Hello my dears,

apart from a lot of blah blah blah, there wasn't much news during the night.

So stay brave and stick to your strategy, better days will come.

The stock market will survive even Captain 🍊.

"DAX slumps after Trump speech - oil prices rise sharply again"

So let's get to the nice and cozy part of the day.

You've voted and I'll deliver.

Only not quite because I've just seen that TJX has passed Dollarama on the home straight🏁.

So today I present the runner-up of the vote, and will probably have to deliver the winner over Easter.

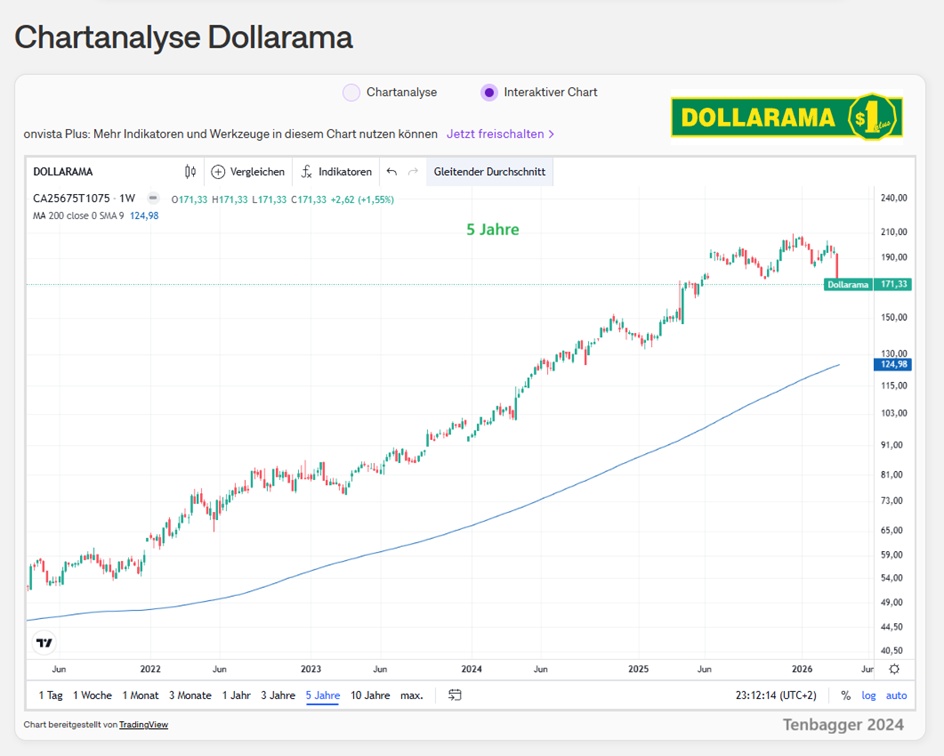

But for now, have fun with Dollarama $DOL

"Proudly serving customers across the country."

Dollarama Inc. is a Canada-based company that offers a wide range of general merchandise, consumables and seasonal items both in-store and online. The company operates its business through its subsidiaries, including Dollarama L.P. and Dollarama International Inc (Dollarama International). Dollarama L.P. operates the chain of stores in Canada and performs related logistical and administrative support activities. Dollarama International operates retail stores in Latin America through Dollarcity, a retail company that offers a range of general merchandise, consumables and seasonal items in stores in El Salvador and Guatemala, as well as in stores in Colombia and Peru. All stores are owned and operated by the company. They are located in large cities, medium-sized towns and small towns. The company operates approximately 1,569 stores across Canada.

Number of employees: 14,230

Dollarama shares fall as annual sales forecast misses expectations

Published: 11:05 March 24, 2026

The Canadian discount retailer expects comparable sales growth of 3% to 4% for the 2027 financial year, below analysts' consensus of 3.9%.

The forecast follows the results of the fourth quarter of 2026, which were mixed compared to expectations. For the quarter ended February 1, 2026, Dollarama reported net income of 392.5 million Canadian dollars, an increase of 0.4% year-over-year, with diluted earnings per share of 1.43 Canadian dollars, slightly exceeding the estimate of 1.41 Canadian dollars.

Sales rose 11.7% to 2.1 billion Canadian dollars, driven by expansion in Canada and Australia, while comparable store sales in Canada rose only 1.5%, below the consensus of 2.6%. The shortfall was attributed to poor weather and a calendar shift that reduced the busy shopping days leading up to the holidays.

Operating income for the quarter grew 4.7% to 584.4 million Canadian dollars, with an operating margin of 27.8%, down from 29.7% a year earlier. EBITDA increased by 6.2 % to 711.5 million Canadian dollars, which corresponds to a margin of 33.9 %.

During the quarter, Dollarama opened seven net new stores in Canada and one in Australia and repurchased approximately 888,000 shares for 174.8 million Canadian dollars.

Looking ahead, Dollarama expects to return to its historical pace of 60 to 70 net new store openings in Canada in fiscal 2027, while maintaining gross margin guidance of 45% to 45.5% and SG&A in the range of 14.1% to 14.6%.

Analysts at Jefferies said the company delivered strong earnings, but pointed out that growth at the Canadian store level fell short of expectations, reflecting calendar effects and weather-related disruptions.

They also pointed to margin pressure from the peak period of Australian operations, resulting in higher operating costs and a moderate decline in EBITDA margin. Despite these short-term challenges, the company highlighted that Canadian sales remained resilient, with growth supported by higher average transaction values.

Jeffer also pointed out that the company's international operations, including Dollarcity, were solid contributors to overall results and emphasized that Dollarama's ongoing share buybacks and dividend increases demonstrate financial flexibility, even as investments in Australia continue.

The company has a 'Buy' rating and a price target of $235 at Jefferies, which implies an upside from the current level of around $173.

Dollarama shares drop as annual sales forecast misses estimates

DOLLARAMA ANNOUNCES PRIVATE ISSUANCE OF 750 MILLION DOLLARS SENIOR UNSECURED BONDS

MONTREAL, March 31, 2026

A leading Canadian value retailer

Geographical distribution of turnover:

(2026 CAD)

Canada 6.8 billion

Australia 455 million

CAD in millions

Estimates

Year Turnover Change

2025 6.413 9,3 %

2026 7.256 13,14 %

2027 8.099 11,62 %

2028 8.647 6,77 %

2029 9.342 8,04 %

Year EBIT Change

2025 1.711 14,37 %

2026 1.938 13,28 %

2027 2.125 9,63 %

2028 2.362 11,16 %

2029 2.565 8,61 %

Year Net result Change

2025 1.169 15,64 %

2026 1,309 12,06 %

2027 1.408 7,54 %

2028 1.584 12,51 %

2029 1.787 12,82 %

Year Net debt CAPEX

2025 2.160 246,9

2026 2.294 272,8

2027 5.134 499,7

2028 4.918 354,8

2029 5.776 341,6

Year Free cash flow Change

2025 1.397 11,59 %

2027 1.047

2028 1.397 33,39 %

2029 2.043 46,24 %

Year EBITDA margin EBIT margin ROE

2024 31,71 % 25,49 % 493,8 %

2025 33,09 % 26,67 % 148,94 %

2026 33,05 % 26,71 % 99,04 %

2027 31,96 % 26,23 % 72,5 %

2028 32,94 % 27,31 % 57,03 %

2029 33,7 % 27,46 % 54,3 %

Year Earnings per share Change

2025 4,16 16,85 %

2026 4,73 13,7 %

2027 5,141 8,7 %

2028 5,844 13,66 %

2029 6,73 15,16 %

Year Debt ratio FC Yield

2025 1,02x 3,47 %

2026 0,96x

2027 1,98x 2,03 %

2028 1,73x 2,71 %

2029 1,83x 3,9 %

Year Dividend p share Yield

2025 0,368 0,27 %

2026 0,4332 0,23 %

2027 0,5025 0,29 %

2028 0,56 0,33 %

2029 0,6667 0,39 %

Year P/E ratio PEG

2025 33.1x 32.5x 2x

2026 38.8x 34.9x 2.8x

2027 33.2x 22.8x 3.82x

2028 29.2x 18x 2.1x

2029 25.4x 15x 1.7x

Market value 46,563

Number of shares (in thousands) 272,731

Date of publication 24.03.2026

Fundamental strengths of Dollarama

✔️ 1. very robust business model

- Value retailers benefit in all economic phases, especially in weaker times.

- High price sensitivity of customers → Dollarama gains market share when consumers need to save.

✔️ 2. Steady, predictable growth

- Double-digit increases in sales and profits for years.

- Expansion in Canada almost complete, but:

- Latin America growth above Dollarcity (Guatemala, Colombia, El Salvador, Peru) is a real driver.

✔️ 3. High margins for a discounter

- Economies of scale + efficient logistics

- Private label strategy

- Very strong cash conversion

✔️ 4. Crisis-resistant

- Dollarama was one of the most stable retail stocks in North America in 2020-2023

What type of investor is Dollarama suitable for?

👍 Well suited for:

- Long-term buy-and-hold investors

- Investors who want stable, predictable cash flows

- Investors who are willing to pay a premium valuation for quality

👎 Less suitable for:

- Value investors

- Dividend collectors

- Traders who want to play short-term volatility

My personal assessment (clear & direct)

Dollarama is an excellent companybut the share is not cheap. If you are investing for the long term (5-10+ years), Dollarama can be a solid core holding candidate similar to Costco or Walmart, only smaller and more focused.

For a new entry, I personally would rather wait for setbacks towards 150-160 CAD to get a better risk/reward ratio.

Analysis by Mr. Prompt follows in the comments!