This is the third part of my series on stocks with a potential return of 20% per year.

In this series, I present companies that could achieve an annual return (CAGR) of 20% or more over the next few years.

In parts 1 and 2, we looked at software giants such as $CSU (-1,7 %) and $MSFT (-1,78 %) both relatively solid stocks with great potential. In Part 3, I would like to introduce you to Mastercard$MA (-0,89 %) in part 3.

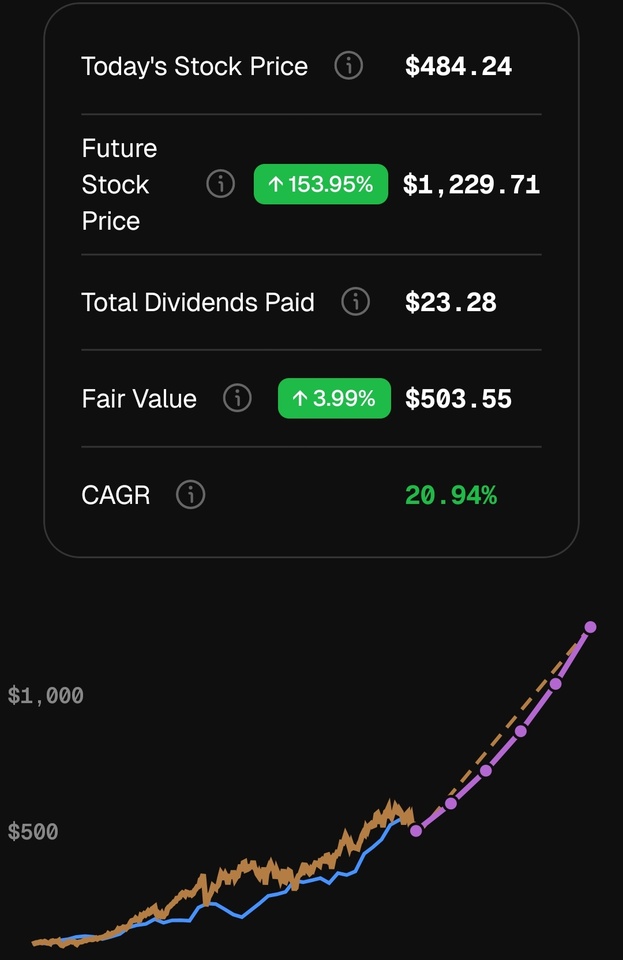

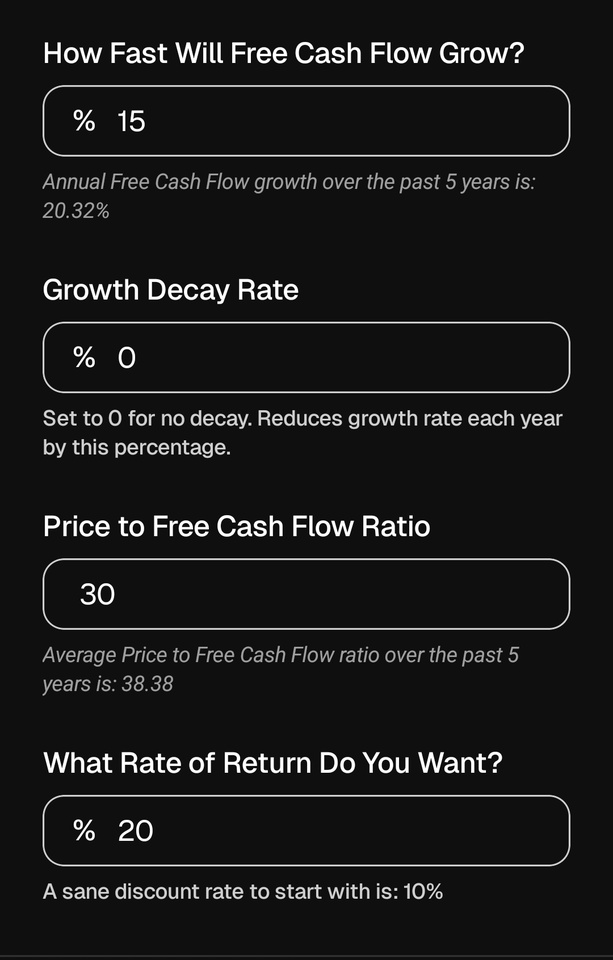

I use the StockUnlock tool for the valuation. I choose the most suitable ratio for each company; in the case of Mastercard, this is the P/FCF ratio (price/free cash flow ratio). With the conservative assumptions you can see in the picture, the model calculates an annual return of around 20% for the next five years.

Pros & cons: Mastercard (MA)

Mastercard is often regarded as a "quality stock" par excellence. In order to achieve a 20% CAGR, the interplay between earnings growth and valuation (multiple) must be right.

Opportunities:

The duopoly: Together with Visa, Mastercard dominates global payment transactions. The moat (network effect) is gigantic; it is almost impossible to displace this network.

High margins: Mastercard produces extremely high operating margins (often over 50%), as the infrastructure is already in place and every additional transaction is almost pure profit.

Scalability: The company benefits massively from the trend towards a cashless society, especially in emerging markets.

Return of capital: MA is known for aggressive share buybacks and steadily increasing dividends, which further drives earnings per share.

Risks

High valuation: Mastercard is rarely "cheap". A price/earnings ratio (P/E) or P/FCF in the 30 to 35 range is standard. If the market environment turns, this multiple could shrink (multiple compression), which would depress returns.

Regulation: Governments around the world (especially the EU and USA) regularly review fee structures. New laws to cap transaction fees could slow down growth.

Alternative payment systems: Cryptocurrencies, fintechs (such as Adyen or Stripe) or state-run instant payment systems (such as Pix in Brazil or FedNow in the USA) could compete for market share in the long term.

I own 42 shares in $MA (-0,89 %) .

And now it's your turn! Where do you see 20 carg? Extremely fear makes me personally extremely happy 😁 😁

I wish you all a wonderful weekend