German shareholders and Poles

Polish companies and shares are rarely discussed in German-speaking countries. The best known are probably Dino Polska

$DNP (-0,09 %) and Zabka $ZAB (-1,39 %) which are both active in the food retail sector. In the small-cap investment community Text S.A. $LVC (+0,46 %) is also known to some. Recently @Daxhund also published a recommendable post about the waste company Mo-BRUK $MBR (+2,04 %) was also published. However, today's post is not about these four shares. This post is the beginning of a kind of series on Polish growth stocks. However, this first post contains some basic information about the Polish economy and a brief introduction to the stocks as a foretaste of what to expect in the coming weeks.

Poland as a business location

The most populous country in Eastern Europe is developing into a very attractive location for companies. This is particularly evident in the rapid development of gross domestic product to date: since 1980, the figure has risen by an average of 7% per year [1]. According to estimates, growth is only expected to slow by two percentage points to 5% per year by 2030. As in Germany, a large part of value creation is generated by the service sector. Industry and agriculture together only contribute around 1/3 to GDP [2]. With an unemployment rate of 2.7 % (Germany: 3.5 %), it also has the lowest unemployment rate in the EU after the Czech Republic [3]. Incidentally, the national currency is the złoty. One złoty is equivalent to around 0.27 US dollars [4]. The currency has recently appreciated slightly, but interest rate cuts are foreseeable in Poland in the coming months [5].

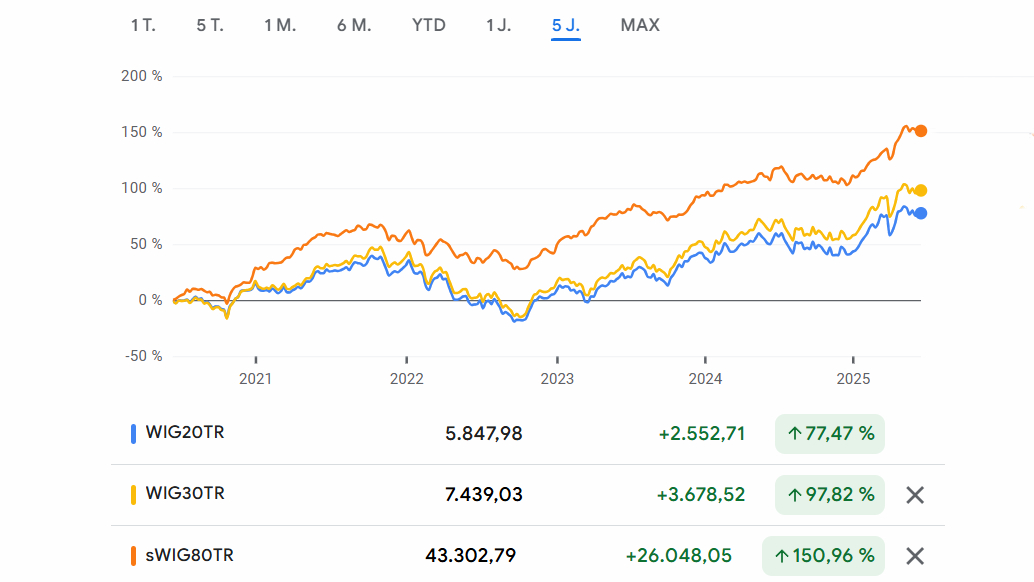

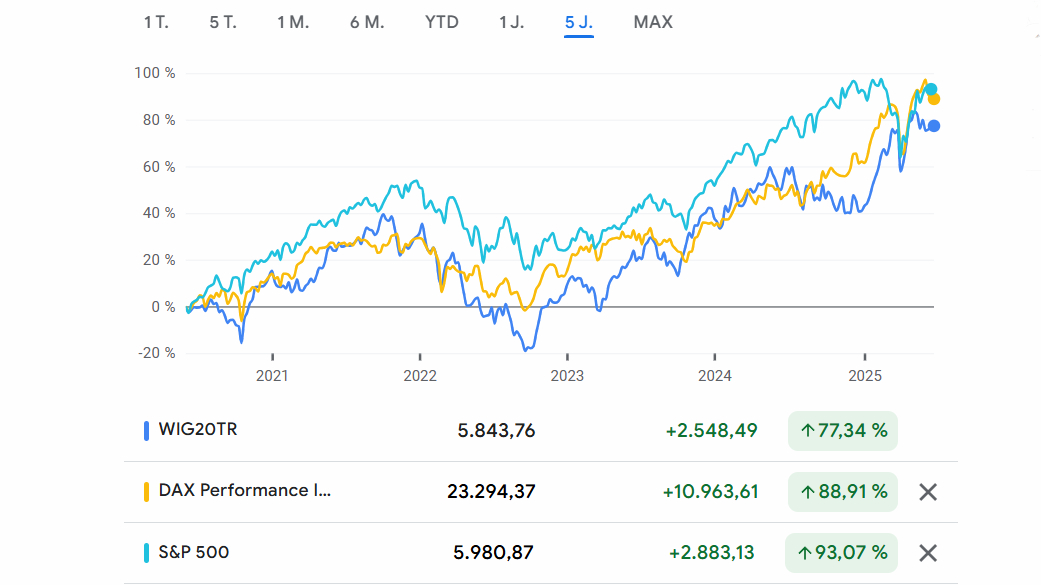

The economic success is also reflected in the share prices of Polish stocks. The best-known index is the WIG20TR performance index. This tracks the 20 largest and most liquid companies listed on the Warsaw Stock Exchange. With an annualized return of around 12 % over the last five years, it is roughly on a par with the German DAX index and the famous S&P 500.

google.com/finance/

It is worth taking a look at the Polish indices that track medium-sized companies. A comparison of the various indices reveals a clear pattern. The smaller the companies covered by the respective index, the higher the return to date. The smallest index, WIG80TR, comprises 80 small Polish companies and has achieved an impressive return of over 20 % per year. This is even better than tech indices such as the Nasdaq 100 (14.5 % p.a.).

google.com/finance/

Disclaimer

This is not investment advice. These are personal assessments and cannot replace professional advice. If you don't want to miss any more stock analyses from me, please subscribe to my free sub-subscription (link in profile).

However, it is difficult to invest in the Polish market via ETFs. However, if you are firmly convinced of Poland, you can take a look at the iShares MSCI Poland UCITS ETF USD (Acc). According to its own statements, the ETF promises "access to the highest-volume companies on the Polish stock market". It contains 13 different stocks. However, the largest position (PKO Bank Polski) is quite overweight with a share of 20% of the total position. The TER of the ETF is also quite high at 0.74% p.a. The past performance correlates strongly with the WIG20TR.

The three stocks

Vercom

With a market capitalization of the equivalent of 600 million euros, Vercom $VRC (+0,26 %) is the most valuable of the three companies. Founded in 2005, the company offers cloud communication platforms (CPaaS) for companies to optimize their relationship with customers. Among its many products is the Emaillabs platform, for example, which can be used to reliably send notifications, password resets, purchase receipts and offers to customers. Turnover rose by 47% to 469 million złoty (112 million euros) in the last financial year. However, the share has its price: according to my own estimates, the P/E ratio is 27. It remains to be seen whether this valuation is justified.

cyber_Folks

cyber_Folks $CBF (+0,29 %) is a Polish technology company. It specializes in web hosting and the registration and transfer of domains. It's like the Polish Ionos, but without its own cloud. With a steadily growing customer base of 370,000 and impressive average revenue growth of 40% since 2005, there is little to complain about in terms of figures. Half of the turnover comes from Poland, the other half is international sales. The company also holds large stakes in the other two shares. It holds 50 % of the shares in Vercom and 49.9 % in the other. The complete takeover of both companies is not planned for the time being, but rather a kind of cooperation in which the various products are implemented across all three companies because they complement each other so well. This will create an ecosystem that can be expanded through possible further acquisitions.

Shoper

Shoper $SHO (-0,1 %) offers a platform based partly on a subscription model. With Shoper, companies can create their own online store. There is also the additional option of launching and managing advertising campaigns. In other words, a Polish equivalent to Shopify. In 2024, turnover increased by 26% to 192 million złoty. The net margin improved from 17% to 19%. The share price is currently 29 times the expected profit for this year. For Shopify it is 80 times. This raises the question of whether this valuation discount is justified and whether Shoper can continue to hold its own in the future.

Sources

[1]

https://de.statista.com/statistik/daten/studie/14410/umfrage/bruttoinlandsprodukt-bip-in-polen/

[3]

https://de.statista.com/statistik/daten/studie/160142/umfrage/arbeitslosenquote-in-den-eu-laendern/

[4] https://www.google.com/finance/quote/PLN-USD?sa=X&ved=2ahUKEwi7zeDfo92NAxWbhv0HHS0VPEUQmY0JegQIChAv