+++ Stock analysis of Clinuvel Pharmaceutical: +++

$CUV (+3,85 %)

Pharmacy of the future?

Outline of the article:

1. introduction

2. how did I come across the share?

3. company analysis including company history

4. financial ratios

5. who is invested?

6. current problems/opportunities

7. dividend

8. moat analysis

9. my opinion on the share

1. introduction

Today there is again a small stock analysis as a Getquin contribution. Today's analysis is dedicated to a very exciting pharmaceutical company that might just be at the beginning of its career.

First of all: Out of bias I disclose that I am invested in Clinuvel. This article is only meant to give you a closer look at this (still) small company.

As it has always been the case with my stock analyses so far, I introduce the analysis with a little joke.

Doctor: "So, Mr. Meier, you are drunk again, didn't I tell you only one bottle of beer per day?"

Meier: "Yes, do you actually think you are the only doctor I go to!

Source: https://witze.net/arzt-witze

(Since I did not use any pictures/graphs in the last stock analysis (Deutsche Post), I would like to use them in this post).

2. how did I come across the share?

Very few people know that I am a fan of Florian Homm. I like to read his books, as I am fascinated by his career and appreciate his analytical skills. (I am aware that Florian Homm is a bit of a crash prophet :)). Through his biography "Head Money Hunting", I first came in contact with the stock market, I was then a 16-year-old boy who dreamed of getting rich quick, and doing little for it. Today I am smarter. Already in his biography Homm mentioned his success with the then penny stock Clinuvel, which has increased more than tenfold due to him as an activist hedge fund manager. (Not verified). Homm also devotes special consideration to Clinuvel in other books, and special YouTube videos. If a legendary hedge fund manager thinks so highly of a small Australian company, there must be something to it - right? That's an easy question to answer at the end of this post.

Sources: Book:

- The Principles of Wealth; Moritz Hessel and Florian Homm; Finanzbuchverlag.

- Book: Head Money Hunting; Florian Homm

3. company analysis including company history

Clinuvel Pharmaceutical is a specialized pharmaceutical company that develops drugs for genetic, metabolic (metabolic), life-threatening and common diseases. The drugs are mainly marketed to industrialized countries. The geographic distribution of sales is dominated by Europe and the USA (89%). 11% of sales come from Switzerland and other countries. The company was founded in 1987 by specialist researchers who set out to find a drug for EPP (skin disease). Then, in 2006, the first studies were conducted until Europe (2014) and the U.S. (2019) gave their permission to market the drug. In 2020, Clinuvel announced that a new drug (Prenumbra) was in development.

On the company's website, it is written that Clinuvel is a specialty pharmaceutical company whose goal is to serve the open needs of patients. It is further written that Clinuvel is particularly interested in diseases for which there are currently no alternatives. For investors, this strategy is worth its weight in gold, because health insurance companies/individuals are forced to pay high prices for medicines without substitutes. Because health is important to everyone. (No valuation of this strategy from my side).

Sources:

- https://www.worldofvalue.de/beitrag/clinuvel-pharmaceuticals-211210

- CLINUVEL PHARMACEUTICALS LIMITED : Aktionäre Vorstände Geschäftsführer und Unternehmensprofil | A0JEGY | AU000000CUV3 | MarketScreener

4. financial ratios

As I mentioned earlier, I am invested in Clinuvel. The decision to buy the stock was influenced by the company's very strong financials. Why I am so convinced about the company, you can see now:

Before I put a company in my portfolio, I first look at the financial stability, so especially the debt, etc., to make sure that my investment will not go bust. Clinuvel's debt is low, as the company has a debt-to-equity ratio of 14%. For comparison, the pharmaceutical giant John Sohn and John Sohn has a debt to equity ratio of 145%.

Source: Own representation: Calculated with data from www.yahoo.finance.com

Clinuvel also shines when it comes to gearing. The definition of gearing is as follows: "Das Gearing is a measure of the financial Hebelwirkung of the company , showing the degree to which a company's activities are financed by shareholders' funds compared to creditors' funds." A good gearing is close to zero or tends to negative. In the case of Clinuvel Pharmaceuticals, gearing has been consistently between -70 to -85 for the past 4 years, showing that the company is liquid even in the current times, and is not in danger of filing for bankruptcy. Most people have noticed that key interest rates around the world are being raised in order to fight inflation. Accordingly, interest coverage is important for a company. By calculating interest coverage, you can see whether a company can easily or heavily repay its debts. Clinuvel has no problems here either. The interest cover in 2022 is 141 times. By comparison, Deutsche Post has "only" an interest cover of 13.8 (2022).

Sources:

- https://www.investopedia.com/terms/g/gearingratio.asp

- Calculation: Own presentation

In addition to financial stability, the profitability of a company is of course also important. Based on gross profit margin and operating profit margin, one can quickly see whether a company is doing well or poorly. Both key figures are excellent at Clinuvel. The gross profit margin varies between 90% and 84% (surveyed period: 2020-2022). The operating profit margin is also convincing with a solid value of 55% (2021). The fact that Clinuvel has such high margins can be attributed to its business model. This is because Clinuvel, as a pharmaceutical company, only has to raise large sums for research and approval. After the drugs have been approved by the EFSA and the FDA, the sale of the drugs generates "passive income." This is because Clinuvel only needs to have the drugs mass produced and distributed. By producing drugs for rare diseases for which there is no second cure on the market, Clinuvel leaves health insurers no choice but to pay whatever price CUV deems appropriate.

The return on invested equity is also noteworthy. This describes the return one receives on one's invested capital. (Roe). The Roe was 35% in 2021 and 28% in 2022.

In order to buy a company as cheaply as possible, one must pay attention to a wide variety of valuation ratios. These help to understand, based on historical data, whether a company is currently cheap to buy.

Three important ratios are enterprise value/EBIT; EV/EBITDA and EV/Sales. If these ratios are low and the company has no fundamental reasons to depreciate in value, a low value may indicate a buying opportunity.

The above valuation ratios have been falling for the past three years at Clinuvel. It is important to note that Clinuvel was a hype stock that traded too high. At its all-time high, Clinuvel was a popular stock for short-sellers who made a lot of money by penalizing the stock. Due to the fact that the ratios are now at a fair value, I decided to buy the stock.

According to forecasts, the share's price-to-book value and cash flow should increase steadily in the coming years. This suggests that the stock is now growing steadily and slowly as CUV increases its sales of existing drugs and as new drugs come to market.

5. who is invested?

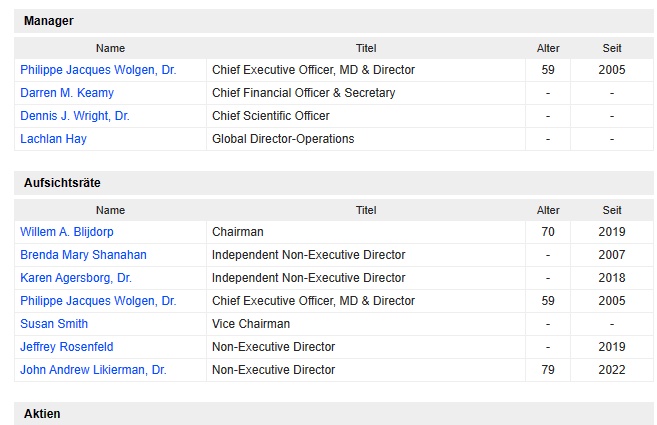

Control is good, trust is better! This proverb can also be applied well to the stock market. CEOs have control over the companies you invest in and accordingly have more accurate insights into what is going on with the companies. Therefore, I like to see the CEO speak positively about the future about a company. However, it is better when the boss underlines the vote of confidence with an insider buy. This is the case with Clinuvel, because the main shareholders are:

1. Dr. Wolgen (CEO; 6.3%)

2. Ender 1 GmbH (5.2%)

3. Dr. Bljord (Chairman of Clinuvel; 3.5%)

4. Bedcock (2.4%)

5. Vanguard (2%)

Based on the major shareholder structure, you can see that the CEO and Chairman of the company have invested a lot of money in the company. To me, this is an extremely positive signal for the future. Moreover, Dr. Wolgen writes in the annual report to the shareholders that they are very important to him and he is positive about the future of the company. He also notes that short-sellers will only be interested in CUV in the short term, and that's why you shouldn't sell your shares.

Source:

- CLINUVEL PHARMACEUTICALS LIMITED : Aktionäre Vorstandsmitglieder Manager und Unternehmensprofil | AU000000CUV3 | MarketScreener

- www.DATAROMA.com

- Annual report (2021)

6. current problems & opportunities

To understand risks and opportunities at Clinuvel, one must take a closer look at the company's business. I will now take a closer look at the drugs and their processes. Since I myself am not a medical specialist, and I do not want to do that to you, I will try to explain everything simply.

All mentioned information can be found on Willkommen bei CLINUVEL - Clinuvel findable.

1. The DNA repair program

The program targets skin cancer caused by ultraviolet radiation by causing DNA damage. The target group of the drug SCENESEE, are people suffering from Xeronderma pigmentosum. This is a congenital disease that prevents DNA repair. As a result, those affected must avoid the sun, as the UV radiation will otherwise lead to aggressive skin cancer. The mortality rate of the disease is high, and the life expectancy is 30 years. It is estimated that 1 person in 450,000 people in Europe suffers from the disease.

The solution:

Clinuvel's drug aims to increase DNA repair capacity and alleviate the consequences of regular tumor removal. Currently, the drug has been successfully tested and approved in phase 1,2,3. The latest news was that it is now being tested on adolescents for efficacy. If this trial is successful, the lives of affected children will improve significantly.

"SCENESSE (afamelanotide 16mg) is approved in the European Union as an orphan drug for the prevention of phototoxicity in adult patients with erythropoietic protoporphyria (EPP). SCENESSE is approved in the United States to increase "pain-free" light exposure in adult EPP patients with a history of phototoxicity. Information about the product can be found on CLINUVEL's website at. www.clinuvel.com"

2. Arterial Ischemic Stroke

A stroke occurs when important blood vessels (carry oxygen and nutrients) become blocked by clots. As a result, the brain suffers from a lack of oxygen and is damaged. Current methods involve chemically dissolving the clot or physically removing it. Nevertheless, these methods are quite ineffective because treatment must happen quickly after the stroke. Because treatment is often not given quickly enough, the stroke is usually fatal or ends in permanent disability. Every year, about 15 million people suffer a stroke. 5.5 million do not survive it. 50% of the survivors suffer from a permanent disability afterwards. Dementia is also often a consequence of strokes.

Solution:

Clinuvel is currently researching a drug that will restore a stroke patient's neurological and muscular functions. This happens by improving blood flow to the brain. Clinuvel focuses primarily on patients who cannot be treated by conventional methods because the affected area of the brain cannot be reached. Dr. Bilbao of Clinuvel states the goal is that 70-80% of stroke patients who are not helped by conventional treatments will benefit from the New Method.

The new drug is called afamelanotide, and has the advantage of acting as a powerful antioxidant hormone. So the patient's brain is protected by reduced fluid formation and restoration of the blood-brain barrier.

Personally, I am extremely grateful about the research of doctors on this subject, and hope that this method will be used in the future, and many lives will be saved.

3. Light protection through pigmentation

Everyone should know that the contact between skin and the sun's UV rays is not good. This is because this contact causes sunburns, DNA damage (skin cancer) and photoaging. People with lighter skin (Europeans, etc.) are generally more affected by these consequences.

Solution:

Clinuvel is developing melatonin medication, is responsible for tanning the skin, to reduce these consequences. Implanted melatonin makes it possible to tan without UV rays. As a result, the skin does not react so violently to the UV rays. Side effect: people with white spots on their skin are enabled to balance their skin color.

Now to the evaluation of chances and risks:

The opportunities for the pharmaceutical company are obvious. Through the successful approval of the drugs, new sources of money are gained, which incidentally can save millions of people. Personally, I find all the tested methods and drugs more than sensible and almost revolutionary. With the approval of the health authorities, a global expansion can then take place, which can make the company and the shareholders rich.

The risks, on the other hand, are that the company will not get the approvals and the funds spent will have been "wasted". There is also the risk that Clinuvel will be acquired by a larger pharmaceutical company. The company has a current market capitalization of 600 million.

Sources: Pharmazeutische Technologie - Clinuvel

For me personally, the opportunities outweigh the risks, which is why I am a shareholder in the company.

7. the dividend

The company's current dividend yield is 0.22% ($0.04). Based on the last dividends, you can see that the company has increased the dividend every year. On average, 60-70% per year. The financial situation suggests that the company can easily sustain the dividend and there is clearly room for increase. But I feel comfortable with the low dividend, as the funds should rather be spent on future drugs and research.

Source: https://www.marketscreener.com/quote/stock/CLINUVEL-PHARMACEUTICALS

8th Moat Analysis

A company without a strong moat is weak against its competitors. Therefore, a company's moat must be examined.

1. intangible assets

Clinuvel has strong patents in addition to real estate (research laboratories). These patents are unique and the drugs have no serious competitors: PRICING POWER. Licenses and registrations also belong to Clinuvel

2. switching costs

As Clinuvel is mainly active in the USA/Europe and Switzerland, the company earns "strong" currencies. Exchange costs are therefore rather low. (May come with expansion into third countries).

3. network effect

Pharmaceutical companies like Clinuvel have a strong network effect, because the value of the products increases with demand. With pricing power and a high chance of scaling, there is a high chance that Clinuvel can benefit from a network effect.

4. cost advantages

Based on the high profit margins, one can see that the company is very profitable. These profit margins are easily scalable and grow with production. The chance that many pharmaceutical companies will invest in the same methods to produce their own product in the future is low, otherwise the profit margins of both sides will be very reduced.

5. good management

The point: who is invested clearly shows that the company management is very competent, and have strong confidence in the company. In addition, the CEO continues to strive to expand the company's drug portfolio. In my opinion, the management is very good!

6. geographical differences

Australian companies have no disadvantages compared to European/ American companies.

7. minimum efficient size

This is where top dog Clinuvel scores, as there are few competitors in the segment: melatonin, stroke drugs and DNA repair program. People depend on these drugs, and they don't care where it comes from - it has to work.

8. dependence on suppliers

Clinuvel has companies manufacture the drugs for them. If one supplier can't deliver/produce, another is found (time lost). But no direct dependence. Secured products through patents.

Lastly, a classification from me. I am fundamentally and ethically convinced of Clinuvel. The company produces helpful medicine and can market it profitably. I am invested, and will continue to invest if progress is good. There is also a chance that larger funds can list the stock. The current problem is that large funds like BlackRock or Vanguard are only allowed to invest minimally in Clinuvel, otherwise price manipulation could occur. I don't know the exact market capitalization at which large asset managers will be allowed to invest in large amounts, but I suspect it to be more than 1.5 billion.

I see Clinuvel in good hands in the future and I am a happy shareholder :)

And as always:

IMPORTANT: As with the last analysis, PLEASE give me some constructive feedback. Info you are missing or suggestions for improvement will be greatly appreciated. And another big thank you for all the positive feedback on the Deutsche Post analysis. Feel free to suggest a company in the comments that I should analyze next.

In this sense, have a relaxing weekend.

Image sources: www.clinuvel.com