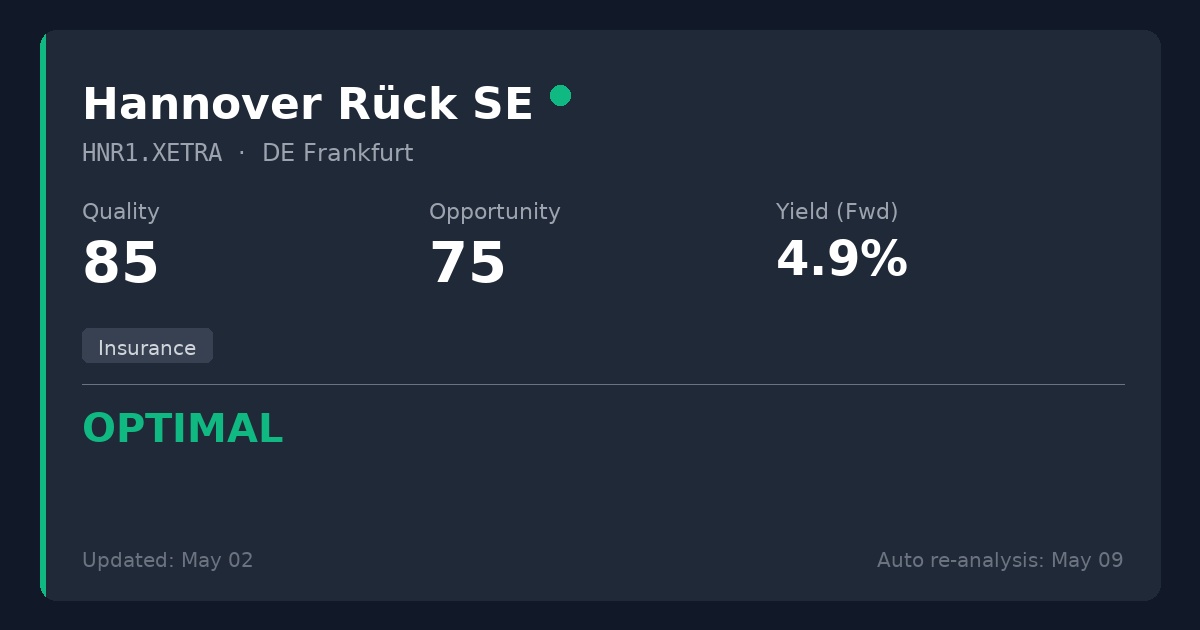

Sharing some current data and context on Hannover Re $HNR1 (-0,62 %) , which is sitting in the 🟢 OPTIMAL quadrant on DividendQuad.

The Quantitative Picture:

• P/E Ratio: 11.74x

• Dividend Yield: 4.88%

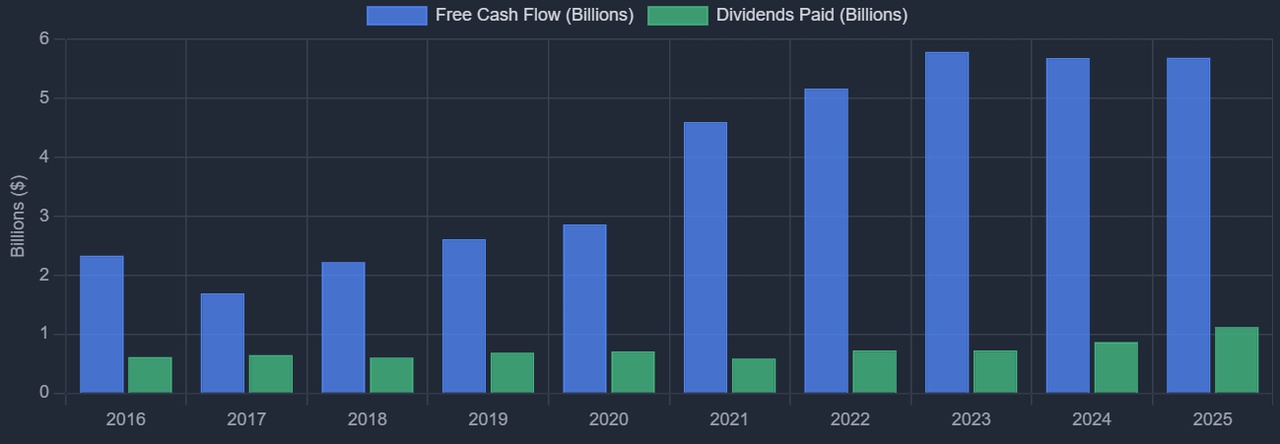

• FCF Payout Ratio: 19.7% (Showing the dividend is well-covered by cash flow, despite standard screeners showing a distorted GAAP payout of >100%)

The Market Context:

The low multiple reflects some specific industry headwinds. The market is pricing in caution due to reports of a slightly softening environment during the 1/1 renewals. Additionally, Hannover Re's strategy of taking on more tail-risk compared to peers (like SCOR) has kept some investors on the sidelines following heavy catastrophic loss years recently.

The Counter-Balance:

Despite those concerns, the underlying financials remain robust:

• 2025 closed with a strong combined ratio below 90%.

• Management is projecting net income of at least €2.7 billion for 2026.

• They actively mitigate their tail-risk exposure by sharing a significant portion of large losses with ILS (Insurance-Linked Securities) investors.

Between the strong cash generation and disciplined underwriting, it's an interesting setup.

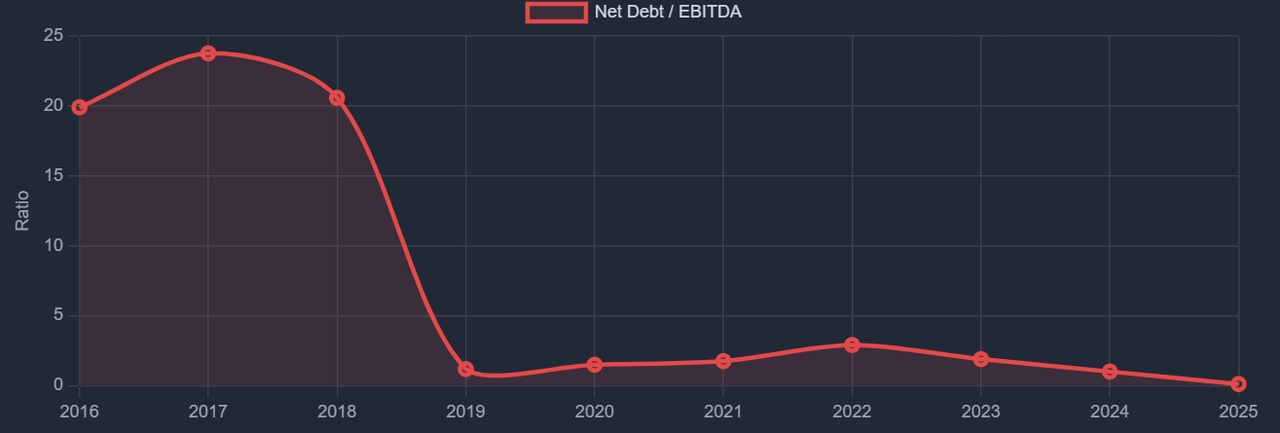

(Charts from DividendQuad. Data powered by EODHD).