Waste Connect

Price

Discussion sur WCN

Postes

5

Morningstar Best Stocks to own 2026

$ (+3,16 %)TYL (+3,16 %)

$GE (+1,48 %)

$GD (+1,97 %)

$CHRW (-11 %)

$ROL (-1,56 %)

$TW (+0,03 %)

$CSGP (+1,93 %)

$RKT (+0,95 %)

$CLX (+2,23 %)

$ROST (+3,37 %)

$FAST (+2,31 %)

$CSCO (+1,42 %)

$YUMC (+0,4 %)

$KOF (+0 %)

$ORLY (+1,45 %)

$KO (+1,36 %)

$RY (+0,37 %)

$MDLZ (+0,47 %)

$IMBBY (+0,3 %)

$A (-0,77 %)

$IDXX (+1,67 %)

$SONY (+1,65 %)

$MSCI (+0,13 %)

$SYY (+0,77 %)

$VLTO WI (+0,62 %)

$DPZ (+2,1 %)

$IDEX (-1,63 %)

$VRSN (+7,09 %)

$COST (+0,79 %)

$ITT (+0,41 %)

$SHW (+2,42 %)

$EPD

$SIE (+1,02 %)

$CP (+0,15 %)

$CTAS (+2,51 %)

$ROG (+1,36 %)

$BK (-0,71 %)

$CNR (-0,78 %)

$PM (+1,54 %)

$TSM (-3,01 %)

$ITW (+2,28 %)

$APD (+2,05 %)

$PG (+0,06 %)

$AAPL (+4,07 %)

$BAC (+1,16 %)

$CPB (+1,54 %)

$VRSK (+4,13 %)

$HSY (+1,82 %)

$GWRE (+4,74 %)

$HII (-0,4 %)

$GSK (+0,24 %)

$SBUX (+0,51 %)

$ALLE (-0,72 %)

$INTU (+5,24 %)

$MSI (+2,08 %)

$GWW (+1,12 %)

$UNP (+1,14 %)

$WCN (+1,02 %)

$WM (+1,2 %)

$NOC (+2 %)

$CAT (-0,81 %)

$PAYX (+3,22 %)

$ADP (+3,02 %)

$MCO (+1,21 %)

$SPGI (+1,31 %)

$NDSN (+1,32 %)

$WMT (+1,42 %)

$OTIS (+1,35 %)

$CL (+1,32 %)

Best Companies to Own: Methodology

The companies on this list are covered by Morningstar Research Services’ equity analysts and have shares available to US investors. This means that Morningstar equity analysts have calculated fair value estimates for the shares of the companies that trade on US exchanges. As a result, most of the companies on this list are based in the US.

Within that coverage list, the best companies meet the following criteria:

- Wide Economic Moat. The Morningstar Economic Moat Rating summarizes the length of a company’s competitive advantages. An economic moat is a structural feature allowing a firm to generate excess profits over a long period. If Morningstar Research Services believes that excess returns will persist for 20 years or more, that company earns a wide moat rating.

- Standard or Exemplary Capital Allocation.The stock’s Morningstar Capital Allocation Rating is an assessment of the quality of management’s capital allocation, with particular emphasis on the firm’s balance sheet, investments, and shareholder distributions. Capital allocation is judged from an equity shareholder’s perspective, considering companies’ investment strategy and valuation, balance-sheet management, and dividend and share buyback policies on a forward-looking basis. A company can receive an Exemplary, Standard, or Poor Capital Allocation Rating.

- Low or Medium Fair Value Uncertainty. The fair value Morningstar Uncertainty Ratingrepresents the predictability of a company’s future cash flows and, therefore, the level of certainty in the fair value estimate of that company. The Uncertainty Rating for a company can be Low, Medium, High, Very High, or Extreme. It captures a range of likely potential intrinsic values for a company based on the characteristics of the business underlying the stock, including such things as operating and financial leverage, sales sensitivity to the economy, product concentration, and other factors. The more predictable cash flows, the smaller the range of potential intrinsic values, the lower the uncertainty.

What Gives a Company an Economic Moat?

Companies with moats have one or more of the following characteristics:

- Network Effect. Lots of people are using the service, which then makes the service more valuable to the people who use it.

- Intangible Assets. Patents, brands, regulatory licenses, and other intangible assets can prevent competitors from duplicating a company’s products or allow the company to charge a significant price premium.

- Cost Advantage. Firms with a structural cost advantage can either undercut competitors on price while earning similar margins or charge market-level prices while earning relatively high margins.

- Switching Costs. When it would be too expensive or troublesome to stop using a company’s products, the company often has pricing power.

- Efficient Scale. When a niche market is effectively served by one or a small handful of companies, there is no room or incentive for potential competitors to enter the market.

To maintain analysts’ independence, Morningstar Research Services does not publicly rate its parent company Morningstar Inc. Therefore, Morningstar, Inc. is not on the list of the best companies available to US investors.

https://www.morningstar.com/stocks/best-companies-own-2026-edition

Waste Management Q1 2025: Waste professionals with a doctorate?

Waste Management $WM (+1,2 %) is the third largest position in my portfolio with approx. 4.5%... and I feel quite comfortable with that.

The Q1 figures came out on 29.04. I have categorized the figures for myself.

With this post and my general classifications, I am also trying to provide a good, comprehensible overview to give all "shareholders" or future shareholders an adequate insight and ensure an understanding of the company.

SourcesQ1 Report [1] and Earnings Call [2]

WM presents a strong Q1, with double-digit sales growth and a solid operating performance. However, earnings per share are lower despite record sales. Find out why this is not necessarily a bad sign here. Have fun!

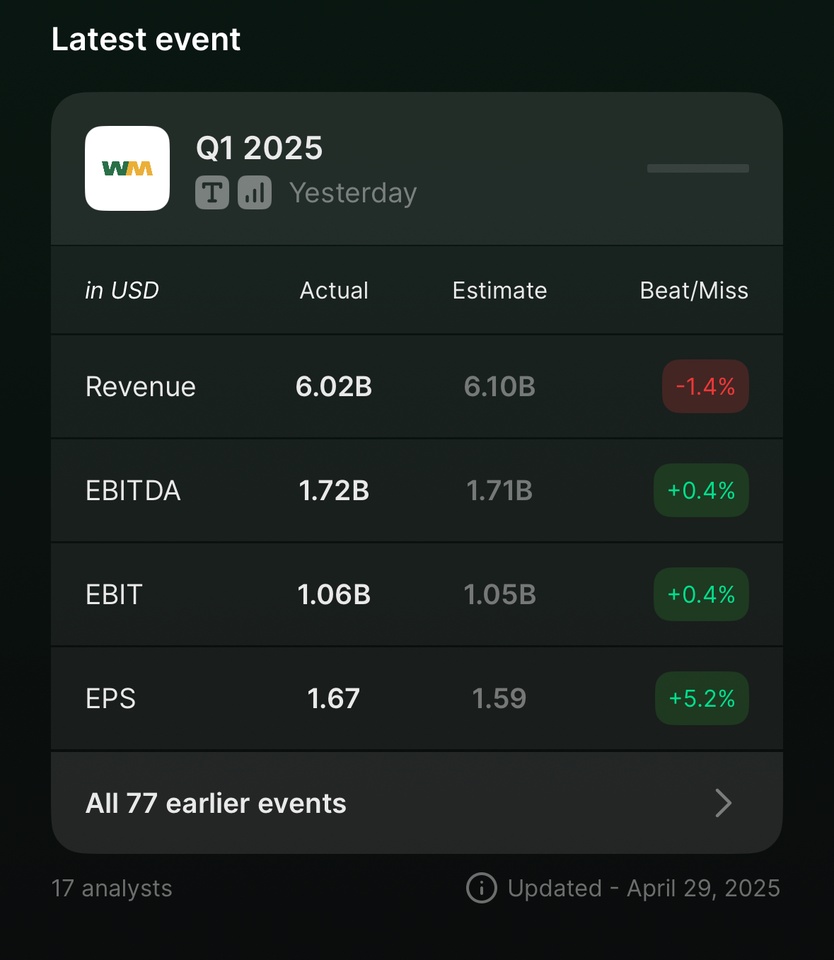

📊 ESTIMATES VS. REPORTED

📊 Q1 figures at a glance

- Turnover6.02 billion $ (+16.7 %)

- Adjusted EBITDA1.72 billion $ (+12.2 %)

- Adjusted EPS1.67 $ (previous year: 1.75 $)

Why is sales growing strongly but EPS falling?

In the first quarter of 2025, WM reported adjusted EPS of $1.67, compared to $1.75 in the previous year, despite a +16.7% jump in sales, does that sound alarming at first? But it's not...

1 . The Stericycle takeover has a double effect: (more context later)

Sales increase because Stericycle is now fully included in the balance sheet ($619m sales in Q1).

At the same time, however, costs are also rising:

- Interest payments on new debt that was used for financing

- Amortization of the purchase price

- One-off integration costs (e.g. system conversions, personnel)

All of this has a negative impact on earnings per share, even though the new division is already profitable.

2 . Special tax effects & discontinuation of subsidies

- In the previous year, WM benefited from tax credits for alternative fuels, which expired in 2025.

- This explains part of the decline compared to the strong Q1 2024.

3 . Higher capital costs put pressure on free cash flow

- Even though operating cash flow remained solid ($1.21 billion), free cash flow was only $475 million, leaving less room for buybacks or earnings growth.

Conclusion so far: The falling EPS is not a warning signal, but a consequence of...

- strategic growth (acquisition),

- temporary integration costs,

- expiring tax benefits and

- increased interest rate environment.

In the long term, EPS should improve again significantly as soon as synergies from the Stericycle integration and new RNG/recycling plants take effect.

🚛 What is the traditional core business doing?

The so-called legacy business includes:

- Collecting, transporting and disposing of waste

- Customers: Cities, households, companies

- Service: Planning, logistics, landfills, disposal & recycling

Q1 2025:

- Turnover5.40 billion $

- Adjusted EBITDA1.62 billion $

- EBITDA margin: 30 % (Q1 2024: 29,6 %)

- EBITDA growth: +5 % YoY

Growth driver:

- Core pricing +6.5 %

- Cost optimization:...

COO John Morris:

"We reduced operating costs for the sixth consecutive quarter, now at 60.5% of sales."

The reason for this:

- Focus on employee retention & process automation

- Route planning & resource deployment improved through digital tools

- Residential margin at 20% for the first time in 6 years due to targeted withdrawal from low-margin customers

- Withdrawal from residential (private households):

- A lot of effort, low margin

- Focus now on commercial & industrial = better cost/income ratio

Comment (COO John Morris):

"This was the fourth quarter in a row with a 30% margin and that despite a difficult basis for comparison and winter influences."

WM is concentrating on quality rather than volume, more income through targeted pricing and a focus on high-margin customers.

💊 WM Healthcare Solutions Stericycle takeover: between waste and medicine, WM reorganizes itself

WM acquired Stericycle, the leading provider of medical waste disposal, for $7.2 billion in 2024.

The business is less cyclical, fast-growing and in a regulated market.

Q1 2025:

- Turnover619 million $

- EBITDA95 million $

- EBITDA margin: 15,3 %

- Margin improvement compared to Q4 2024: +20 basis points

- Target synergies: $80-100 million in additional EBITDA by the end of 2025

- Target synergies: USD 250 million annually by 2027 (ongoing savings + efficiency gains)

-> e.g. through joint administration, logistics, location optimization

Comment (CEO):

"Our customers value our digital environmental platform and nationwide network - a clear competitive advantage."

♻️ Recycling & Renewable Energy

- Recycling: WM sorts & sells raw materials such as paper, plastic and metal

- Renewable Energy: Recovery of biogas (RNG) from landfills

Q1 2025:

- Combined EBITDA contribution18 million $

- Ø price for recycled raw materials88 $/ton (previous year: 84 $)

- Positive increase, but still below previous highs (e.g. 2022: approx. 120 $)

An EBITDA contribution of $18 million compared to total EBITDA of $1.72 billion?

That sounds vanishingly small? I asked myself the same question...

Why the amount seems low, but still fits

1 . Recycling & Renewable Energy are capital-intensive, long-term oriented

- These areas require high investments in advance (e.g. plants, automation, RNG projects).

- The returns come over years, not in the first or second quarter.

2 . Growth still in the start-up phase

- Many plants (especially RNG) are still under construction or have recently come online.

- CEO Jim Fish said: "8 new RNG plants are currently under construction, all of which are scheduled for completion in 2025."

- The full EBITDA impact will therefore only unfold later.

3 . Recycling margins are heavily dependent on raw material prices

- Prices for recycled raw materials were $88/tonne in Q1, which is well below previous highs (e.g. 2022: $120).

- Ergo: fluctuating contribution to EBITDA, but not a structural problem.

4 . Benchmark: 20% growth YoY

- EBITDA from Recycling & Renewable Energy increased by >20% compared to Q1 2024 .

- The trend is therefore positive, even if the absolute figure appears small.

➡️ It is a growing business area with long-term potential. EBITDA contributions will increase in the next quarters & years as soon as new plants are up and running.

💰 Further financial figures

- Adjusted EBITDA margin (total): 28.5% (previous year: 29.6%)

- Free cash flow: $475 million (previous year: $714 million)

- Investments in sustainability128 million $

- Cash position216 million (end of 2024: $414 million)

Further voices from the earnings call:

CFO Devina Rankin on financial strategy & risks

- Free cash flow in Q1 as planned: $475 million

- CapEx at $831 million, focus on sustainability & fleet ramp-ups

- Customs risks lowas WM pre-produced equipment at an early stage

- Share buybacks further paused, focus on deleveraging

- Leverage ratio: 3.58x, target by the end of 2025: ~3.15x

"Despite interest burden and investments, we are fully on track - operational strength and synergy potential remain intact."

CEO Jim Fish emphasized:

"I'm proud of the fact that we've become a predictably strong performer, quarter after quarter, over the past few years."

He sees WM in a strong strategic position, particularly thanks to three drivers:

- Growth in the core business (Collection & Disposal)

- strong contribution from Stericycle

- Sustainable investments in recycling & biogas (RNG)

Particularly exciting:

- The automated recycling centers achieved EBITDA margins twice as high as non-automated plants.

- 2 new plants went online in Q1, with 7 more to follow by the end of 2025.

- 8 new RNG plants are under construction, all with high yields and progressing according to plan.

"Our sustainability strategy is working, these projects are delivering strong, growth-oriented EBITDA."

The call once again showed how operational fine-tuning, automation and acquisitions go hand in hand and underlined the following points:

- Technology and pricing secure margins

- Sustainability is more than a buzzword, it delivers profit

- Stericycle brings new potential that is structurally anchored

P/E ratio & current valuation (personal assessment, no investment advice)

Current level: ~ 34,49

In recent years: between 25-30

➡️ the current P/E ratio signals that the market believes WM will continue to enjoy stable growth and security.

Are there any special effects in earnings that distort the P/E ratio?

Yes, the ones already mentioned. Nevertheless, explained again:

1 . EPS (earnings per share) is currently falling slightly due to:

- Interest costs due to Stericycle financing

- Depreciation & integration costs

- Elimination of tax credits for alternative fuels

➡️ This means:

- The "G" in the P/E ratio is currently under pressure, but not structurally weakened

- The P/E ratio appears artificially higher because earnings are temporarily lower

➡️ The current high P/E ratio is explainable and temporary

- WM remains a defensive quality stock with strong cash flow

- Not a bargain, but a solid investment for long-term strategists

- If you think long-term (3+ years, you will find a company with a clear strategy & growth path here

🔮 Conclusion & outlook

WM remains a fundamental long-term runner with vision.

Although the Stericycle financing is putting pressure on EPS and cash flow in the short term, the focus on high-margin areas, sustainability and healthcare opens up long-term potential.

- Positive: Strong legacy business, successful entry into healthcare disposal

- NeutralEPS slightly down, cash flow temporarily under pressure

- RisksInterest costs, margin pressure in recycling, political uncertainty regarding sustainability

My conclusion: WM delivers structurally, those who think long-term will find stability and perspective here.

I remain invested, position will not be increased for the time being.

________________

Thank you for reading 🤝

________________

Sources:

[1] https://investors.wm.com/static-files/00de6f79-f0b6-4b6a-af79-9e5f892c73f5

[2] https://investors.wm.com/static-files/9db3d0d5-0c4d-47fa-aab1-f0bf71a86859

_______________

$WM (+1,2 %)

$RSG (-0,18 %)

$WCN (+1,02 %)

$CLH (-0,85 %)

$CWST (-0,66 %)

"1, 2 or 3 You have to decide three fields are free. Pop! Plopp, that means stop, just one more hop, then it stays that way".

𝗠𝗮𝗿𝗸𝗲𝘁 𝗡𝗲𝘄𝘀 🗞️

𝗛𝗲𝗿𝘁𝘇𝘀𝗰𝗵𝗹𝗮𝗴 / 𝗗𝗲𝗿 𝗧𝘄𝗶𝘁𝘁𝗲𝗿-𝗘𝗹𝗼𝗻 / 𝗚𝗮𝘀𝗽𝗿𝗲𝗶𝘀 𝗿𝘂𝗻𝘁𝗲𝗿 / 𝗘𝘀 𝗸𝗮𝗻𝗻 𝗻𝘂𝗿 𝗲𝗶𝗻𝗲𝗻 𝗴𝗲𝗯𝗲𝗻

𝗜𝗣𝗢𝘀 🔔

Hertz - Car rental company Hertz Global Holdings has set the terms for its "re-IPO." Hertz plans to offer 37.1 million shares at $25 to $29 each. They are to be tradable on the Nasdaq under the symbol HTZ. The company generated earnings before interest, taxes, depreciation and amortization (EBITDA) of $860 million in the third quarter.

𝗘𝘅-𝗗𝗮𝘁𝗲𝘀 📅

As of today, AdvanSix ($960 (-1,28 %)), Carlyle Group ($3VU (+2,31 %)), Carriage Services, Inc. ($CSV (+3 %)), Hanesbrands ($HN9), HomeStreet Bank ($HMST), Invitation Homes ($4IV (+0,77 %)), Kennametal Inc. ($KM3 (+0,65 %)), Landstar System ($LDS (-2,74 %)), Macerich ($M6G (+1,79 %)), MetLife ($MWZ (+2,75 %)), Northeast Bank ($NBN (+1,33 %)), Papa John's Pizza ($PP1 (-0,74 %)), Terex ($TXG (+1,66 %)), Westpac ($WBC (+1,73 %)), Webster Bank ($WED (+0,75 %)) and Waste Connections ($UI51 (+1,02 %)) traded ex-dividend.

𝗤𝘂𝗮𝗿𝘁𝗮𝗹𝘀𝘇𝗮𝗵𝗹𝗲𝗻 📈

Today, among others, Akasol ($ASL), bet-at-home.com ($ACX (-0,76 %)), Covestro ($1COV (-0,42 %)), Denki Kagaku Kōgyō ($DIK (-0,51 %)), Fujikura Ltd. ($FJK (-4,56 %)), Henkel ($HEN (+0,29 %)), HolidayCheck ($HOC), Hypoport ($HYQ (-1,56 %)), International Flavors & Fragrances ($IFF (+2,98 %)), Isuzu ($ISUZY), Jack Henry & Associates ($JHY (+1,65 %)), Nippon Kayaku ($NP7 (+0 %)), PayPal ($2PP (+3,79 %)), PhosAgro ($P6SG), Softbank ($SFT (-6,61 %)), Teijin ($TIJ (-0,55 %)) and Yamaha Motor ($YMA (-0,35 %)) presented their figures.

𝗠𝗮𝗿𝗸𝗲𝘁𝘀 🏛️

Elon - Tesla($TL0 (-3,46 %))-founder Elon Musk has let his fans vote on Twitter whether he should sell ten percent of his Tesla shares. Most recently, the 50-year-old faced calls to pay more taxes to help solve the world's problems. Of just over 3.5 million users, 58 percent voted in favor of a sale. This would make the block of shares to be sold worth around $20 billion currently. Based on this vote, the Tesla share price slumped by an interim 8.47 percent to EUR 965.66.

Gazprom ($GAZ) - After several months of energy crisis and rising prices, the Russian gas company is now supplying gas to Germany and Austria again under pressure from Putin. The Gazprom Vice-Chairman also stated that Russia had no interest in such high gas prices, as this would accelerate the transition of renewable energies in Europe.

𝗖𝗿𝘆𝗽𝘁𝗼 💎

Shiba Inu ($SHIB) - The co-founder and creator of Dogecoin, the origin of all meme coins, explicitly distanced himself from Shiba Inu last Sunday. He also emphasized that he himself is also not a holder of the comparatively new meme coin. Before that, various theories circulated that he could be involved in the project.

New York - The newly elected mayor of the city of New York is seamlessly following up on his bullish statements on the topic of cryptocurrencies. Thus, he stated in an interview on Sunday that especially in schools should be taught about blockchain technology, about cryptocurrencies and about the new opportunities associated with them. Despite the clear attitude of the mayor, he still believes that the implementation of digital currency in the real world should not be rushed, but should be realized with intelligence and accuracy.

Follow us for french content on @MarketNewsUpdateFR

Titres populaires

Meilleurs créateurs cette semaine