Good morning my dears

Juan has already arrived back in the USA and visited a company for you in San Jose, California.

Which we may even introduce to you this afternoon.

So you can start the new stock market week with these two companies in mind and be well prepared.

During this time, I continued to work on the topic of energy in Europe.

Today I would like to introduce you to a player that is not entirely unknown to most of you. Some of you may be surprised that I am introducing you to this company today on the subject of energy and electricity 🔌.

The Group is benefiting from several global megatrends at the same time: increasing air traffic, the defense boom, energy demand from AI data centers and Small Modular Reactors (SMR).

Emergency power solutions for data centers and SMR technology are particularly exciting.

Now some of you will probably know that this is about Rolls Royce $RR. (+0,15 %) is involved.

As always, we look forward to opinions and a discussion in the comments. As always, the Prompt family is also invited to join in.

(@Raketentoni / @Aktienhauptmeister )

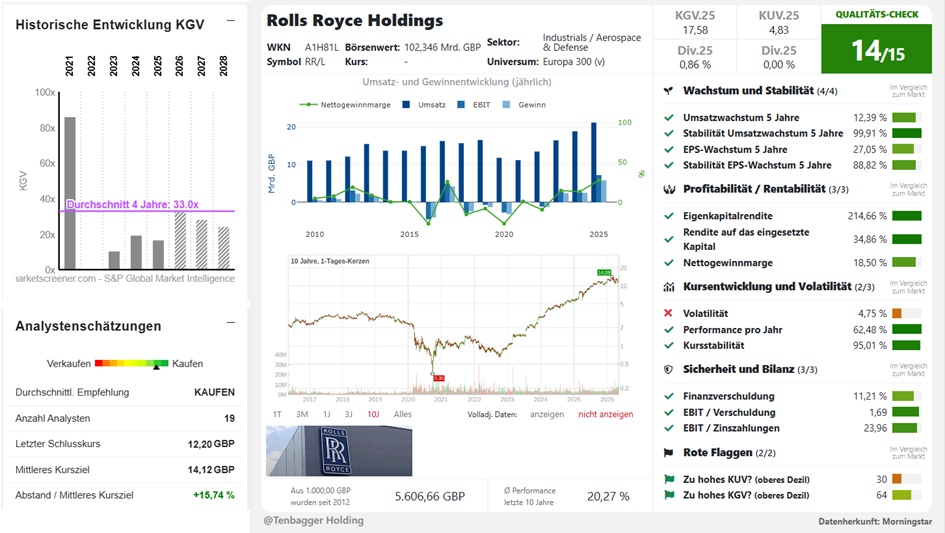

Rolls-Royce Holdings plc specializes in the development, manufacture and marketing of engines for the aviation, marine and energy sectors. The breakdown of net sales by product family is as follows:

- civil aircraft engines (51.8%);

- military aircraft engines, marine engines and submarine nuclear power plants (23.8%);

- Energy and propulsion systems (24.4 %): intended for power plants.

The geographical breakdown of net sales is as follows: United Kingdom (14.6 %), Germany (5.8 %), Europe (14.6 %), United States (27.4 %), North America (2.5 %), China (7.1 %), Asia (13.5 %), Middle East (7.9 %), Africa (2.8 %), Australasia (2 %), Central and South America (1.8 %).

Number of employees: 43,162

Breakout alert for the winner of several megatrends! Rolls Royce Holdings on the upswing after figures

Von S. Bank - Updated on 06.05.26 13:43

Rolls Royce Holdings is bucking the weakness among defense stocks. There are good reasons for this: The company is in the midst of a far-reaching transformation to become a "highly profitable, resilient growth company". Particularly striking: strong margin increases, high free cash flow and growth in all three core segments - Civil Aerospace, Defense and Power Systems. The Group is simultaneously benefiting from several global megatrends: increasing air traffic, the defense boom, energy demand from AI data centers and Small Modular Reactors (SMR).

Civil Aerospace is the Group's most important cash flow driver. The aftermarket business is particularly attractive, as maintenance contracts deliver high margins over decades. The 'Defense' segment delivers stable cash flows with long contract terms and a high level of political support. Of particular interest: nuclear technologies and future fighter jet platforms. The 'Power Systems' segment is developing into the Group's AI and energy winner. Emergency power solutions for data centers and SMR technology are particularly exciting.

The Power Systems division delivered a record order intake in the first quarter, driven by data centers and government contracts. With an order backlog of GBP 7.3 billion in this division, planning reliability for the coming quarters is high. The company also recently secured further long-term revenue streams in the defense segment by equipping the Australian frigates and the Turkish Eurofighter fleet. The financial targets for 2026 remain unchanged with an underlying operating profit of GBP 4.0 billion to GBP 4.2 billion and a free cash flow of GBP 3.6 billion to GBP 3.8 billion.

Rolls-Royce Holdings plc-2025 Full Year Results – Presentation

Juan analysis on Rolls-Royce (2025-2028)

(short, precise, investor-focused - in the typical Juan tone)

1. growth & momentum

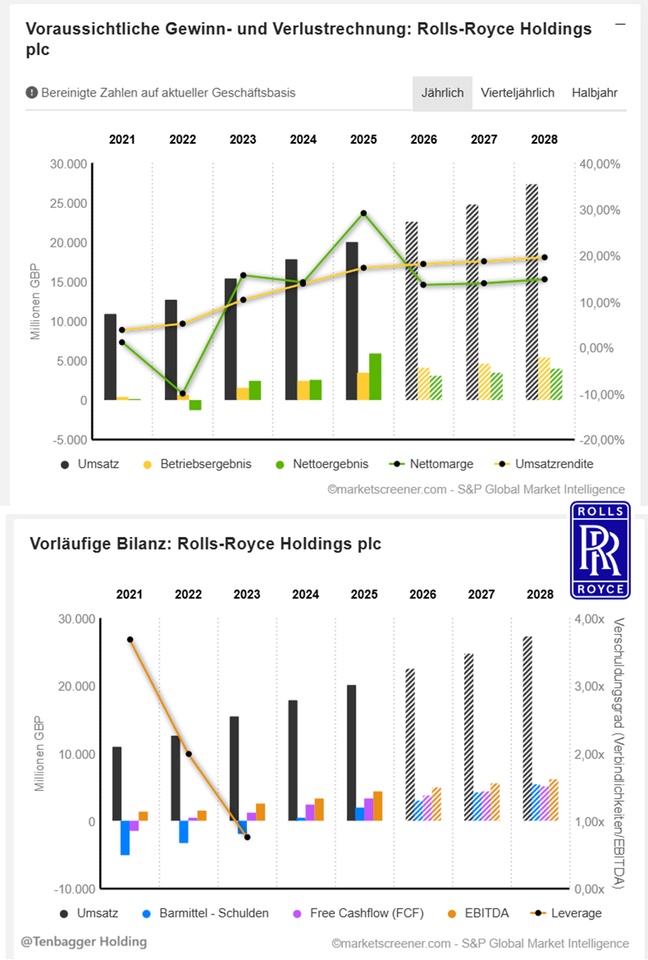

Rolls-Royce delivers four years of continuous double-digit sales growth. 2025-2028 sales increase from £20.1 billion → £27.3 billion.driven by commercial engines, services and defense. The EBIT increase remains strongbut normalizes after the turnaround: from +40 % (2025) to +15 % (2028).

2. profitability

The margins show a clear picture of a company that wants to return to the Champions League:

- EBITDA margin rises to 22,36 %

- EBIT margin climbs to 19,53 %

- FCF margin improves to 18,62 %

This is extremely strong for an industrial group extremely strong and signals structural efficiency.

3. cash flow & balance sheet

Free cash flow grows from £3.27 billion → £5.09 billion. - a massive lever for valuation and debt reduction. Net debt turns deeply negative: -£1.97bn → -£5.43bn. → Rolls-Royce becomes effectively net debt-free and builds up liquidity.

4. profitability & return on capital

The ROE is extremely distorted due to the return to positive equity extremely distortedbut the direction is right: 2026-2028: 126 % → 172 % → Signal: Turnaround completed, capital base healthy again.

5. valuation & outlook

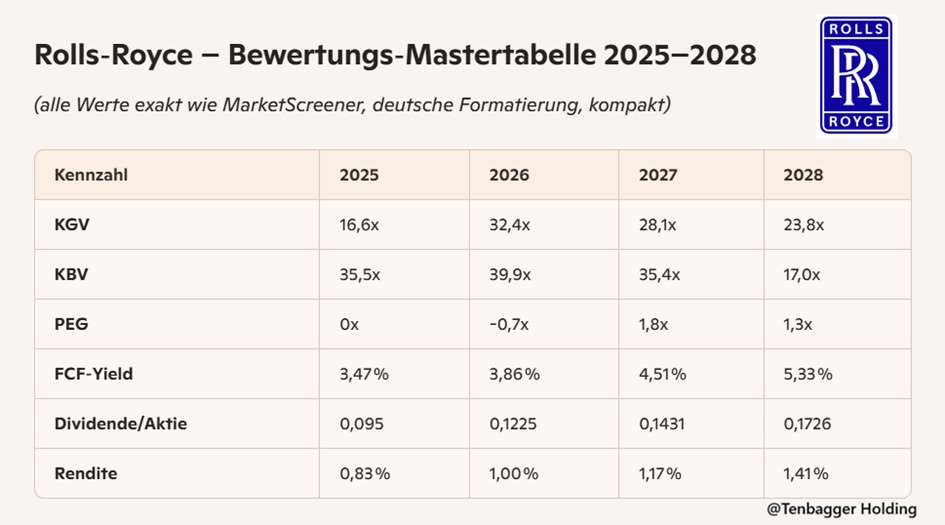

EPS clearly increases: 0,69 → 0,51 (2025-2028, with dip in 2026). However, the operating story remains intact:

- rising margins

- rising cash flow

- Decreasing debt

- structural demand in the engine and service business

Juan's conclusion

Rolls-Royce is no longer a turnaround casebut a scaling cash flow compounder. The combination of margin expansion, strong FCF and massive debt reduction makes the share one of the most attractive quality re-ratings in the European industrial sector. For momentum and FCF investors, Rolls-Royce remains a top tier.

Market value 100,831

Number of shares (in thousands) 8,266,184

Date of publication 26.02.2026

Juan valuation analysis (ultra-compact)

Juan pushes up his glasses, looks at the valuation line and grins:

"Rolls-Royce is expensive - but not too expensive for the story.

P/E ratio high, P/B ratio astronomical, but the market is clearly paying for the margin and FCF explosion.

PEG clean >1 again from 2027, so valuation runs into normality.

FCF yield increases every year, over 5% in 2028 - that is the real driver.

Dividend grows steadily, yield remains low, but cash power is the argument.

In short: premium multiple, but with a premium foundation. Not a bargain - a quality momentum play."

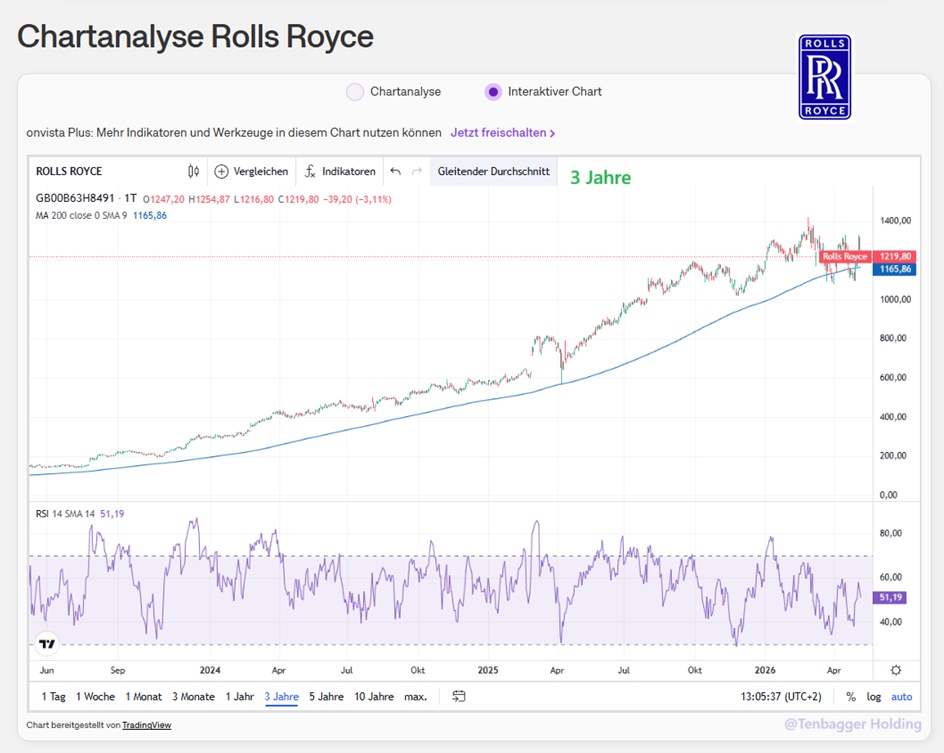

Performance:

1 week +1.72 %

1 month -4.55 %

6 months +7.14 %

1 year +56.63 %

3 years +707.01 %

5 years +1,042.78 %

Rolls Royce Holdings (ISIN GB00B63H8491): Several global supercycles are at work here. Rolls-Royce is transforming itself from a cyclical industrial company into a strategic infrastructure and technology provider. The share is on the verge of breaking out again. With a P/E ratio of 32, the share does not look cheap. But the chart looks all the better. I expect a sustained breakout movement.

PRICE: €14.11 (08.05.2026 at 22:00)