Hi everyone,

I first set out on my investment journey because I dreamed of a life where I could afford everything I wanted, without having to compromise. 🏜️

Early on in this journey, I stumbled upon the FIRE movement, and for a long time, my motivation was to build enough wealth that I wouldn’t have to work anymore. 😎

As my wealth grew, my financial goals kept shifting a bit higher. At some point, I started thinking I wanted to be a millionaire. Then I started thinking I wanted to be a multimillionaire. 🤑

Well, somehow there’s no reasonable limit—or at least, I’ve been subconsciously pondering for quite a while where that limit actually lies for me personally.

In the last few days, there have been several posts, including ones by @Dirty30 , @1Chrischi1 , @FinanzPapa ,@Hahajjk and, in particular, from the lovely @DonkeyInvestor , that have dealt with the withdrawal phase, building up a lifestyle to live off of it, and, in particular, concrete goals. 🎯

Over the past few years, the idea has matured within me that no longer having to work isn’t a meaningful goal. Sure, I can easily imagine taking lots of vacations and traveling. But still, I’m increasingly coming to realize that regular work is fundamentally good for us humans and gives us stability. ⚖️

That’s why my goal of no longer having to work as soon as possible has vanished into thin air. 🎈💥

At the same time, over the past three years, I’ve experienced illness and had to cope with unexpected deaths among my close and extended circle, which have made my desire to put everything off for later shift even more clearly toward experiencing as much as possible in the here and now. 🏥⚱️

Not that I haven’t been doing that. But I want to spend less mental energy worrying about the future going forward (does that sentence even make sense?!? :D).

So what does the perfect compromise look like for me? Inspired by our @DonkeyInvestor , I’ve defined a clearer, more tangible goal for myself over the last few days and committed to it. I plan to start allocating parts of my assets to my lifestyle much sooner and put my savings plans on hold. 🚢

This also has to do with the fact that, at 34, I’m already much further along than I could ever have dreamed. Now I’d like to share my thoughts on this with you to get feedback on the idea and its theoretical implementation.

Over the last few days, I’ve worked with Claude to develop the rough idea into a more comprehensive simulation, which has now led me to a detailed concept. The concept isn’t set in stone, but I think it will serve as an excellent guideline for me. I’ve experimented with various parameters and their adjustments in every possible direction to develop a plan that promises me, as quickly as possible:

- initial withdrawals,

- without going broke

- where the assets continue to grow as much as possible

- ensures that withdrawals continue to grow as much as possible

- ensures I’m fully covered starting at age 60

- I squeeze the maximum lifetime withdrawals out of my savings (because that’s why I started in the first place...). 🧭

The plan:

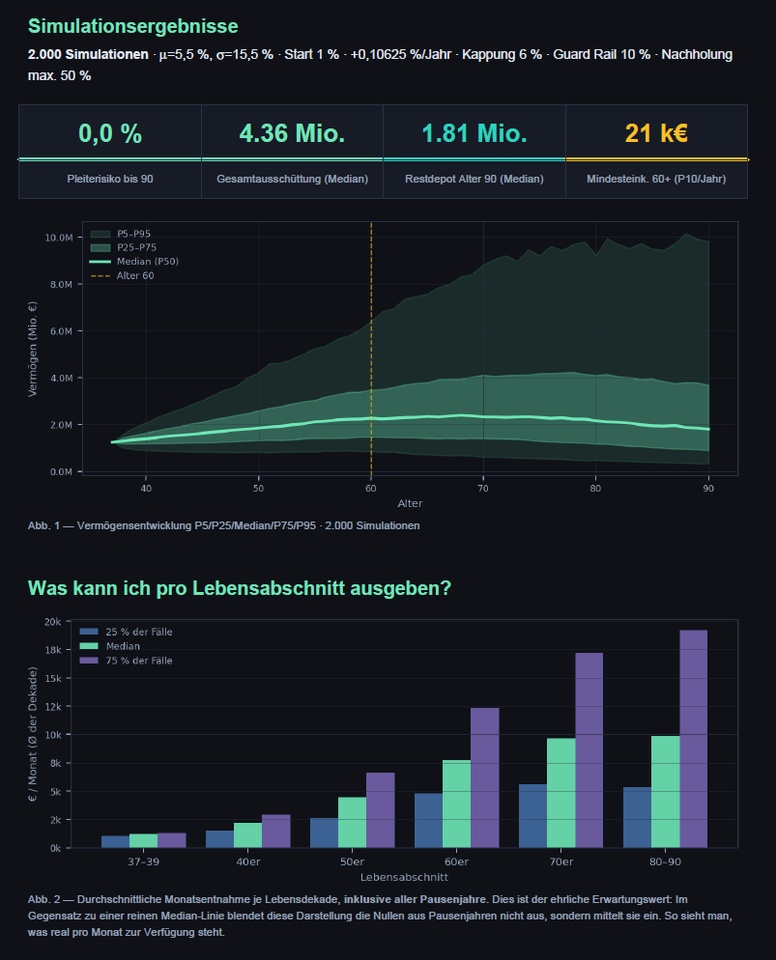

Once my net worth reaches 1.25 million euros, I will stop my savings plans, which will immediately open up entirely new financial possibilities for me, since my wife and I have maintained savings rates ranging between 30% and 70% over the past 10 years. In addition, I will withdraw 1% of my assets and add it to my spending budget. Since my capital isn’t entirely invested in the stock market (we started investing in real estate in our 20s), I calculated using an average return of 5.5% per year and ran the simulation with a variance of 15.5%.

Since the withdrawal is supposed to increase annually, I looked for the best growth rate, which turned out to be a plus of 0.10625% per year. The maximum withdrawal should be 6% per year.

To avoid severely damaging the portfolio during negative capital market phases, a 10% guard rail has proven to yield very good results. What does that mean? If my portfolio ever falls more than 10% below its all-time high (ATH), I will forgo the withdrawal for that year. Instead, the withdrawal will be made up as soon as I’m back above 90% of my ATH. If no withdrawals are allowed for several years in a row, a maximum of 50% of the portfolio will be withdrawn when making up the difference (this is a theoretical rule for the simulation; in reality, I would never withdraw such a substantial amount; however, I find it fascinating how robust the simulation still is; to me, this means that things could actually go even better in reality)

You can find the graphical representation of the Monte Carlo simulation here:

In my simulation, I used my dream scenario, in which I have a total net worth of over 1.25 million by age 37. With conservative planning and a 5.5% return, this could generate an incredible 4.36 million in spending power 🚀

With a little luck, the whole thing could, of course, skyrocket… 💣

What do you think of this in general? What would you do differently? Have your goals shifted over time, or even changed completely? Why have your goals changed?

I’d be happy if anyone who’s read this far would leave a comment :)