The finance ministers and central bank governors of the G20 will meet on Thursday.

>>> Monday, October 21, 2024, 15:00

3. SAP $SAP (-0,4%)defies the weak economic environment

SAP appears to be unaffected by the weak economy. According to analysts' expectations, the Group seamlessly continued the growth of its cloud business in the third quarter. Even slight disruptive factors such as investigations in the USA and the departure of three board members have not thrown the Walldorf-based software giant off track. SAP will present its figures on Monday shortly after 22:00 after the close of the US stock exchange. An analysts' conference will take place at 23:00.

>>> Monday, October 21, 2024; 22:05

4. deutsche Börse $DB1 (+0,12%)remains on course for growth with Simcorp

Deutsche Börse should have remained on course for growth in the third quarter. The figures are likely to be characterized by the integration of Simcorp and a good development in the Trading & Clearing division. The exchange operator will probably confirm its targets for the year as a whole. Larger acquisitions are currently not an issue, not only because of the ongoing integration of Simcorp, but probably also due to the change in the Group's top management.

>>> Tuesday, October 22, 2024; 19:00

5th Deutsche Bank $DBK (-2,66%)with good investment banking - Postbank helps

The fact that Deutsche Bank is currently attracting less attention than a certain Frankfurt-based competitor is unlikely to be changed by the third quarter report. The bank will deliver solid figures and confirm its targets. Although the bank recently had to raise its forecast for risk provisioning, things are going well in the investment bank. CFO James von Moltke recently said that significant growth is expected, particularly in the M&A and issues business. The bank will also see a positive effect on earnings from the reversal of the Postbank provision, as it will not need the full EUR 1.3 billion for the settlement with the former Postbank shareholders. In this context, statements on new share buybacks should also be of interest.

>>> Wednesday, October 23, 2024; 7:00 a.m.

6 Beiersdorf $BEI (-0,46%)on the home straight after the summer quarter

After the first nine months, Beiersdorf should be on track for its full-year targets for both sales and EBIT margin. The summer quarter is likely to have benefited from strong demand for sun protection and the derma skin care brands. The innovation Epicelline and the launch of Eucerin Face in the USA should also be well received. On the other hand, further declines in sales for the luxury cosmetics brand La Prairie in China. Nevertheless, organic sales growth at Group level and in both the Consumer and Tesa segments is likely to have been in line with the target range - with Consumer tending towards the upper end and Tesa and the Group towards the lower end. Following a pull-forward effect in the second quarter, Tesa could deliver somewhat weaker results in the third quarter. With the second quarter figures, Beiersdorf had explained that the development in the US market and at La Prairie in the second half of the year would be decisive for the positioning in the target range.

>>> Thursday, October 24, 2024; 07:00

7. symrise $SY1 (+1,32%)could raise the forecast

Symrise is likely to have increased sales and margins in the third quarter. According to analysts, strong sales in both divisions and better pricing should have contributed to this. The focus is on the forecast. In August, CFO Olaf Klinger held out the prospect of a review after the end of the quarter and a possible increase - which is expected by the market. However, analysts at UBS also point out that the fragrance and flavor manufacturer usually gives conservative forecasts. Investors may also ask about the planned sale of the business with ingredients and flavor enhancers for feed for fish farming.

>>> Thursday, October 24, 2024; 07:30

9. Mercedes-Benz $MBG (-3,33%)burdened by weakness in China

Burdened by the weak market environment and increasing price pressure, Mercedes-Benz recently had to lower its outlook for this year twice within a short space of time. The reluctance to buy has hit the DAX-listed company particularly hard in China, where sales of particularly expensive and high-margin luxury cars have increasingly lost momentum. However, there are also positive aspects that analysts are emphasizing at the Stuttgart-based premium car manufacturer, such as its commitment to the dividend payout ratio and share buybacks. The management should emphasize this again when presenting the quarterly figures so that the mood does not change even more.

>>> Friday, October 25, 2024; 07:30

10th Ifo business climate index rises in October

Economists expect the Ifo Business Climate Index to have risen again in October for the first time since April - to 85.6 (September: 85.4) points. Nevertheless, the situation of the German economy is tricky. From a cyclical perspective, an Ifo increase would indicate an improvement. Energy prices are no longer weighing so heavily on the economy and the effects of high key interest rates are slowly easing. However, the structural problems in the automotive industry, which is so important for Germany, are likely to persist for some time to come, and the rest of the export-oriented industry will also have to adjust to the new geopolitical conditions for some time to come.

>>> Friday, 25.10.2024; 10:00

11. at Porsche $P911 (-1,22%)everything depends on the final quarter

The situation at Porsche has become increasingly gloomy in recent months. It was already foreseeable at the beginning of the year that the many model changes would entail high expenses and that the environment in China would be difficult. However, this was recently compounded by delivery problems, production interruptions and considerably tougher competition. When the figures for the third quarter are presented, analysts are only expecting a return of just over 11 percent - but Porsche is aiming for 14 to 15 percent for the year as a whole. The management's comments on the final quarter will therefore be the linchpin in terms of target achievement.

>>> Friday, October 25, 2024; 17:30

Monday: Stock market dates, economic data, quarterly figures

ex-dividend of individual stocks

CVS Health USD 0.67

Caterpillar 1.41 USD

Bank of New York Mellon USD 0.47

Husqvarna (B) SEK 2.00

Quarterly figures / company dates Europe

03:00 Logitech quarterly figures

07:35 Forvia SE sales 3Q

18:30 Metro Trading Statement 4Q

22:05 SAP quarterly figures

23:00 SAP Analyst Conference

Economic data

- 08:00 DE: Producer prices September FORECAST: -0.2% yoy/-1.0% yoy previously: +0.2% yoy/-0.8% yoy

- 16:00 US: Index of leading indicators September FORECAST: -0.3% yoy previous: -0.2% yoy

- 19:30 US: Federal Reserve Bank of Minneapolis President Neel Kashkari speaks at Chippewa Falls Area Chamber of Commerce event

- 23:00 US: Federal Reserve Bank of Kansas City President Jeffrey Schmid speaks at CFA Society Kansas City event