Global X NASDAQ 100 Covered Call ETF

Price

Debate sobre QYLE

Puestos

62

Regrouping

As I had already planned this morning, I have parted with the $QYLE (-0,01 %) and bought the $WINC (+0,06 %) and bought the I also took the opportunity to get rid of the $JEGP (-0,44 %) which performed even worse than the Global x for me. Overall, I came out of both with a red zero.

In addition to the ishares, 50 of the proceeds from the $ASWM (-1,11 %) went into the portfolio, of which I now have 100.

In the high yield area, I then added the $TDIV (-0,52 %) as the largest position and the $YYYY (-0,59 %) the $JEPQ (+0,25 %) and the $SXYD (+0 %) .

That's how it's going to stay for now; in total, that's around 8-9% of the total portfolio in this area.

As I bought the Winc before the ex-date, but sold the global x afterwards, I can still take the dividends from both this month. As a result, I even have a small gain on the global x overall.

Regrouping

Hello, I have been holding the $QYLE (-0,01 %) . overall, i.e. with dividends, I am currently at about plus minus zero. However, as the ETF has shown in the past that it does not recover from corrections such as Liberation Day, I fear that it will be the same next time.

I am therefore considering switching to the $WINC (+0,06 %) as a cash flow alternative, as it obviously pursues a better strategy due to its active approach. What do you think? And do you have any other suggestions that I may not have on my radar?

Either way, the whole thing would only be an addition of around one percent of the overall portfolio.

Dividendenopi inside (Part 1 )..... Dividendenopi Rewind2025

A little later, but not too late, I'll also have my say at the end of the year, together with an insight into the goings-on of the Opi before @Tenbagger2024 , @SAUgut777 and some others get impatient, as you know, old people are a bit slower. I would also like to take this opportunity to thank and appreciate all those who contribute here on GQ with great analyses and strong contributions, critical comments and a wonderful exchange. I'm deliberately not naming any individuals now, otherwise I won't be able to finish. All of you together are great, whether you're a veteran or a newcomer. The community is alive and I am happy to be a part of it. Thanks also to @christian and the Getquin team, who make this possible by maintaining the platform, even if things sometimes don't run smoothly. The Bavarian says: Basst scho

The year 2025 was exciting and, from my point of view, successful in terms of my expectations. If you don't feel like evaluating a boring dividend strategy, don't want to read about overnight and fixed-term deposits, aren't interested in certificates and don't like the Sparkasse, you are welcome to leave here after Rewind 2025. Many thanks to everyone else for reading and, if necessary, commenting.

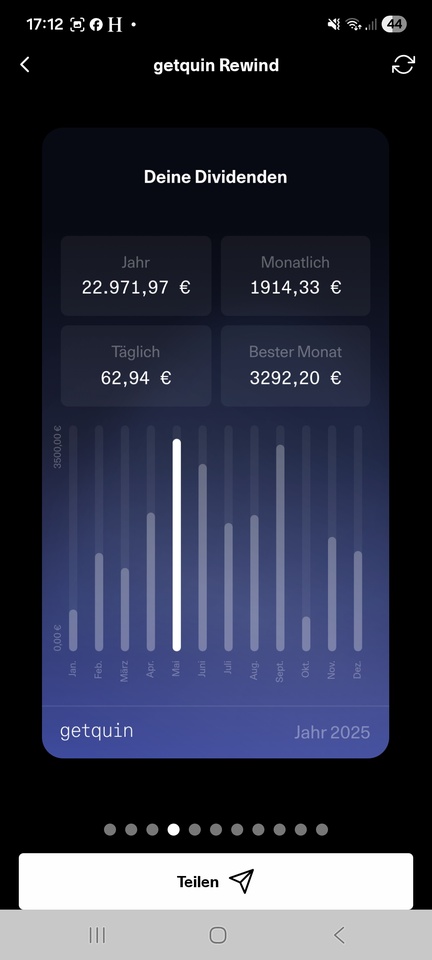

At least as far as the majority of shares are concerned, I am known to be invested in dividend stocks in order to generate the highest possible cash flow. I am now almost 62 years old and do not value excessive performance but would like to make a living from the income from my assets and decided to stop working at the beginning of the year when the company where I was employed was dissolved. I see myself as a buy and hold a while. Nothing lasts forever, especially with high-dividend shares. There are regular reallocations without getting into an operational frenzy. In 2025, for example $TRMD A (+0,69 %) and a large position $HAUTO (+0,66 %) had to leave the portfolio, the high dividend expectations were significantly reduced. The $QYLE (-0,01 %) has not recovered from April, $EQNR (+1,24 %) and $VICI (+0,33 %) led to the brink of capital loss despite respectable dividends and had to give way, as did $MUX (-0,28 %) with its inconsistencies. New additions were $NN (+0,26 %) , $PFE (+0,86 %) , $DTE (-0,46 %) and a first position at the end of the year $ARCC (-0,34 %) You can see the composition in my profile. I generally try to limit myself to +/- 20 positions and weight them according to purchase. A maximum of 20k per position is invested. This results in the calculation of my dividends and expected income. In its current composition, the portfolio shown here has a value of just over € 340,000 as at 31.12.2025 and has generated gross dividends of just under € 23,000 this year. This corresponds to a dividend yield of 6.73%

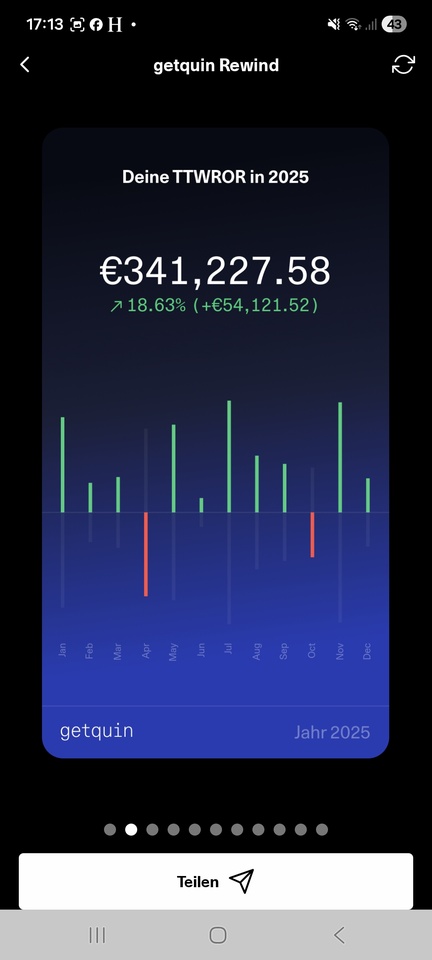

The time-weighted yield was 18.63% and therefore well above average, at least better than 67% of the getquin community. I wasn't able to beat the DAX, but at least I outperformed the S&P500 and beat the relevant MSCI World index by some distance. Even on a 5-year view I am on a par. Tobacco stocks did very well $BATS (-1,11 %) , $IMB (+0,62 %) and $MO (+0,25 %) , $HSBA (+0,29 %) , and $RIO (+0,07 %) and of course $965515 (-1,42 %) that I physically hold and the $EWG2 (-1,49 %) .

That's all there is to the part of my investments shown here in GQ. What follows is a piece of my life story and the first part inside Dividendenopi.

As I said, I now live off my assets. This amounts to just under € 1.2 million in all the forms of investment I hold. Is that enough for a carefree life? For me in any case. Because on top of that, I have a debt-free, owner-occupied property (a single-family home with a large garden in a quiet rural location near a city of 600,000 inhabitants) and a rented two-family home, appropriately enough, as a neighboring property. Partly financed, rent surplus after installment to the bank a good € 700 per month, flows completely into the maintenance reserve. Claims from BAV, life insurance, building society savings contracts will be added on top in the next few years, but are not taken into account here. There's even a savings account with €18,000..... half of which belongs to my wife and she doesn't want to close it.

My wife (still) works and has a decent income despite working part-time and has other liquid assets in the lower six-figure range. She does it herself, the stock market is the devil's work. Her story is not included here either.

So I / we are doing pretty well after all. It wasn't always like that, anyone who is or was self-employed knows that. But consistent financial planning is important, no matter what the situation, as is sticking to your savings rate. I started investing in real estate at the beginning of the 1990s and have been liquidating it over the last few years. In conjunction with my own wealth accumulation and an inheritance, I am now in a comfortable situation for me.

What do I do with the rest of the money outside the getquin portfolio? A good € 500,000 is (still) in call money and fixed-term deposit accounts. Interest rate hopping on call money and fixed-term deposits from 2 years ago yields around 3% on call money and over 4% on fixed-term deposits. The remaining capital is invested in certificates. Mainly in fixed-coupon express certificates with quarterly payout and partly in bonus certificates with CAP and barrier.

My investments currently generate a net monthly cash flow of € 4000, which is enough for me to live on. Plus € 800 ALG on top until the beginning of 2027.... But before the company closed, I only worked 16.5 hours a week. With my wife's income, that's a good €6500, which is bearable. You can certainly do more with your assets, depending on your needs. We live rather modestly, don't have any children and aren't the consumer type.

How am I invested outside of dividends, why certificates and which broker, where and how overnight and fixed-term deposits? I thought that would go beyond the scope of this article, so I'll come back to it in a second part. Thanks for your participation so far and see you soon

Significantly, you can see here that not having children is now the best provision for old age. Not an accusation, just an observation. 🤷♂️

Strategy presentation, feedback welcome

Hello everyone,

I have been following this forum for some time now and have decided to present my experiments and current strategies.

On the one hand, because I want to avoid losing track of things, and on the other hand, to prepare my thoughts for myself and also to get other perspectives and opinions.

Briefly about myself

I am 22 years old and graduated last year with a Bachelor of Engineering in Energy Technology.

I am currently working in a medium-sized company in the energy industry in Germany.

I have been rather frugal with money since I was a child. As I got older, my interest in increasing money wisely grew.

I was also lucky that my uncle opened a junior custody account for me when I was born. As a result, at the age of 18 I already had a small starting portfolio worth around 3,000 euros.

At the beginning, I focused intensively on precious metals and also invested in them. I don't plan to touch these holdings in the long term. If I don't need them, I see them more as a legacy for the next generation. I will buy more from time to time.

Basic start

As a first step, and I am aware that this will be assessed differently, I have taken out a unit-linked pension plan with the savings bank, which I save 150 euros per month.

I also took out a building society savings plan, as I basically want to buy my own home in the long term. I am currently renting.

The building society saver is also 150 euros per month per month.

At the same time, I have been working with neobrokers, from which my current portfolio has gradually developed.

Yes, there are still quite a few stocks in it at the moment. I will probably clean that up in the long term.

1st approach, accumulating ETFs

My first approach was to invest in classic accumulating ETFs.

- World, $XDWD (+0,6 %)

- Emerging markets, $EIMI (+0,86 %)

- AI and big data, $XAIX (+1,68 %)

Smaller side bets were added later.

- Armaments, $DFEN (+0,23 %)

- uranium, $U3O8 (-0,41 %)

- batteries, $BATG (+0,24 %)

I also bought my first individual shares to gain experience. Among other things, I had success with $RHM (-0,27 %) . At the same time, I learned how quickly losses can occur if you are not sufficiently diversified, for example with $ABR (-0,6 %) ,$1SXP (+0,57 %) and other stocks.

This ultimately led me to my second approach.

2nd approach, dividend strategy

As I already have a pension plan through LBS and don't want to be the richest man in the cemetery, I focused more on a dividend strategy.

The first attempt consisted of the following combination

The idea came from a business magazine and was aimed at making monthly distributions as even as possible. I also added $QYLE (-0,01 %) to gain initial experience with option strategies.

However, as this combination is only diversified to a limited extent and I deliberately wanted to move away from the USA, I adapted my strategy further.

Current strategy

Fixed savings rates

- LBS, retirement provision, 150 euros per month

- Building society, residual debt for future home ownership, 150 euros per month

Dividend strategy with 115.24 euros per month

- $XDWL (+0,41 %) , 34 percent

- $IEEM (+1,29 %) , 26 percent

- $XAIX (+1,68 %) , 13 percent

- $EXSH (+0,49 %) , 26 percent

Side bets with 81 euros per month

- $DFEN (+0,23 %) , 62 percent

- $BATG (+0,24 %) , 10 percent

- $QYLE (-0,01 %) , 25 percent

Trading 212 experiment with 100 euros per month

Here I am pursuing the goal of bundling individual shares in a common pot, partially saving them and automatically reinvesting distributions in order to benefit from the compound interest effect in the long term.

I welcome tips and constructive criticism so that I can continue to improve my strategy.

Best regards

Mister Kimo

Perhaps it would make sense to think about liquidating all small positions (for example < 1%) and investing in a closed position

In itself, however, there is little wrong with the individual positions

Why covered call ETF strategies are not an income and are bad for wealth accumulation.

ETFs that partly implement a CC strategy also underperform the market over the long term.

$QYLE (-0,01 %)

$JEPI (+0,25 %)

$JEGP (-0,44 %)

$JEPQ (+0,25 %)

$WINC (+0,06 %)

$IE000MMRLY96 (-0,59 %)

It’s kind of like the dividend vs. accumulating ETF debate. What most people forget to mention, though, is opportunity cost.

If you get monthly payouts, no one says you have to reinvest them in the same stock or ETF. You can put that money anywhere you see potential. Every payout gives you a choice.

Most people are probably better off just buying a global accumulating ETF and forgetting about it. But for me, parking money in JEPG makes more sense than leaving it in bonds or uninvested cash.

Sure, I could use IWDA, but then I’d have to realize losses instead of just seeing smaller monthly payouts. Plus, trading costs make it pointless as a “parking” option, at least for me with my small portfolio. Long term, you should stay invested — but monthly income let me stay flexible and jump on new ideas when I want.

I’m not trying to beat the S&P with JEPG. I just like having the freedom to invest when opportunities pop up.

In my view, JEPG should be compared to bonds or to not investing at all. The key is to understand the risk: during a market downturn, you’ll likely have less available capital with JEPG. You just need to decide whether that tradeoff works for you.

Beware of private equity funds at Trade Republic 🔍

Underperformance 😑

- PE funds usually underperform the NASDAQ 100 over 5 and 10 years.

- The stated target return of 12% p.a. is wishful thinking for advertising purposes.

Extremely high costs 💰

- 2.35% p.a. EQT + 5.00% exit costs

- 4.51% p.a. Apollo

- Comparison: iShares NASDAQ 100 ETF only 0.32% p.a.

- PE fund is up to 23 times (!!!) as expensive and eats up returns like Jumbo Schreiner at the All You Can Eat buffet.

Low liquidity 🤏

- Monthly sale possible, but no buyers guaranteed

- Sale can be prohibited if too many want to sell. You then have to keep the dirt because it is not traded on the stock exchange.

Further risks 🫣

- Apollo is not transparent and does not tell you what is in the fund. You should blindly & naively buy a fortune cookie.

Conclusion 🥱

Hands off. There are many better investments.

#traderepublic

#scalable

#privateequity

#fonds

#etf

#etfs

#nasdaq

#nasdaq100

$UST (+0,81 %)

$CSNDX (+0,79 %)

$EQQQ (+0,91 %)

$QYLE (-0,01 %)

#fail

If the returns were as high as promised and the vola so much lower, then this should be reflected in the share prices of listed PE companies, among other things 🧐

Strangely enough, it doesn't 😅

I love distributing ETFs, which ones should I have?

What are your tips for a nice dividend portfolio or your favorite distributing ETFs? At the moment I have $JEGP (-0,44 %) , $MAIN (+0,08 %) and $EQDS (-0,36 %) ? $QYLE (-0,01 %) I have recently thrown out , it was only running crosswise.

Honest opinion!

Hello lovelies!

I've been reading here for a long time now and have given it a lot of thought!

I started "investing" in mid-November (I just bought something or listened to someone who posted something somewhere). So by my standards, I've paid quite a bit of learning money.

Then I started paying into individual shares and ETFs with savings plans, which was only partially thought through.

Now I've got rid of pretty much everything and have drawn up a very detailed plan with goals, milestones and when to pay in what.

Individual items, such as $MO (+0,25 %) , $O (-0,72 %) and $ATO (+0,75 %) I still have in my portfolio, but I will part with them at a time that suits me.

I am now 21 years old and will start studying dual tax law in September.

This will earn me some money and I still have a part-time job.

My plan is to invest €500 a month in a savings plan.

iShares Core MSCI World (Acc)$IWDA (+0,4 %)

170€

Nasdaq 100 Covered Call (Dist)$QYLE (-0,01 %)

85 €

S&P Global Dividend Aristocrats (Dist)$ZPRG (-0,94 %)

80 €

Vanguard FTSE All-World High Div (Dist)$VHYL (-0,31 %)

65 €

iShares Nasdaq 100 (Acc)$CSNDX (+0,79 %)

50 €

FTSE Emerging Markets (Dist)$VFEM (+1,17 %)

50 €

As my salary will increase over the course of my studies and afterwards, I would like to increase my monthly savings installment by €50 each year. In addition, there will be an extra €2000 minimum per year and larger payments in individual years, such as my savings account in 2037, which will then be finished.

I also considered ETFs. I now have a mixture of distributing and accumulating. I am well aware that it would be better to only save in accumulating ETFs. However, I think it's more motivating and easier for me to receive the dividends and to realize that something is happening and I'm getting something. I will reinvest the dividends. I just don't know exactly how yet.

I'm currently considering whether I want to invest some of it or additionally in $BTC (-2,84 %) preferably with a savings plan (or maybe another platform where it's really Bitcoin).

If I do everything exactly as planned and achieve an average annual return of 7%, I will theoretically be able to live with 45/50 of it. According to my plan now, I would like to start shifting to purely distributing at 40/45 and save a little more depending on my life situation.

This would cap my pension and I would have something I could pass on to my children to give them some security.

You never know what life will bring. Maybe I'll manage to save more sooner or have setbacks and not make it according to plan, but I've made the plan with savings rates... rather pessimistic and hope that I can exceed my annual goals.

I look forward to hearing what you think about this.

Stick to 3 ETFs! Leave individual stocks.

And very important: look at the total return on justetf. Dividends are useless if you perform poorly overall (see Realty Income or Cola).

And it's best never to sell Bitcoin and if never during the year. And don't buy from TR, as you can't send the coins. Buy from Bitvavo.

Once again...

It has a lower TER, is not synthetic and applies its option strategy to only 80% of the portfolio, which protects the intrinsic value much better from the high payout in the long term. It also allows you to ride the upward phase a little better. The last few weeks have clearly shown this.