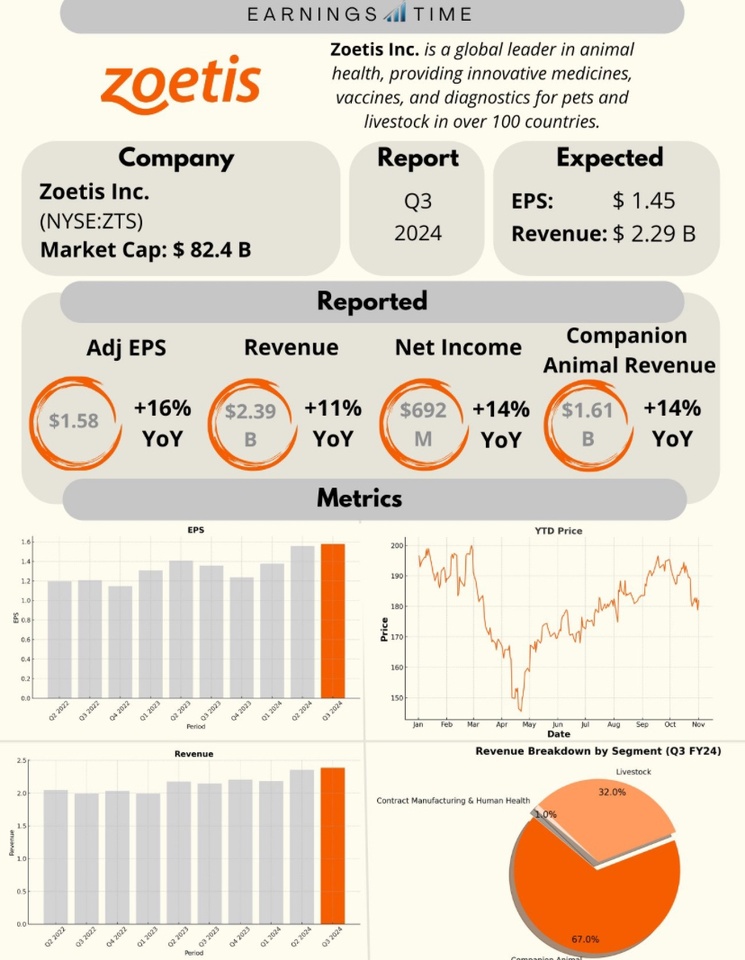

#Zoetis Inc., $ZTS (-1,1 %), Q3 FY24 Results:

📊 Adj EPS: $1.58 🟢

💰 Revenue: $2.4B 🟢

📈 Net Income: $682M

🔍 Raised FY24 revenue guidance to $9.2-$9.3B with expected 10-11% growth.

Postes

18#Zoetis Inc., $ZTS (-1,1 %), Q3 FY24 Results:

📊 Adj EPS: $1.58 🟢

💰 Revenue: $2.4B 🟢

📈 Net Income: $682M

🔍 Raised FY24 revenue guidance to $9.2-$9.3B with expected 10-11% growth.

Hello stock market friends,

I would be interested in your assessment of my Quality Growth portfolio.

I currently feel comfortable with the portfolio, even though it is very technology-focused.

My approach is to only buy absolute quality companies with positive growth prospects at fair valuations. Some companies are simply rarely available at fair valuations ($ANET (-2,69 %)

$SNPS (-1,54 %) and co.), which is why I am prepared to add such companies with strong moats to my portfolio at a premium.

I am currently considering whether $MSCI (-0,16 %) after the market punished the last quarterly figures.

I am also keeping a closer eye on $ZTS (-1,1 %) more closely due to the recent setbacks. Fundamentally, the company is still operating excellently and is starting to look more attractively valued than it did a few months ago.

What stocks do you know that could be a good addition to my portfolio?

LG

I know that advertising is not welcome here😉 but if you want you can watch my new video about $ZTS (-1,1 %) . After the recent price drop, I think they are relatively fairly and interestingly valued. What do you think of Zoetis?

$ZTS (-1,1 %) You are close to the 52-week low, if the support holds it may go up again. Pros are the high market value, the company makes a profit and pays dividends. Cons are the fundamental data such as P/E ratio and P/B ratio. I will take a look at $ELAN (-0,41 %) , $PETS (+0,76 %)

$PETQ in the watchlist

New addition to the depot: Zoetis

While classic pharmaceutical stocks should be well known to most, animal health is less in the spotlight.

#zoetis Zoetis is the global market leader here with medicines, vaccines, diagnostics, etc.

In recent years, a significant premium has always been paid, but this is comparatively low due to recent sales.

I therefore saw an entry opportunity and built up an initial position.

Animal health is a megatrend, as pets are becoming increasingly humanized. Pets are being treated like "real"/human family members - in the truest sense of the word.

I also see a strong positioning in the face of possibly more persistent inflation, as fewer savings are being made on pets.

At the latest at $130, I would increase significantly.

How do you rate the company? How do you see the short/medium/long-term prospects?

Hello everyone,

Today I would like to introduce you to my portfolio. As you probably know, it's just too much fun to expand my portfolio with new stocks. There are now a few too many, but I still can't really part with my worst-performing stocks ($NVM (-0,85 %) , $ENPH (+6,25 %) , $WAC (+3,22 %) ). I'm hoping that I'll be able to sell them in positive territory at some point, or am I on the wrong track and in your opinion should I sell at a loss and try to make up the loss with other stocks?

I have been investing since the end of 2022 and at 29 years old, I still have a long time to go. My strategy is to be as desertified as possible in sectors and to beat the market in the long term (just let me believe that it works :D), hence so many individual stocks. I want to hold these for many years (esp. $AMZN (+1,1 %) , $GOOGL (+0,56 %) , $QCOM (-0,16 %) , $MSFT (-1,04 %) , $V (-0,31 %) , $MC (+1,9 %) , $SALM (+0,15 %) ) but I'm also not too keen to pocket the profits. Are there any stocks in my portfolio that you would view critically for the next few years and would be worth considering selling? Recession and all that...

Priority is on growth, which is reasonably safe, so only a few small caps - but a few bets have to be in there :) ($AIDX (+1,66 %) , $NRX (+0,67 %) , $ITM (+1 %) , $F3C (+2,4 %) , $MITK (+1,65 %) ). But with rather small amounts, probably too small or what do you say?

At the same time, I would also like to claim a €900 allowance via dividends ( $BATS (-0,67 %) , $ENB (-1,5 %) , $BNPQY , $STLAM (+1,77 %) , $ENGI (-0,76 %) , $RIO (-0,21 %) ) and secure a trade or two.

Recently I have been investing 240€/m in the $XDWD (-0,6 %) and between 200 - 500€/m in individual shares (depending on what is left). Actually, I want to increase the existing shares properly now, but somehow there are always nice entry options in solid companies like $0L2T (+3,23 %) , $ZTS (-1,1 %) , $ADM (-0,46 %) , $PANW (-0,33 %) , $ENR (+2,18 %) . Help what to do? :D

And then there's also crypto $BTC (-3,13 %)

$NEAR (-1,42 %)

$ADA (-2,54 %)

And Japan, they're doing well too $4063 (+1,78 %) , $6501 (-2,54 %) , $8001 (-0,41 %)

Looking forward to your feedback and advice!

New addition to the portfolio

I bought a new position in my portfolio today shortly after the start of trading in the USA: Zoetis $ZTS (-1,1 %).

Zoetis is a manufacturer of medicines and vaccines for pets and livestock. The company is interesting for me for the following reasons:

The company operates in both the pet sector and the livestock sector. In the pet sector, there is a long-lasting trend towards regular and better medical care (regular vaccinations, cures, ...). The livestock sector is also benefiting from a sustained demand for better and more efficient medical care.

Overall, the market for veterinary medicine is expected to grow by 7-8% per year. Zoetis is already the market leader in many areas and has always managed to grow faster than the market as a whole.

Risks

This is a sector bet based on the hypothesis that there is a trend towards more and better medical care for pets and livestock. This may of course turn out to be wrong, especially in times of recession, the cost of medical care for pets may not rise (or even fall) as much as hoped.

Another risk is the current valuation. Zoetis is currently valued at a free cash flow yield of around 2.5%. A lot of growth is already priced in.

Summary

The risk/reward is attractive for me and I have opened an initial position. I will give the share time to assess the direction in which the company is developing. The price is certainly not a bargain at the moment, but for me it is still a price level at which I can open an initial position.

Stock analysis/Share presentation ⬇️

Today we are talking about the company Zoetis: $ZTS (-1,1 %)

What is and does Zoetis anyway 🤔

Zoetis is a leading global animal health company specializing in the development, manufacturing and marketing of medicines and vaccines for animals. Zoetis offers a wide range of products for farm animal and companion animal health, including antibiotics, vaccines, analgesics and other medicines. Zoetis is committed to improving the health of animals around the world and helping pet owners keep their animals healthy.

When was Zoetis founded?

Zoetis was founded in 2013 when it was spun off from Pfizer to become an independent animal health company. Zoetis is headquartered in Parsippany, New Jersey, USA.

How many employees does the company have: 🙋🏽♂️🙋🏽♂️

Currently, Zoetis has a total of over 13,800 employees.

P/E RATIO:

Zoetis has a current P/E ratio of just under 37.20, which is not exactly the cheapest valuation.

Market capitalization: 💰

Currently, Zoetis has a market capitalization of around 71 billion euros.

Dividend yield: 💰

The company pays its shareholders a small but fine dividend of currently over 0.9%. This distribution is made on a quarterly basis. Zoetis shareholders receive their dividends in March, June, September and December.

Strengths of the share: 📈

Zoetis is an animal health company that has had strong performance in recent years. Some of Zoetis' strengths include:

Weaknesses of the share: 📉

Some of Zoetis' weaknesses include:

A little more about the business model: ⬇️

Zoetis generates its revenues through the development, manufacture and marketing of animal health products and diagnostic devices. Its range of medicines can be broken down into anti-infectives, vaccines, anti-parasitics and medicated feed additives. Although Zoetis is active in over 120 countries worldwide, more than half of all sales are generated in the USA. China and Brazil follow at a considerable distance, each accounting for 4% of sales. In Germany, the company generates 2% of its sales. The range of products varies by region to meet the needs of customers.

The company reports in two segments.

Pets. This segment is mainly concerned with pets and farm animals such as dogs, cats and horses. As described earlier, the health of our four-legged friends is as important to us as our own. For this reason, we go to the vet at least once a year for a routine check-up. We also regularly have our pets vaccinated to protect them from infectious diseases. Zoetis offers here different vaccines adapted to each animal. Another area of application for Zoetis products is parasite control. This mainly involves fleas, ticks and worms. In addition to these common animal health products, Zoetis also has painkillers and sedatives, as well as oncology and antiemetic products. The companion animal segment accounts for about 60% of Zoetis' total sales.

Farm Animals. This segment focuses on animals used in the food industry. In this segment, the company offers products to prevent or treat conditions that adversely affect livestock. In particular, the aim is to prevent disease outbreaks from spreading to livestock. Mass livestock farming in particular provides good conditions for viruses and other pathogens to infect the entire livestock house in a short time. Veterinary medicines and vaccines are designed to prevent this. The company specializes in cattle and dairy cattle, pigs, poultry, sheep and fish. The livestock sector accounts for around 39% of the company's sales.

In addition to animal health products, the company also offers diagnostic systems for livestock and companion animals. Diagnostic instruments and tests enable veterinarians, livestock producers and pet owners to monitor animal health and detect diseases in animals within minutes. The diagnostics portfolio consists of more than 90 instruments and tests. Currently, the diagnostics segment accounts for only 5% of total sales. However, management also sees great potential in this area through digitalization.

Zoetis is located in a crisis-proof industry and is even the market leader in this sector. Since animal welfare must be ensured at all times, sales are not subject to cyclicality and ensure reliable and stable revenues. Because even in crises, we want our pets to be well. Likewise, meat continues to be consumed even in a crisis. The growing world population and increasing prosperity will continue to ensure growth in the animal health industry in the future.

Your opinion: 🤔🧐

Now I would like to hear your opinion on this stock in the comments.

What do you think of Zoetis and did you already know this company?

Do you guys maybe already have this stock in your portfolio?

Feel free to let me know in the comments.

Of course, this is not an investment advice but just my own opinion that I would like to share with you.

Investment philosophy, "diversification" and dividends

Hi all, as this is my first slightly larger post I would generally appreciate some constructive feedback.

First something About Me

I'll be 22 in a month and I've been active in the stock market for about 2 years now. After a lot of back and forth, I can almost say that I have tried every strategy - but I never really felt comfortable. One learns from mistakes, and I have made many of them.

But what I have also done is to spend countless hours, days and weeks with books, videos, shareholder letters and internet research. I was particularly fascinated by the investment approaches of Terry Smith and the way of Joseph Carlson on Youtube.

My goal quickly became clear, I don't want to have thousands of companies in my portfolio that I don't know, understand or fully support. So an ETF focus was off the table.

Thereupon I built my own investment philosophy, which I would like to present to you in the following.

If you want to know more about me and my goals, there might be another article with a portfolio presentation soon :-)

First I would like to explain to you why I do not believe in diversification hold:

A quote from Warren Buffet is well known: "Diversification is protection against ignorance. It makes little sense if you know what you are doing."

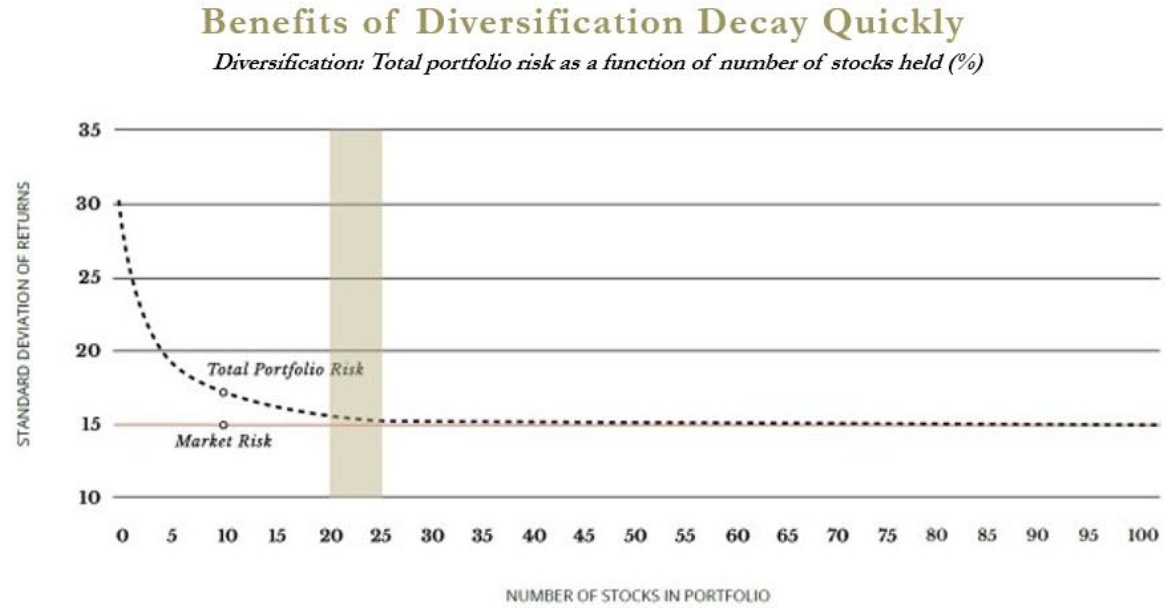

However, a quote from one of the world's best investors alone is unlikely to convince everyone. Studies also support Buffet's view. The advantages of diversification decrease very fast and the gap between market risk and total portfolio becomes minimal from a portfolio size of 20-25 companies - 25 companies give you all the advantages of diversification, more positions only worsen your performance and overview. (Figure 1)

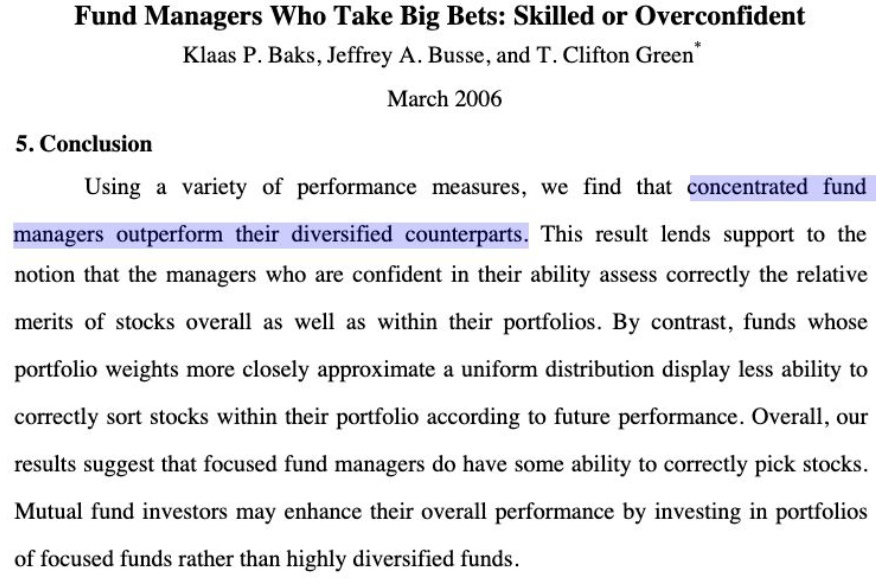

Because concentration delivers better performance. Fund managers who concentrate their knowledge in a few companies deliver better results than more diversified managers. (Figure 2)

Investment philosophy

I want to outperform the market, so I look for the best companies. What makes good companies?

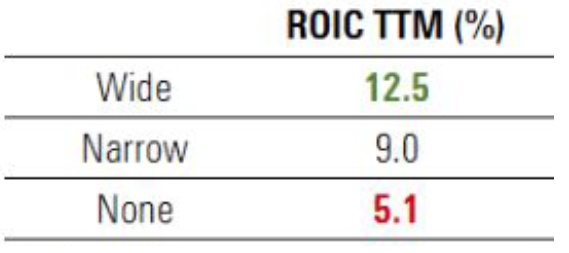

Companies with competitive advantages (moats) outperform the market (Figure 3), and they do so because they have high returns on capital. My first metric for evaluating quality of a company and with a high value in my company analysis is ROIC (Return on Capital Invested). I look for companies with at least 10% ROIC. (Figure 4) Furthermore I want high ROCE (Return on capital employed) and high ROA (Return on Assets) figures.

This directly eliminates some companies and also whole sectors, namely exactly those in which it is not worth to invest anyway. Why is this so?

There are sectors that historically outperform the market (Software, Consumer, Healthcare) - on which my focus is -, and sectors that consistently underperform and are not considered in my investment approach (Banking, Energy, Insurance, Mining, Utilities, Airlines) - just compare the sectors with the main index ;-)

Consumer goods, healthcare and software companies perform better because they generate sustained profits, so they remain profitable even during economic downturns. This allows for consistently high returns on capital.

Next, a look at the margin here I would like to see high Gross Margins >60%, which are also a good indicator of a competitive advantage, and a high Profit Margin, which is an indicator of the efficiency of a company's value creation. However, the most important margin for assessing profitability is the FCF margin.

A company's focus should be maximally on Free Cash Flow, we should invest in companies that are as profitable as possible. In the long run, the share price follows the Fcf/Share.

Beyond that I don't want any debt, any company with Debt/EBITDA > 3 flies right out, preferably anything less than 2.

In terms of growth, I look for stable and good EPS and revenue growth, but FCF growth has the highest priority.

The higher the better, the more important the key performance indicators are.

My minimum benchmarks for the most important metrics:

(Not all of my companies always meet every metric, but I have built my own score where a minimum score must be met and by score I set the "Conviction" to a company).

Buy & Hold and long-term investing outperforms

As long as a company continues to reinvest its capital at high returns there is no reason to sell. (Figure 5)

What about dividends?

Some of my companies pay a dividend, others don't - I don't put much emphasis on dividends, and will definitely not put bad companies in my portfolio just to get a payout in a given month ;) Dividends should be minimized if capital can be reinvested at high rates of return. At my young age and with a long term investment horizon the focus should be on yield, in old age I will also shift to dividends ;)

The most important thing to conclude: Invest in profitable companies that you UNDERSTAND

A few final tips:

My current investable universe:

$ADBE (-0,02 %)

$NVO (-1,68 %)

$CUV (-2 %)

$CDNS (-1,4 %)

$ASML (+0,53 %)

$VRTX (+0,3 %)

$V (-0,31 %)

$MA (-0,36 %)

$MSFT (-1,04 %)

$QLYS (+1,68 %)

$MKTX (-0,42 %)

$KLAC (-1,68 %)

$GOOGL (+0,56 %)

$REG1V (-0,44 %)

$TNE (-1,3 %)

$ENX (+0,76 %)

$EW (+0,22 %)

$VRSN (-0,32 %)

$FICO (-1,06 %)

$FTNT (+0,53 %)

$NEM (-1,08 %)

$MONC (+1,24 %)

$CSU (+0,56 %)

$6861 (-0,24 %)

$ENGH (-1,49 %)

$MC (+1,9 %)

$AAPL (-0,66 %)

$6857 (-3,7 %)

$7741 (+1,12 %)

$PAYX (-0,97 %)

$MTD (+0,02 %)

$TXN (+0,94 %)

$OR (+0,88 %)

$ZTS (-1,1 %) (Companies I watch, in my portfolio I have only 8 of them).

That's it from me for now. Please leave me some feedback and share the post if you like it :-)

What would you like to hear from me next? More about free cash flow? Portfolio presentation? Company presentation? My slightly different valuation approach, far away from P/E?

Some of the illustrations are from a slightly smaller fund ("Long Equity Investing" on Twitter - can only recommend you) or from Terry Smith's Shareholder Letter.

No investment advice

+ 1

Meilleurs créateurs cette semaine