Hello my dears,

our good @Dividendenopi (Gartenopi), mentioned in a comment yesterday that he was still looking for an exciting stock with a good dividend yield in the industrial sector.

When I then mentioned a space stock, he must have @Klein-Anleger had to smile a little. And he commented:

"There's no such thing as a space company paying dividends".

I'm really looking forward to the comments that I've managed to find a company.

I really like this one:

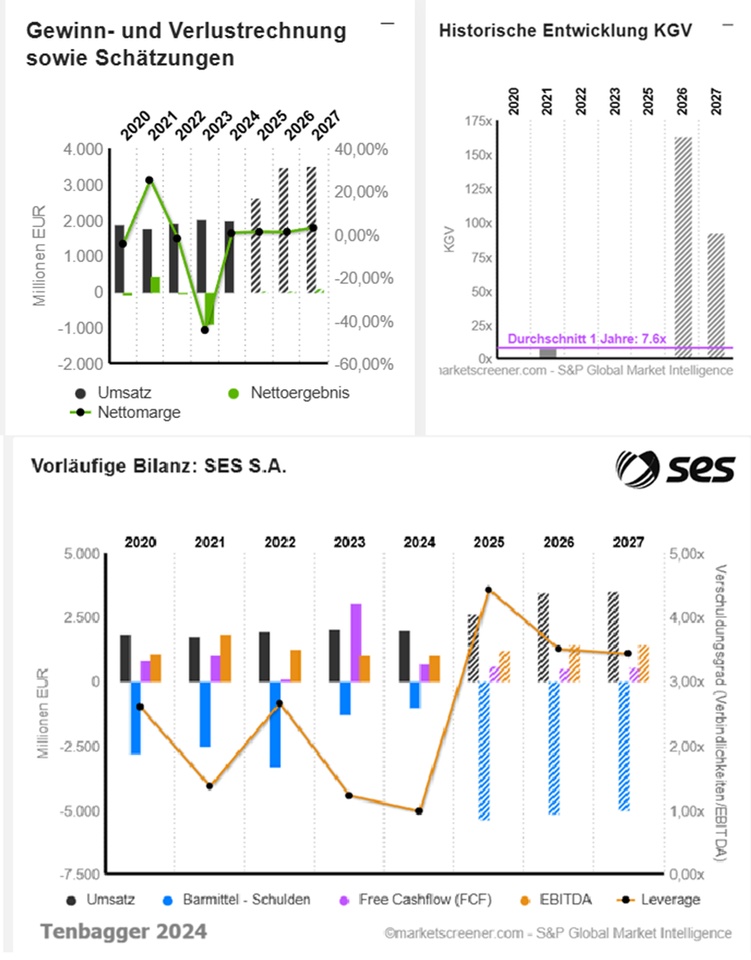

- In 2027, the net result will grow by +203 %

- Free cash flow remains constant (nevertheless, one should keep an eye on the debt)

- EBIT margin and ROE increase well (but are not overwhelming, but good compared to other satellite operators. These often do not have a positive EBIT margin and are not profitable).

- Dividend yield increases to an excellent 9 %

- 82 % annual performance, despite high dividend yield (Growth and dividend)

- P/E ratio falls and the PEG is then a good 1.2x

My dears, what do you like and what don't you like?

You should all be aware of the potential in the sector by now.

SES S.A. specializes in satellite communication and media transmission solutions. With a fleet of around 120 satellites in two different orbits, geostationary orbit (GEO) and medium earth orbit (MEO), SES is positioning itself as a global player offering connectivity and video transmission on land, at sea and in the air. The expansion was accelerated by, among other things, the completed acquisition of Intelsat in July, making SES a global powerhouse in multi-orbit connectivity.

The company aims to increase profitability through targeted investments in new technologies and the modernization of its satellite fleet. Particular attention is being paid to the O3b mPOWER system, a satellite constellation in the MEO that provides high-performance connectivity for governments, mobile network operators and companies. Last year, the Group announced the placement of a dual-tranche bond with a volume of EUR 1.0 billion in June. This provides the Group with the necessary liquidity for future investments and expansion.

On September 25, European shares from the "space technologies" trend saw positive price reactions. The trigger was the announcement by German Defense Minister Pistorius that a total of EUR 35 billion would be made available for space projects and a security architecture in space by 2030. The initial reaction of SES S.A. was positive. The share stabilized at the GD 20 and thus laid the foundation for the next upward wave. In this scenario, the share could prepare to break out of the consolidation that has been ongoing since June and reach a 52-week high.

SES S.A. has a bold vision to deliver captivating experiences by distributing the highest quality video content and providing seamless connectivity around the world, anywhere in the world. As a leading provider of global content connectivity solutions, SES S.A. operates the world's only multi-orbit satellite constellation with a unique combination of global coverage and high performance, including the commercially proven low-latency O3b system in medium Earth orbit. By leveraging an extensive and intelligent cloud-enabled network, SES S.A. is able to deliver high-quality connectivity solutions anywhere on land, at sea or in the air. SES S.A. is a trusted partner for the world's leading telecommunications companies, mobile network operators, governments, connectivity and cloud service providers, broadcasters, video platform operators and content owners.

SES S.A.'s video network broadcasts more than 6,300 channels and has an unrivaled reach of around 362 million homes. The company provides managed media services for linear and non-linear content.

Number of employees: 2,118

- Luftfahrt

- Cloud

- Kreuzfahrt

- Energie

- Regierung

- Maritim

- Telekommunikations- und MNO-Unternehmen

- Medien & Rundfunkanstalten

- Sportorganisationen

ACQUISITION OF INTELSAT: A WINNING COMBINATION

Geographical distribution of revenues: SES S.A.

Year 2024

U.S.A. 713 million

Others 406 million

Germany 321 million

Others Europe 205 million

United Kingdom 203 million

Luxembourg 79 million

France 74 million

EUR in millions

Estimates

Year Turnover Change

2024 2.001 -1,43 %

2025 2.631 31,46 %

2026 3.490 32,68 %

2027 3.514 0,69 %

2028 3.566

Year EBIT Change

2023 -686 -590 %

2024 64 109,33 %

2025 85,33 33,33 %

2026 198,7 132,81 %

2027 287,3 44,63 %

2028 391,33

Year Net result Change

2023 -905

2024 15 101,66 %

2025 30,48 103,21 %

2026 35,96 17,97 %

2027 108,9 202,98 %

Year Net debt CAPEX

2023 1.252 405

2024 999 303

2025 5.391 675,8

2026 5.140 608,3

2027 5.005 730,7

Year Free cash flow Change

2023 3.074 2419,67 %

2024 703 -77,13 %

2025 599,7 -14,7 %

2026 521,5 -13,04 %

2027 566,2 8,57 %

Year EBIT margin ROE

2023 -33,79 % 4,63 %

2024 3,2 % 3,54 %

2025 3,24 % 9,34 %

2026 5,69 % 10,72 %

2027 8,18 % 12,43 %

Year Earnings per share Change

2026 -0,08

2027 0,08 +241,83 %

2028 0,23 +229,11 %

Year Dividend Yield

2023 0,5 8,39 %

2024 0,5 16,3 %

2025 0,5 7,69 %

2026 0,55 8,46 %

2027 0,59 9,08 %

Year P/E ratio PEG

2025 -38,2x

2026 163x -1x

2027 92.9x 1.2x

Market value 2,716

Number of shares (in thousands) 417,898

Date of publication 26.02.2025

Performance

1 week -1.44 %

1 month -3.63 %

6 months +10.45 %

1 year +82.38 %