Hello dear Getquin Community,

This year's IAA Mobility in Munich showed that the automotive industry is on the verge of a turning point. With over 30 percent more exhibitors than in 2023 and numerous premieres from Audi, $BMW (+0,67 %) BMW, $MBG (+0,47 %) Mercedes, $VOW3 (+0,96 %) VW, Opel and Chinese challengers such as BYD and $1211 (-0,58 %) BYD and $9868 (+0,65 %) XPeng, it became clear that electromobility has now become the standard. However, behind these new platforms and concepts lies an even bigger topic, namely autonomous driving and the robotaxis of the future.

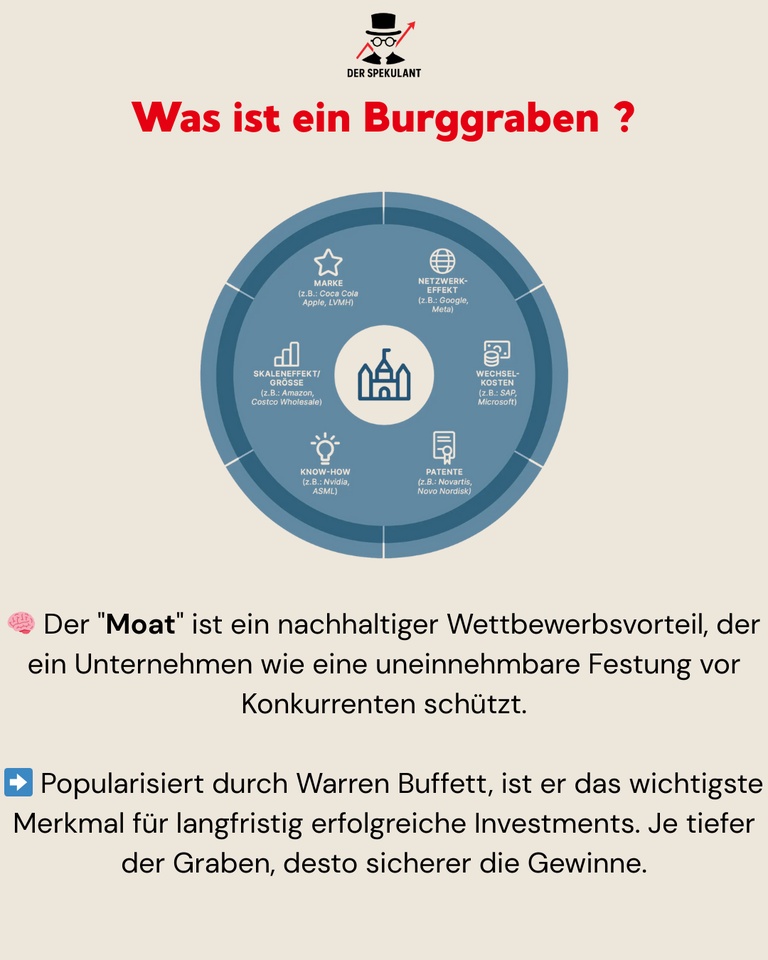

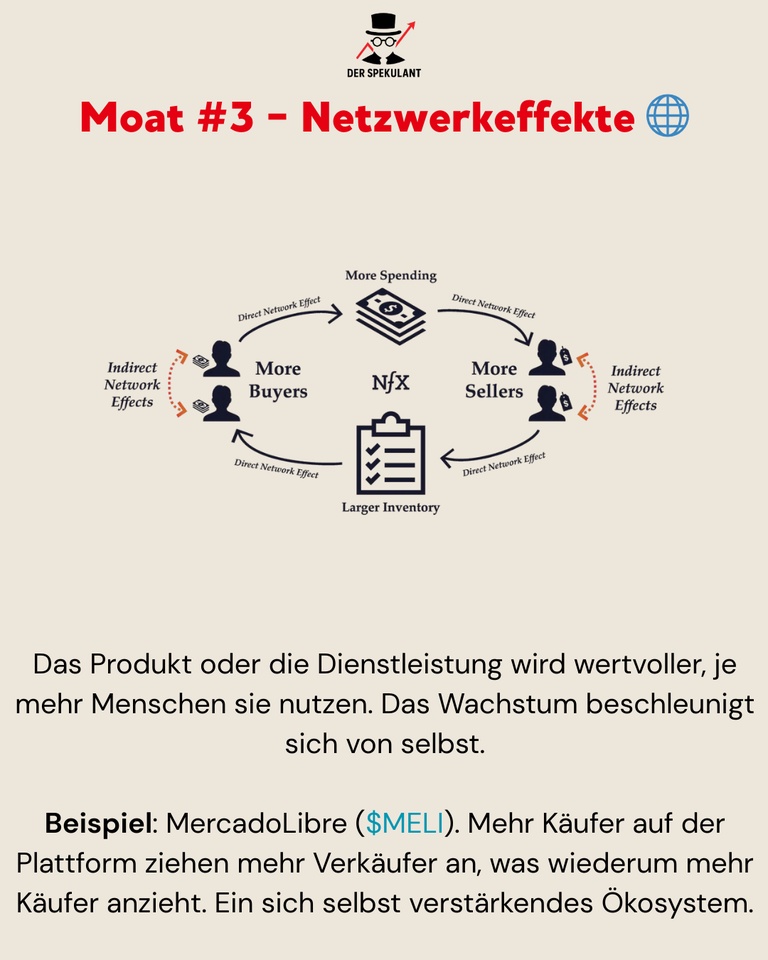

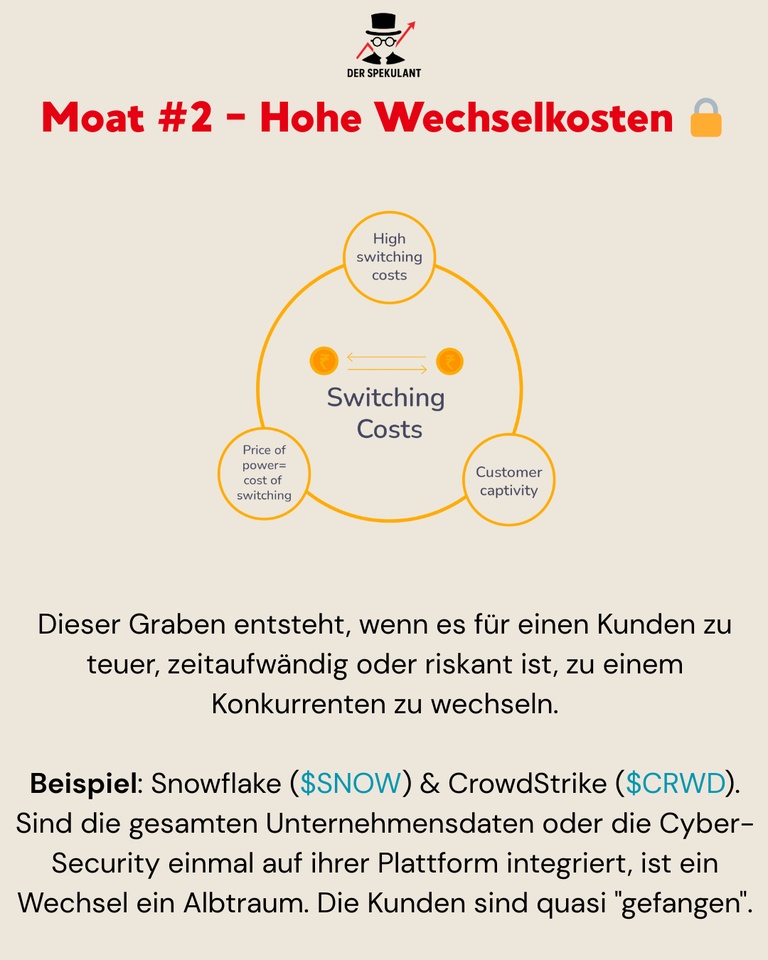

In order to present this field in a clear and transparent way for investors, I have broken down the entire value chain into individual sectors. These include automotive and suppliers, semiconductors and technology, communication and infrastructure, software and algorithms, logistics and transportation, insurance and finance, energy and infrastructure, battery and propulsion, maps and mapping, and safety and cybersecurity. Within each sector, I have analyzed the big players, the hidden champions and the blade manufacturers and highlighted my favorites in each case with a brief explanation. @Multibagger 😎

My aim was to develop as comprehensive a picture as possible that shows where the opportunities lie in this new industry and how investors can position themselves at an early stage. Perhaps the IAA 2025 was not just a car show, but actually the starting signal for the next big investment ecosystem around robotaxis and autonomous driving. If I have overlooked any important aspects or if a categorization was not quite precise, I look forward to your comments @BamBamInvest

@Epi

😎 and exciting additions @All-in-or-nothing 😎 Together we can understand this topic even better and learn from each other. @Tenbagger2024 😎

Feel free to leave a 👍. I wish you every success with your investments 🚀

🚘 Automotive & suppliers

Big player:

$TSLA (-3,07 %) Tesla - pioneer in autopilot/FSD, vertical integration, huge database

$MBG (+0,47 %) Mercedes-Benz Group - EQS/EQE with Level 3 approval in Germany, strong regulatory expertise

$BMW (+0,67 %) BMW - New class platform, e-models with prepared sensor technology & level 3 approaches

$VOW (+1,98 %) VW Volkswagen - Cariad software unit, massive push towards ADAS/AV

$7203 (+0,82 %) Toyota (Japan) - largest OEM, cooperation with Pony.ai and Denso

$GOOGL (+1,8 %) Alphabet Waymo (private/Alphabet $GOOGL) - robotaxi pioneer in the USA

$9888 (+1,67 %) Baidu Apollo (9888.HK) - Robotaxi & Full-Stack AV in China

$Pony.ai (private, China) - Robotaxi & partnerships with Toyota

👉 Favorite: Alphabet Waymo ($GOOGL (+1,8 %))

Moat through years of data collection in real operation, deep AI integration, financially secured by Alphabet. Compounder potential, as Waymo can scale as a platform.

Hidden champions:

$APTV (+0,68 %) Aptiv - supplier for ADAS, sensor fusion, E/E architectures

$MG (+0,23 %) Magna International - produces complete vehicle systems including autonomous components

$ZF Friedrichshafen (private) - German giant in steering and braking systems for AVs

Veoneer (private, formerly listed) - safety software, vision, sensor technology

$SHA0 (+1,12 %) Schaeffler AG (DE, Germany, Xetra) - global supplier of drive, chassis and intelligent steering systems. Important for e-mobility and redundancy solutions in autonomous driving.

👉 Favorite: Aptiv ($APTV (+0,68 %)

)

High barriers to entry through system integration, broad customer base (OEM-agnostic), strong cash flow and close partner of major car manufacturers.

Blade manufacturer:

$NVDA (+2,31 %) Nvidia - Drive Orin / Thor chips for OEMs, standard in the AV sector

$QCOM (-0,49 %) Qualcomm - Snapdragon Ride platform for AVs

$INTC (-7,3 %) Intel Mobileye - EyeQ chips, one of the market leaders in ADAS

$LAZR (+30,8 %) Luminar Technologies - Lidar, partnerships with Volvo, Mercedes, SAIC

$OUST Ouster, Inc. - Lidar solutions

$INVZ Innoviz (INVZ) - Lidar sensor technology, cooperation with VW & BMW

👉 Favorite: Nvidia ($NVDA (+2,31 %)

)

Dominance in high-performance AI chips, ecosystem with software (CUDA, DriveSim), network effects through partnerships with almost all OEMs. Classic compounder, enormous moat due to technology and developer lock-in.

Takeaway:

In the automotive & supplier sector, it's not just who sells the most cars, but who has mastered the best technology stack for autonomy. OEMs work closely with specialized suppliers and blade manufacturers. Investors should focus less on unit numbers and more on data basis, software expertise and partnerships. The real levers often lie with suppliers and technology enablers, not just the traditional car brands.

💻 Semiconductors & technology

Big players:

$NVDA (+2,31 %) Nvidia - GPUs & AV chips (Drive Orin, Drive Thor), software ecosystem

$QCOM (-0,49 %) Qualcomm - Snapdragon Ride platform, automotive pipeline >30 billion USD

$INTC (-7,3 %) Intel / Mobileye - EyeQ chips, ADAS market leader

$AMD (+6,32 %) AMD - GPU/CPU, entry into automotive AI compute

👉 Favorite: Nvidia ($NVDA (+2,31 %)

) Unique position: Technological moat through CUDA ecosystem, enabler of almost all AV developments, quasi-monopoly in high-end compute. Classic compounder with long-term growth leverage.

Hidden champions:

$LAZR (+30,8 %) Luminar Technologies - Lidar supplier, partnerships (Volvo, Mercedes, SAIC)

$INVZ Innoviz Tech. - Lidar, BMW & VW as customers

$KOTMY Koito Manufacturing - world market leader in automotive lighting, entry into lidar through Cepton integration, important role as supplier for OEMs

$AMBA (+2,55 %) Ambarella (AMBA) - camera chips & vision processors for AV

$STMPA (-2,82 %) STMicroelectronics (France/Italy, Euronext) - automotive microcontrollers, sensors, power electronics. European counterpart to Infineon.

$AIXA (+1,18 %) Aixtron (Germany, Xetra) - supplies manufacturing equipment for SiC and GaN semiconductors, indispensable for power electronics in EV/AV.

$ELG (+2,7 %) Elmos Semiconductor (Germany, Xetra) - niche player for mixed-signal semiconductors in automotive, e.g. for radar and driver assistance.

👉 Favorite: Luminar ($LAZR (+30,8 %)

) Clear technical USP, strategic OEM deals in series production, high barriers to entry in lidar technology. Scalable compounder in a niche market.

Blade manufacturer:

$TSM (+1,4 %) Taiwan Semiconductor - production of all relevant automotive chips

$ASML (-0,02 %) ASML Holding - Lithography monopolist, without ASML no AI/AV chips

$EQIX (+0,56 %) Equinix - data center colocation for AI training & simulations

$DLR (+2,14 %) Digital Realty - cloud and data infrastructure

$AMZN (+1,56 %) Amazon AWS - Cloud resources for AI training, simulation & OTA updates

👉 Favorite: ASML ($ASML (-0,02 %)

) Monopoly on EUV lithography, no advanced chips for autonomous driving without ASML. Moat through technology and patents, classic compounder.

Takeaway:

Semiconductors & technology are the foundation of autonomous driving. While Nvidia plays the central role with computing power, lidar specialists such as Luminar ensure perception. The real shovelware winner, however, is ASML, without whose machines there would be no AV chips. Investors will find the deepest technological moats in the entire value chain here.

📡 Communication & infrastructure

Big players:

$ERIC B (-0,5 %) Ericsson - 5G/6G networks, vehicle-to-everything (V2X) applications, global player

$NOK (+1,89 %) Nokia - 5G/Edge solutions for automotive & smart cities

$QCOM (-0,49 %) Qualcomm - Snapdragon Digital Chassis, V2X chipsets, automotive pipeline

Huawei (private, China) - strong player in 5G/AV communication, partnerships in Asia

👉 Favorite: Qualcomm ($QCOM (-0,49 %)

) Wide moat through IP in mobile communications, at the same time deep automotive integration via Snapdragon Ride & Digital Chassis. Compounder, as economies of scale in chips + licenses worldwide.

Hidden champions:

$Cohda Wireless (private, Australia) - pioneer for V2X communication, software solutions for OEMs

$Autotalks (private, Israel, acquisition by Qualcomm planned) - leader in dedicated V2X chips

Commsignia (private, Hungary) - V2X middleware & roadside units

👉 Favorite: Autotalks (private, Israel)

Technology leader in dedicated V2X chips, unique IP portfolio. Strong takeover candidate (Qualcomm already active), giving moat + exit potential.

Shovel manufacturer:

$CSCO (+0,2 %) Cisco Systems - network infrastructure for automotive, cloud & edge

$AMT (+0,49 %) American Tower - cell towers & infrastructure, benefits from 5G expansion

$CCI (-0,12 %) Crown Castle - radio tower and fiber optic infrastructure (mainly USA)

$EQIX (+0,56 %) Equinix - data centers, basis for edge computing and OTA updates

$DLR (+2,14 %) Digital Realty - colocation & data center capacity for simulations and AV data

👉 Favorite: Equinix ($EQIX (+0,56 %)

)

Global leader in data center colocation, benefits from the edge computing trend. Strong moat due to network effects & high switching costs. Long-term compounder.

Takeaway:

Communication & infrastructure are the silent cornerstones of autonomous driving. Without low-latency networks, edge data centers and V2X communication, no AV can drive safely. While Qualcomm forms the technological bridge between chip and infrastructure, hidden champions such as Autotalks secure niche leadership. On the blade side, Equinix remains unbeatable, as every OEM & service provider needs computing power at the edge.

🤖 Software, platforms & algorithms

Big Player:

$GOOGL (+1,8 %) Alphabet / Waymo - Robotaxi pioneer, full-stack AV software, years of database

$TSLA (-3,07 %) Tesla - FSD, Dojo supercomputer, vertical integration incl. fleet

$9888 (+1,67 %) Baidu Apollo (HK) - largest robotaxi network in China, full-stack solution

$UBER (-0,67 %) Uber - AV platform in partnership (e.g. with Momenta), scaling via existing user base

👉 Favorite: Alphabet / Waymo ($GOOGL (+1,8 %)

)

Unbeatable moat due to millions of real driving kilometers + simulations, strong financial base via Alphabet, focus on platform scaling (robotaxi, licensing model). Compounder with global expansion potential.

Hidden champions:

$Momenta (private, China) - L4 software for OEMs, partner of Mercedes, Toyota

$AUR Aurora Innovation - software + sensor technology for truck autonomy, partner PACCAR, Volvo

$Argo AI (private, USA) - formerly Ford/VW, now partly continued through partner projects

$Oxbotica (private, UK) - modular AV software, focus on industrial & logistics applications

👉 Favorite: Aurora Innovation ($AUR

)

Clear focus on trucking (biggest lever in the AV market), long-term OEM partnerships, strong moat due to specialization in long-haul autonomy. Still young, but strong compounder potential.

Shovel manufacturer:

$PLTR (+2,29 %) Palantir - data management, simulation & AI analysis for AV training

$SNOW (+2,02 %) Snowflake - Cloud data platform, relevant for AV data streams

$MSFT (+0,63 %) Microsoft Azure - cloud & simulation platform for OEMs

$AMZN (+1,56 %) AWS - largest provider for AI training & simulations in the AV sector

$ADBE (-0,07 %) Adobe - Simulation & Digital Twin Tools (via partnerships)

👉 Favorite: Palantir ($PLTR (+2,29 %)

)

Deep integration in data pipelines, modular platform for simulation & decision logic. Moat due to lock-in effects with major customers, strong compounder with AI scaling.

Takeaway:

Software and algorithms are the real key to autonomous driving. Vehicles are becoming "data centers on wheels" and only the companies with data, simulation and AI stacks can dominate the market in the long term. Waymo provides the scalable robotaxi ecosystem, Aurora scores with its trucking focus, and Palantir ensures that data streams remain manageable. This is where the biggest margins are generated, not in the sale of hardware.

🚚 Logistics & transportation

Big player:

$AUR Aurora Innovation - focus on autonomous trucks, partnerships with Volvo & PACCAR

$TuSimple (private, USA) - pioneer for autonomous trucks, strong in the USA and China, currently undergoing restructuring

$AMZN (+1,56 %) Amazon / Zoox - Robotaxi & autonomous delivery services, integration into e-commerce and Prime

$FDX (+0,92 %) FedEx - test programs for autonomous delivery (cooperations with Aurora, Nuro, among others)

$DHL (-0,13 %) Deutsche Post DHL - pilot projects with autonomous delivery vehicles & drones

👉 Favorite: Amazon / Zoox ($AMZN (+1,56 %)

)

Moat through e-commerce ecosystem, integration of AV in the last mile, strong financial power and scalability. Compounder due to synergies between logistics and technology.

Hidden champions:

$Nuro (private, USA) - autonomous delivery vehicles specifically for the last mile

$Einride (private, Sweden) - electric autonomous trucks, focus on freight & sustainability

$Gatik (private, Canada/USA) - AV for medium distances (B2B supply chains, e.g. Walmart)

$Starship Technologies (private, Estonia/USA) - autonomous delivery robots for urban logistics

👉 Favorite: Gatik (private, Canada/USA)

Clear business model: "middle-mile" logistics, profitable niche market with predictable routes. Moat through early commercial contracts (Walmart). Compounder potential through scaling in the B2B sector.

Shovel manufacturer:

$CAT (+0,5 %) Caterpillar - autonomous technologies for construction machinery & mining, know-how transferable

$DE (+0,55 %) Deere & Co - autonomous agricultural machinery, similar technology stacks as for trucks

$ISRG (-1,06 %) Intuitive Surgical - example of high-end automation (here as a cross-reference for AV tech transfer)

$UPS (+0,01 %) United Parcel Service - logistics infrastructure, partner for AV integration

$R (+0,36 %) Ryder System - fleet management, leasing and AV test integration

👉 Favorite: Deere & Co ($DE (+0,55 %)

)

Autonomy already in use (precision farming), moat through data & technology in the agricultural sector. Compounder quality, as know-how in navigation & autonomy is transferable to transportation/logistics.

Takeaway:

Logistics is one of the first markets where autonomous driving brings real profitability. Trucks and delivery services benefit from 24/7 operation without drivers, while the last mile (Nuro, Gatik) opens up new business models. Amazon is the most powerful player through vertical integration, while hidden champions like Gatik occupy targeted profitable niche markets. Shovel manufacturers such as Deere supply the already proven autonomy stacks.

🏦 Insurance & finance

Major players:

$ALV (+0,33 %) Allianz - the world's largest insurer, involved in AV pilot projects at an early stage

$MUV2 (+0,31 %) Munich Re - reinsurance, develops models for AV risk transfer

$CS (+0,17 %) Axa - active in AV insurance testing & research

$BRK.B (+0,27 %) Berkshire Hathaway - large presence in the US motor insurance market via Geico

👉 Favorite: Munich Re ($MUV2 (+0,31 %)

)

Moat through global reinsurance strength, pioneer in new risk models for AVs. Compounder characteristics through diversification and ability to insure new markets (cyber, AV, climate) at an early stage.

Hidden champions:

$LMND (+1,4 %) Lemonade - digital insurance, AI-driven, quickly adaptable for AV policies

$Root Insurance (private/USA, formerly listed) - data-driven car insurance, use of driving data

$Next Insurance (private, USA) - platform approach, simple onboarding for new risks

$Wefox (private, Germany) - digital platform for insurance brokerage, flexible for new products

👉 Favorite: Lemonade ($LMND (+1,4 %)

)

Pure digital insurer with AI-driven underwriting. Moat through data and automation approach. Still small, but compounder potential as scalable platform can be used in new markets such as AV policies.

Shovel manufacturer:

$SREN (+0,86 %) Swiss Re - global reinsurer, benefits from increasing AV risk volume

$VRSK Verisk Analytics - data & risk analytics for insurers, AV risk models

$GWRE (-0,85 %) Guidewire Software - software solutions for insurance companies, customization for AV policies

$FICO (+3,16 %) Fair Isaac - Analytics & risk modeling, increasingly relevant for complex AV data

👉 Favorite: Verisk Analytics ($VRSK

)

Moat through exclusive data pools & analytics. Enabler for almost all insurers. Compounder character, as growing demand for data & models in new markets such as AVs.

Takeaway:

Autonomous driving shifts liability from the driver to the manufacturer or software provider. Insurers need to develop new products, reinsurers and data providers are becoming more important. Munich Re is protecting the industry, Lemonade is testing digital models and Verisk is providing the data intelligence without which no AV insurance can function. Investors will find silent but indispensable winners of the upheaval here.

🛡️ Security & Cybersecurity

Big players:

$PANW (+1,3 %) Palo Alto Networks - market leader in network security, focus on cloud & IoT, relevant for connected vehicles

$CRWD (+0,86 %) CrowdStrike ($CRWD) - endpoint security, strong platform for AV endpoints and fleets

$CHKP (-0,87 %) Check Point ($CHKP) - Security appliances & firewalls, focus on embedded & IoT

$CSCO (+0,2 %) Cisco Systems ($CSCO) - Network security + automotive infrastructure

👉 Favorite: Palo Alto Networks ($PANW (+1,3 %)

)

moat due to the width of the platform, which extends from the data center to the vehicle. With the $CYBR (+0,7 %) -integration, PANW has also covered the topic of identity security. Compounder properties through continuous expansion, high customer loyalty and a strong M&A strategy.

Hidden champions:

$CON (+1,23 %) Argus Cyber Security (private, subsidiary of Continental) - specialized in automotive cybersecurity

$Upstream Security (private, Israel) - cloud-based cyber platform specifically for connected vehicles

Karamba Security (private, Israel) - embedded security for control units (ECUs)

$4704 (+0,07 %) VicOne (subsidiary of Trend Micro) - AV-specific threat analysis

👉 Favorite: Argus Cyber Security (private, part of $CON (+1,23 %)

Continental)

Pioneer in the automotive segment, deep integration in OEMs. Moat through early partnerships and specialization in vehicle architectures.

Shovel manufacturer:

$AKAM (-0,14 %) Akamai - Content Delivery & Edge Security, relevant for OTA updates

$FTNT (+0,84 %) Fortinet - Network & IoT security, broad base

$ZS (+1,56 %) Zscaler - cloud-native security for data traffic between AV & cloud

$NET (+0,22 %) Cloudflare - infrastructure protection, DDoS protection for fleets & updates

$BB (+3,78 %) BlackBerry QNX - Operating system & security framework for automotive

👉 Favorite: BlackBerry ($BB (+3,78 %)

)

Moat by QNX, which is already running in millions of vehicles. Strong lock-in with OEMs. Compounder potential if QNX continues to scale as a security operating system for AV architectures.

Takeaway:

Cybersecurity is the nervous system of autonomous driving. Without secure communication, OTA updates and fleet protection, AV is inconceivable. Palo Alto Networks provides the necessary breadth and depth, Argus secures the vehicles themselves, and BlackBerry QNX provides the foundation in the control units. Investors are relying on the invisible gatekeepers of tomorrow's mobility.

⚡ Energy & infrastructure

Big player:

$EBK (+0,3 %) EnBW - operator of charging infrastructure in Germany, expansion of fast-charging parks

$SHEL (-0,11 %) Shell - massive entry into e-mobility & charging infrastructure, partnerships with OEMs

$BP (-1,33 %) BP - charging and energy infrastructure via bp pulse, global rollout

$TSLA (-3,07 %) Tesla ($TSLA) - Supercharger network as AV backbone, potential licensing model

👉 Favorite: Tesla ($TSLA (-3,07 %)

)

Moat due to world's largest fast charging network with high availability & own software integration. Compounder, as Supercharger can grow as a service independently of the OEM.

Hidden champions:

$Ionity (private, joint venture of BMW, Mercedes, Ford, VW, Hyundai) - Europe's premium charging network 👉 Access via OEMs such as BMW or Mercedes

$ALLG Allego - listed charging infrastructure operator, focus on Europe

$FAST (+0,11 %) Fastned (FAST.AS) - fast charging network in Europe, rapidly growing

$DCFC Tritium DCFC - manufacturer of fast charging stations, globally active

👉 Favorite: Fastned ($FAST (+0,11 %)

)

Clear business model as a pure fast-charging operator, strong moat through premium locations & brand perception. Compounder potential via expansion in Europe.

Shovel manufacturer:

$ABBN (+0,44 %) ABB - leader in charging hardware & power grid infrastructure

$ENR (+4,35 %) Siemens Energy - grid infrastructure & charging hardware, important supplier for energy transition + AV

$SU (+1,65 %) Schneider Electric - power distribution, smart grids for charging infrastructure

$6594 (+3,38 %) Nidec - motors & drives for e-mobility

$ETN (+0,44 %) Eaton - Energy management & charging infrastructure components

👉 Favorite: ABB ($ABBN (+0,44 %)

)

Broadly positioned from fast charging hardware to grid technology. Moat due to market leadership & long-standing customer base. Compounder, as electromobility + AV will bring growth for decades.

Takeaway:

Autonomous vehicles don't just need software, they need a reliable charging and energy base. Tesla is securing a massive advantage with its Supercharger network, while hidden champions such as Fastned are setting the pace in Europe. On the shovel side, ABB dominates with its global infrastructure expertise. Investors should not underestimate this sector, as no AV will drive without energy.

🏙️ Mobility services & platforms

Big players:

$UBER (-0,67 %) Uber Technologies - ride-hailing, partnerships with AV start-ups (Momenta), robotaxi plans in Munich

$LYFT (-0,17 %) Lyft - ride-hailing, own AV programs, cooperations with Aptiv & Motional

$DIDIY (+0,93 %) Didi Global - largest ride-hailing network in China, AV research on Didi Autonomous Driving

$9888 (+1,67 %) Baidu Apollo - robotaxi operator in China, leading with Apollo Go

$AMZN (+1,56 %) Amazon / Zoox - fully autonomous robotaxi, integration into Amazon ecosystem

👉 Favorite: Baidu Apollo ($9888 (+1,67 %)

HK, China, HKEX)

Moat through network effects in the world's largest mobility market. Apollo Go has already completed hundreds of thousands of robotaxi journeys. Compounder potential as China aggressively promotes AV.

Hidden champions:

$Momenta (private, China) - L4 autonomy software, partnerships with Mercedes & Toyota, based in Suzhou, China

👉 Access indirectly via investors such as $7203 (+0,82 %) Toyota or Mercedes $MBG (+0,47 %)

$Motional (joint venture Hyundai & Aptiv, private, USA/South Korea) - Robotaxi tests in the USA

👉 Access via $Hyundai or $APTV (+0,68 %) Aptiv

$WeRide (private, China) - Robotaxi & AV bus solutions, based in Guangzhou, China

👉 Investors: Renault-Nissan-Mitsubishi Alliance

$Cruise (private, USA) - GM subsidiary for robotaxis, based in San Francisco

👉 Access via $GM (+3,46 %) General Motors

👉 Favorite: Motional (private, USA/South Korea)

Strong moat through OEM partnerships (Hyundai + Aptiv). Realistic scaling through series integration, compounder potential via global fleet integration.

Shovel manufacturer:

$HTZ (+0,22 %) Hertz Global - fleet management, integration of AVs in rental fleets

$SIX2 (+1,8 %) Sixt SE - Car sharing & fleet leasing, focus on Europe

$R (+0,36 %) Ryder System ($R, USA, NYSE) - fleet services & leasing, AV test integration

$GRAB (+1,94 %) Grab Holdings ($GRAB, Singapore, Nasdaq) - Southeast Asian ride-hailing market leader, entry into AV services

$Ola Cabs (private, India) - AV pilot projects in India

👉 Favorite: Sixt SE ($SIX2 (+1,8 %)

.DE, Germany, Xetra)

Moat due to premium positioning in Europe, flexible business model (rental, leasing, car sharing). Compounder, as Sixt invests early in fleet integration of AVs and benefits from growing Mobility-as-a-Service market.

Takeaway:

Mobility services are the interface to the end customer. This is where it will be decided whether AVs remain just technology or break through to the mass market. Baidu dominates in China, Motional scores with strong partners in the West, and Sixt provides the platform to bring scalable AVs into everyday life in Europe. Investors who get in early will secure access to the future platform monopolies of mobility.

🔋 Battery & drive

Big player:

$300750 CATL - world market leader for battery cells, supplies almost all major OEMs

$373220 LG Energy Solution - global player, supplier for Tesla, Hyundai, GM

$6752 (+1,71 %) Panasonic Holdings - long-standing partner of Tesla, strong in energy storage

$1211 (-0,58 %) BYD - integrates battery production and vehicles, pioneer in blade batteries

👉 Favorite: CATL ($300750

SZ, China, Shenzhen)

Moat due to technological leadership and economies of scale, supplies almost all global OEMs. Classic compounder, as batteries are at the heart of every AV fleet.

Hidden champions:

$Northvolt (private, Sweden) - European battery startup, sustainable production, supplies VW and BMW 👉 Access indirectly via VW ($VOW3 (+0,96 %) DE, Germany, Xetra) or BMW ($BMW (+0,67 %) DE, Germany, Xetra)

$SLDP Solid Power - specialist for solid-state batteries, partnerships with Ford and BMW

$ProLogium (private, Taiwan) - solid-state batteries, pilot projects with Mercedes👉 Access indirectly via Mercedes-Benz Group ($MBG (+0,47 %) DE, Germany, Xetra)

$QS QuantumScape ($QS, USA, NYSE) - solid-state batteries, strong focus on future technology

$MOD (+5,77 %) Modine Manufacturing (USA, NYSE) - Thermal management for batteries, e-motors and power electronics. Critical for range and safety.

$KULR (+2,82 %) Technology (USA, NYSE) - specializes in battery cooling, energy storage and recycling. Still small, but focus on safety makes it interesting in the AV context.

$ZIL2 (-1,56 %) ElringKlinger (DE, Germany, Xetra) - supplier of battery packs, housings, seals and fuel cell technology. Supports OEMs in electrification and alternative drive systems.

👉 Favorite: Solid Power ($SLDP

USA, Nasdaq)

Technology leader in solid-state batteries with strong OEM partnerships. Moat through patents and early market entries. Compounder potential through commercialization from 2027+.

Blade manufacturer:

$6594 (+3,38 %) Nidec (JP) - leader in electric motors for EVs and AVs

$IFX (-0,02 %) Infineon Technologies (DE) - semiconductors for power electronics and battery management

$300450 Wuxi Lead Intelligent (China, Shenzhen) - machines for battery production

$UMI (-0,64 %) Umicore (Belgium, Euronext) - cathode materials and recycling

$ALB (+8,64 %) Albemarle (USA, NYSE) - Lithium mining and processing

👉 Favorite: Infineon Technologies ($IFX (-0,02 %)

DE, Germany, Xetra)

Moat due to market leadership in power electronics, deeply integrated in battery and drive systems. Compounder potential due to growing demand for silicon carbide (SiC) chips for EV and AV applications.

Takeaway:

Battery and drive are the foundation of autonomy. Without powerful energy storage, reliable electric motors and robust power electronics, no autonomous vehicle can be operated economically. CATL dominates cell production, Solid Power is a promise of the future in solid state technology, and Infineon supplies the critical power electronics. Investors who neglect this sector are ignoring the heart of autonomous driving.

🗺️ Maps & Mapping

Big players:

$GOOGL (+1,8 %) Alphabet / Waymo (USA, Nasdaq) - HD maps for robotaxis, combined with AI-supported real-time navigation

$9888 (+1,67 %) Baidu Apollo (China, HKEX) - leader in AV mapping in China, integrated into Apollo Go

$HERE Technologies (private, based in NL/DE, owners: Audi, BMW, Mercedes and others) - global provider of HD maps, industry standard for many OEMs

$TOM2 (-1,38 %) TomTom (Netherlands, Euronext) - specialized in HD maps for AVs, partner of Volvo and Bosch

👉 Favorite: HERE Technologies (private, access via OEMs Audi, BMW, Mercedes)

Moat through global map databases, OEM consortium as backing. Compounder potential, as almost all autonomous vehicles rely on HD maps.

Hidden champions:

$002405 Navinfo Co. Ltd, (China, Shenzhen) - market leader for digital maps in China, partnerships with OEMs - unfortunately not tradable in the EU

$Civil Maps (private, USA) - specialized in AI-supported HD mapping for AVs

$DeepMap (private, USA, acquired by $NVDA (+2,31 %) Nvidia) - high-precision mapping, integration with Nvidia Drive

$Mapbox (private, USA) - cloud-based mapping platform, strong in the developer ecosystem

👉 Favorite: NavInfo ($002405

SZ, China, Shenzhen)

Dominance in the Chinese market, regulatory anchoring and partnerships with major OEMs. Moat through market access in China, compounder potential through data growth.

Shovel manufacturer:

$PL Planet Labs (USA, NYSE) - daily earth observation data, basis for dynamic mapping

$HEXA B (+5,61 %) Hexagon AB (Sweden, Nasdaq Stockholm) - measurement technology and geodata solutions

$TRMB (+0,76 %) Trimble (USA, Nasdaq) - positioning and geospatial data for AV and industrial applications

👉 Favorite: Hexagon AB ($HEXA B (+5,61 %)

Sweden, Nasdaq Stockholm)

Moat due to decades of experience in geodata and measurement technology, strong market position in industry and automotive. Compounder potential, as mapping and positioning are indispensable for all AV applications.

Takeaway:

High-precision maps are the nervous system of autonomous driving. Without continuously updated HD maps, vehicles cannot navigate safely. HERE secures a key role through OEM stakes, NavInfo dominates the Chinese market, and Hexagon provides the geospatial bucket technology. Investors should not overlook this sector, as mapping is the invisible foundation on which autonomy works.

Sources: own research, https://www.t-online.de/mobilitaet/aktuelles/id_100901210/iaa-mobility-muenchen-2025-alle-neuheiten-von-audi-bmw-vw-opel.html

Images: https://www.deraktionaer.de/artikel/mobilitaet-oel-energie/robotaxis-das-milliardenrennen-der-autonomen-autos-20381083.html

https://insideevs.de/features/763886/vorschau-iaa-2025-neuheiten-2026/