Hello everyone,

I’ve been on my investment journey for just under 2.5 years now, and I’d be very interested in your critical feedback and opinions.

First, a quick introduction:

I’m 26 years old, work full-time in the steel industry, and my monthly savings amount is currently just under 560€ -> 150€ Nasdaq 100 / 150€ ACWI IMI / 100€ physical gold / 100€ Bitcoin / €60 in a mutual fund policy.

I hope to be able to increase these amounts back to 200/200/100/100/60 in the future.

My investment horizon is about 25–30 years, so that I can transition to part-time work in my mid-50s.

I also have a home savings contract with just under 7.5k, which I consider my emergency fund.

Now, about my investment portfolio:

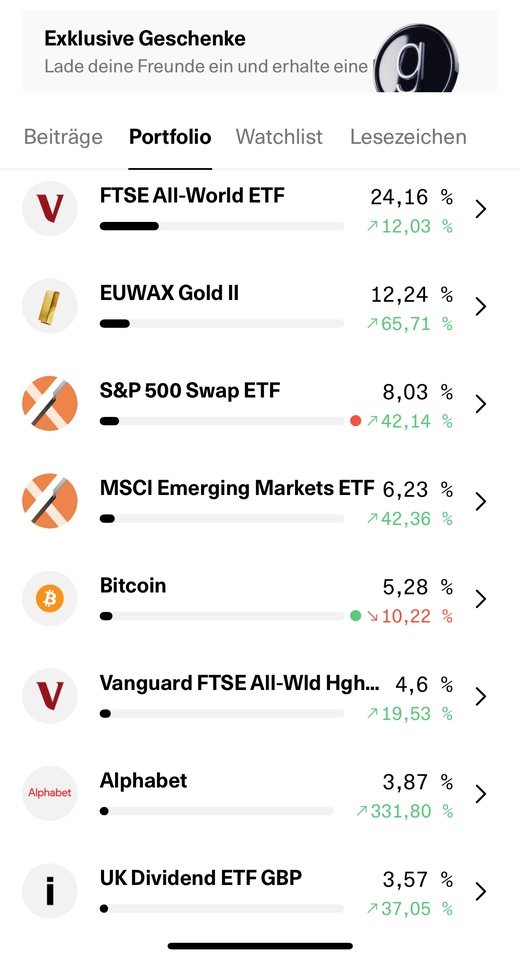

I have a mutual fund policy through HDI that includes the Vanguard FTSE All-World $VWCE (+0,03 %) , Vanguard FTSE Dev. Europe $VWCG (-0,13 %) , iShares Core S&P 500 $CSPX (+0,25 %) and Franklin FTSE MSCI India $FLXI (-0,48 %) . The weightings are 60/15/15/10.

In the future, I plan to simplify this and transfer everything into the FTSE All-World fund.

Basically, I’d like to keep the mutual fund policy because the contract dates back to before 2004, which means it’s tax-free.

I’m contributing about €60 per month with a 5% growth rate until the year 2045. The contract ends in 2069, when I turn 70. However, I can cancel the contract at any time and receive the money tax-free.

The rest of my portfolio consists of my core ETFs: the Xtrackers Nasdaq 100 $XNAS (-0,06 %) and the SPDR MSCI ACWI IMI $SPYI (+0,17 %) .

This is supplemented by just under 10% Bitcoin $BTC (-1,82 %) (Bitvavo) and 10% gold $EWG2 (+0,83 %) (the EUWAX isn’t eligible for a savings plan at ING, so I’ve started contributing to WisdomTree instead).

The rest consists of individual stocks, which I used to try to diversify and outperform the market. Unfortunately, that didn’t work at all, and I’ve realized that I lack the time and patience for individual stocks.

Ideas / Target Allocation:

I’d like to keep the portfolio leaner and more streamlined and sell off individual stocks in the near future. Parting with Novo, Nu, and Mastercard isn’t too difficult for me, but I really like Visa and Berkshire, as I’m convinced of their long-term quality.

My target allocation for the portfolio (excluding the fund policy) should therefore look as follows:

35% Nasdaq 100 -> alt. 40%

35% ACWI IMI -> alt. 40%

10% individual stocks -> alt. 0%

10% Bitcoin

10% gold

I’d be interested in your opinions and constructive feedback regarding the portfolio and the allocation. Should I perhaps avoid individual stocks altogether? Is it even a good idea to invest in gold at age 26? With this allocation, does it make sense to also invest in Epi’s Wikifolio $DE000LS9U6W1 (-0,07 %) as well?

Thank you all in advance, and I wish you a relaxing Friday and a pleasant weekend!

Best regards,

The Blonde Investor