What do you think of SMC, get out or stay?

Debate sobre SMCI

Puestos

67

1Semana·

Welcome to the club

$SMCI (-9,91 %) a cyclical stock with AI opportunities

RSI (14) is around 50-55 - indicating neither overbought nor oversold conditions.

The same chart pattern is forming as for Tesla. Symmetrical triangle 🚀

1010

4 Comentarios

1Semana

Symmetrical triangle: the price can also break out to the downside. That's why I would have waited for at least the breakout

••

3Semana·

After the Oracle rally: you need to know these cloud favorites

Hello dear Getquin Community,

After $ORCL (-3,03 %) Oracle caused quite a stir after the last quarterly figures and the market reacted extremely positively with a 40 percent increase in the share price, so much so that CEO Larry Ellison briefly became the richest person in the world overnight, I wanted to unravel the magic and find out exactly which division caused this tremor.

The answer is Cloud Infrastructure, or OCI for short. In this area, the demand for data centers for artificial intelligence has exploded, which has brought Oracle long-term orders worth 455 billion US dollars. However, it is not only Oracle that is benefiting, but also other hyperscalers, regional challengers and, above all, the so-called shovel manufacturers that provide the basic infrastructure.

I have taken the trouble to look for potential competitors and up-and-coming challengers so that you have a complete overview of this sector. I have divided the whole thing into the following segments: 🌍 Big players (hyperscalers), 💡 Hidden champions (selection by region), ⚒️ Shovel manufacturers (infrastructure suppliers) and, as always, my favorite.

If I have overlooked any important aspects or a classification was not entirely precise, I look forward to your comments and exciting additions. Together we can understand this topic even better and learn from each other.

Feel free to leave a 👍. I wish you every success with your investments 🚀

🌍 Big Player (Hyperscaler)

Amazon Web Services - $AMZN (-5,92 %) (USA, Nasdaq) → World market leader with >30 % market share, huge data centers & own AI chips (Trainium, Inferentia)

Microsoft Azure - $MSFT (-3,3 %) (USA, Nasdaq) → second largest provider, strong AI focus through OpenAI partnership

Google Cloud - $GOOGL (-3,4 %) (USA, Nasdaq) → third largest provider, specialized in AI workloads & big data

Oracle Cloud Infrastructure (OCI) - $ORCL (-3,03 %) (USA, NYSE) → Number 4 worldwide, currently fastest growth (+70-80 %), RPO USD 455 bn

Alibaba Cloud - $BABA (-8,67 %) , $9988 (-8,32 %) (China, NYSE/HKEX) → Market leader in Asia, complete cloud suite from IaaS to AI

Favorite: Oracle - $ORCL (-3,03 %)

Oracle impresses with its cloud infrastructure OCI, which recently collected orders worth 455 billion US dollars. The moat lies in the close integration of the database business and cloud services as well as the multi-cloud partnerships with Microsoft and Google. The compounder property is the result of long-term contracts and economies of scale in data center construction.

Alternative favorite: Alibaba Cloud - $BABA (-8,67 %) , $9988 (-8,32 %)

Alibaba is number one in Asia and number four worldwide. The moat lies in the close integration with Alibaba's e-commerce and fintech ecosystem. The compounder property stems from the enormous growth in emerging markets and the increasing demand for cloud services in China. While the stock is valued significantly cheaper than Oracle, there are geopolitical and regulatory risks.

💡 Hidden champions (selection by region)

🇪🇺 Europe

OVHcloud - $OVH (-2,16 %) PA (France) → largest European cloud provider, GDPR- and Gaia-X-focused

Scaleway - private (France, part of the Iliad Group) → Developer and AI cloud platform

T-Systems - part of $DTE (+0,17 %) DE (Deutsche Telekom, Germany) → Hybrid & Sovereign Cloud for Public Sector

IONOS - $IOS (-3,84 %) DE (Germany, Xetra)

Largest European web hosting and SME cloud provider. Burggraben: strong brand and high customer loyalty in the SME sector.

Aruba Cloud - private (Italy) → regionally strong in SMEs & hosting

Outscale - private (France, subsidiary of Dassault $DSY.PA) → Industrial Cloud & Simulation

Favorite: OVHcloud - $OVH (-2,16 %)

Burggraben: strong position as a GDPR-compliant sovereign cloud with Gaia-X. Compounder: increasing trust from authorities and companies ensures growing recurring revenues.

🇨🇳 China

Baidu AI Cloud - part of $BIDU (-8,38 %) , $9888 (-8,29 %) (Nasdaq, China/USA) → AI workloads, autonomous driving, language models

JD Cloud - part of $JD (-6,72 %) , $9618 (-5,5 %) (Nasdaq, China/USA) → Cloud for e-commerce & retail

Kingsoft Cloud - $KC (-11,43 %) , $3896 (-9,48 %) (Nasdaq, China/USA) → Gaming, streaming and app cloud

China Telecom Cloud - part of $728 HK (HKEX) → Infrastructure cloud, state-supported

China Mobile Cloud - part of $941 HK (HKEX) → 5G edge cloud with telecom backbone

Favorite: Kingsoft Cloud - $KC (-11,43 %) , $3896 (-9,48 %)

Moat: Specializing in gaming, streaming and mobile apps with deep integrations into ecosystems. Compounder: benefits from China's growing online consumption and strong embedding in the Tencent environment.

🇯🇵 Japan

NTT Communications - part of $9432 (-1,09 %) T (Tokyo) → Enterprise cloud with global network

NEC Cloud - $6701 (-6,47 %) T (Tokyo) → Government & security solutions

Fujitsu Cloud K5 - $6702 (-5,49 %) T (Tokyo) → Hybrid cloud for large companies

Rakuten Symphony Cloud - part of $4755 (+0,59 %) T (Tokyo) → 5G & telecom cloud

IIJ Cloud - $3774 (-2,71 %) T (Tokyo) → Cloud pioneer for enterprise IT

Favorite: NTT - $9432 (-1,09 %)

Moat: global telecom backbone and huge enterprise customer base. Compounder: expansion of data centers in Asia and Europe with stable recurring revenues.

🇮🇳 India

Reliance Jio Cloud - part of $RELIANCE NS (NSE India) → Telecom Cloud, partnership with Azure

Tata Communications IZO - $TATACOMM NS (NSE India) → Hybrid cloud & global backbone

Infosys Cobalt - $INFY (NYSE/NSE India) → Cloud migration platform & consulting

HCLTech Cloud - $HCLTECH NS (NSE India) → AI-powered hybrid cloud

Wipro Cloud Studio - $WIPRO NS (NSE India) → MultiCloud service provider

Favorite: Tata Communications - $TATACOMM

Moat: global fiber optic network and deep networking in hybrid cloud. Compounder: growing international expansion and increasing demand for multi-cloud solutions.

🌏 Asia / Oceania

Naver Cloud - part of $035420 KQ (Korea KOSDAQ) → AI & gaming cloud

Samsung SDS Cloud - $018260 , $SMSN (-4,06 %) KQ (Korea KOSDAQ) → Enterprise & IoT Cloud

KT Cloud - part of $030200 KQ (Korea KOSDAQ) → Telecom & Edge Cloud with 5G

Telstra Cloud - $TLS (-0,86 %) AX (Australia) → Telecom Cloud, Asia-Pacific focus

Macquarie Telecom Cloud - $MAQ AX (Australia) → Public Sector & Compliance

Favorite: Naver Cloud - $035420

Moat: strong integration of AI and gaming in Korea. Compounder: rapid scaling due to growing demand for AI and ML applications.

🌍 Latin America

UOL Diveo (Compasso UOL) - private (Brazil) → Cloud + Managed Services

Tivit Cloud - private (Brazil) → MultiCloud for industry & banks

Locaweb Cloud - $LWSA3 SA (Brazil) → SME Hosting & Cloud

Claro Cloud - part of $AMX (-0,27 %) (Mexico, NYSE/HKEX) → Telecom Cloud in Latin America

DesireCloud - private (Chile/Peru) → Local provider for companies

Favorite: Locaweb - $LWSA3

moat: Market leader for SME cloud and hosting in Brazil. Compounder: enormous scalability through the digitalization of small and medium-sized enterprises throughout Latin America.

🇨🇦 Canada

OVHcloud Canada - part of $OVH (-2,16 %) PA (France) → Data centers for North America

SherWeb - private (Quebec) → Cloud and MSP services for SMEs

HostPapa - private (Canada) → SME cloud solutions

Canadian Web Hosting - private (Canada) → Cloud & hosting with a focus on data protection

Beanfield Cloud - private (Toronto) → Cloud combined with fiber optic infrastructure

Favorite: SherWeb - private

Moat: close ties to SMEs via managed services. Compounder: fast-growing cloud ecosystem for small businesses in North America, high customer loyalty.

⚒️ Blade manufacturers (infrastructure suppliers)

🖥️ Semiconductors & Chips

Nvidia - $NVDA (-6,14 %) (USA, Nasdaq) → GPUs for AI training & cloud

AMD - $AMD (-10,01 %) (USA, Nasdaq) → CPUs/GPUs for Data Center

Intel - $INTC (-5,15 %) (USA, Nasdaq) → Server CPUs & AI accelerators (Gaudi)

TSMC - $TSM (-6,55 %) (Taiwan, NYSE/TWSE) → largest chip manufacturer, produces for NVIDIA/AMD

Samsung Electronics - $SMSN (-4,06 %) KQ (Korea) → Memory, foundry, GPUs/CPUs

Favorite: Nvidia - $NVDA (-6,14 %)

Moat: near monopoly in high-end GPUs for AI. Compounder: Ecosystem and network effects through CUDA and developer community.

📦 Data center hardware & servers

Supermicro - $SMCI (-9,91 %) (USA, Nasdaq) → GPU clusters & AI servers

Dell Technologies - $DELL (-4,8 %) (USA, NYSE) → Enterprise Servers & Storage

Hewlett Packard Enterprise - $HPE (-7,48 %) (USA, NYSE) → Hybrid Cloud & Edge

Inspur - private (China) → AI & Cloud Server

Lenovo - $LNVGY (-5,78 %) (China/ADR) → HPC and AI servers

Favorite: Supermicro - $SMCI (-9,91 %)

Moat: Specialization in GPU clusters and AI servers. Compounder: benefits from every expansion of the hyperscalers, extremely high scalability.

⚡ Memory & network chips

Micron - $MU (-6,96 %) (USA, Nasdaq) → DRAM & HBM memory

SK Hynix - $HY9H (-4,16 %) KQ (Korea) → Memory chips, HBM for NVIDIA

Broadcom - $AVGO (-7,17 %) (USA, Nasdaq) → Network Chips & Switches

Marvell - $MRVL (-5,93 %) (USA, Nasdaq) → Network & 5G chips

ASE Technology - $ASX (-5,41 %) (Taiwan, NYSE) → Packaging for high-end chips

Favorite: Broadcom - $AVGO (-7,17 %)

Moat: deep roots in network infrastructure of hyperscalers. Compounder: benefits from rising demand for switches and custom chips for the cloud.

🏭 Data centers / colocation

Equinix - $EQIX (-1,43 %) (USA, Nasdaq) → largest colocation provider worldwide

Digital Realty - $DLR (-3,41 %) (USA, NYSE) → Data centers worldwide, strong in Europe/USA

China Telecom DC - part of $728 HK (HKEX) → Data center infrastructure in China

NTT Data Centers - part of $9432 (-1,09 %) T (Tokyo) → Data centers in Asia/Europe

NEXTDC - $NXT (-0,82 %) AX (Australia) → Growing data centers in the APAC region

Favorite: Equinix - $EQIX (-1,43 %)

Moat: global networking and extremely high switching costs for customers. Compounder: continuous expansion and cross-selling potential through platform structure.

🔋 Energy & cooling

Schneider Electric - $SU (-2,76 %) PA (France, Euronext) → Power & Cooling for Data Center

ABB - $ABBN (-0,59 %) (Switzerland, SIX/NYSE ADR) → Energy & Automation

Siemens Energy - $ENR (-3,54 %) (Germany, Xetra) → Power Grids & Data Center Technology

Vertiv - $VRT (-6,22 %) (USA, NYSE) → Cooling, Racks & UPSs

Eaton - $ETN (-2,61 %) (Ireland/USA, NYSE) → Power Management

Favorite: Schneider Electric - $SU (-2,76 %)

Burggraben: market-leading energy and cooling systems for data centers. Compounder: long-term growth due to increasing demand for efficient data centers.

🌐 Network & Connectivity

Cisco - $CSCO (-3,83 %) (USA, Nasdaq) → Router & Network Hardware

Arista Networks - $ANET (-4,24 %) (USA, NYSE) → High-speed switches for hyperscalers

Juniper Networks - Acquisition by $HPE (-7,48 %) Hewlett Packard HP (USA, NYSE) → Routing & Network Security

Ciena - $CIEN (-5,18 %) (USA, NYSE) → Fiber Optics & Optical Networks

Nokia - $NOK (+2,68 %) (Finland, NYSE/Helsinki) → 5G & Core Networks

Favorite: Arista Networks - $ANET (-4,24 %)

Moat: technological leadership in high-speed switches in hyperscaler data centers. Compounder: enormous growth opportunities due to exponential data traffic in AI workloads.

✨ Takeaway

The Oracle quake shows: Cloud & AI are the growth drivers of the coming years. While hyperscalers are in the spotlight, hidden champions are growing in their niches in the background and blade manufacturers are making money from every expansion of the infrastructure.

👉 Question for you: Do you prefer to focus on hyperscalers in your strategy? hyperscalersthe hidden champions or directly on the shovel manufacturers?

I look forward to your opinions!

Source: own analysis

Image - Image credit: Getty Images

6464

21 Comentarios

3Semana

So many interesting suggestions 👍🏼

•

77

•

1Lun·

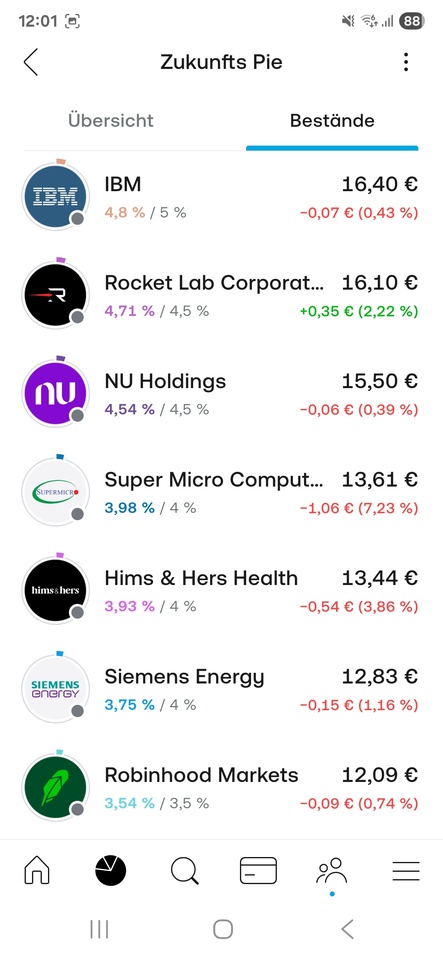

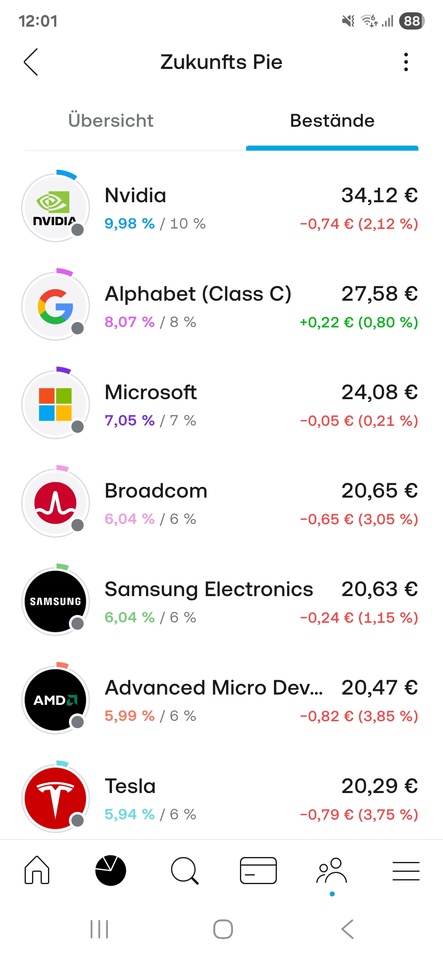

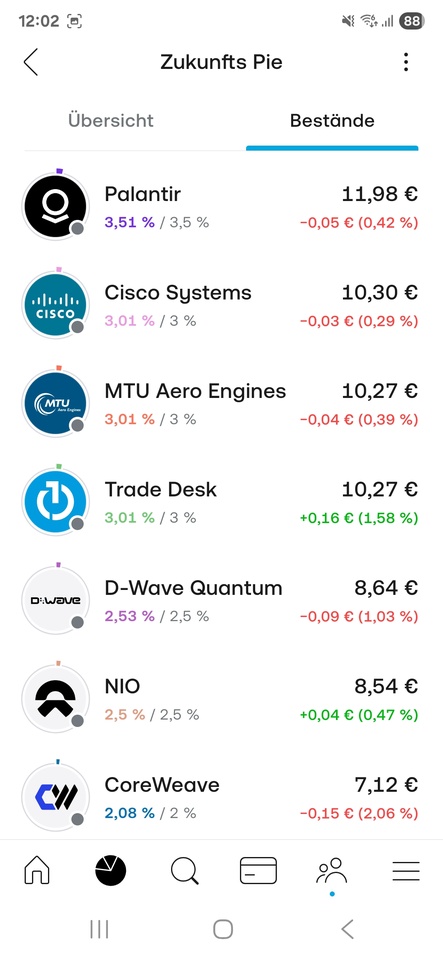

Once again 212

So 1.5 weeks have now passed. The first gimmicks are over and my Watchlist Pie has returned a total of 4.5% in one week. This has now been sold and I have built up a pie to save for the next 8-10 years. I'm starting with 50€ a week until I've completed the broker's test phase. After that I'll ramp it up to about 1k per month.

There are still a few stocks missing, but the big ones will be scaled down a bit. Among others $IREN (-9,15 %) ....

What do you think of the selection?

$NVDA (-6,14 %)

$GOOGL (-3,4 %)

$MSFT (-3,3 %)

$AVGO (-7,17 %)

$005930

$AMD (-10,01 %)

$TSLA (-6,86 %)

$IBM (-4,51 %)

$RKLB (-6,93 %)

$NU (-3,45 %)

$SMCI (-9,91 %)

$HIMS (-8,47 %)

$ENR (-3,54 %)

$HOOD (-9,88 %)

$PLTR (-7,09 %)

$CSCO (-3,83 %)

$MTX (-2,98 %)

$TTD (-5,03 %)

$QBTS (-7,49 %)

$9866 (-9,66 %)

$CRWV (-5,69 %)

And what of course should not be missing is $SIKA (+0,11 %) These are still weighted at 2% 😉 As a craftsman, I really enjoy using the products myself. The technological progress compared to other products such as StoCretec or others is already enormous, but it would go beyond the scope of this article.

2020

40 Comentarios

I definitely see IBM in a positive light! Most of the others too. As a student, I have a similar choice - but only €25 a week for now ^^

However, I see Tesla as doomed🙈🫡

Nevertheless, I wish everyone (who doesn't push Tesla as the most valuable company in the world) good luck :)

However, I see Tesla as doomed🙈🫡

Nevertheless, I wish everyone (who doesn't push Tesla as the most valuable company in the world) good luck :)

•

44

•1Lun·

Megatrend robotics, freshly updated, added value guaranteed!

After my first post on humanoid robots received a lot of positive feedback, I went into more detail. I have subsequently added my favorites in each sector.

Extended analysis of the value chain including shovel manufacturers and potential hidden champions

New categorySecondary key sectors (sales, marketing, financing)

In additionTop 25 companies worldwide, as well as Top 10 Europe and Top 10 Asia

I have also added a video link for beginners. This will give you an idea of how far the development of humanoid robotics has already progressed.

Thank you for your attention and your support 🙏

🌐 1. value chain of humanoid robots (with hidden champions)

1. research & chip design

$ARM (-10,82 %) ARM (UK) - CPU-IP, energy-efficient processors

$SNPS (-12,42 %) Synopsys (US) - EDA software, chip design

$CDNS (-9,81 %) Cadence (US) - EDA & Simulation

$PTC PTC (US) - Engineering Software, CAD/PLM

$DSY (-2,25 %) Dassault Systèmes (FR) - 3D Design & Digital Twin

$SIE (-2,34 %) Siemens (DE) - Industrial Software & Lifecycle Mgmt

$ADBE (-3,29 %) Adobe (US) - Design, AR/UX

ANSYS (US) - multiphysical simulation - acquisition by Synopsis

Altair (US) - CAE, simulation, digital twin - acquisition by Siemens

$HXGBY (-2,42 %)

Hexagon (SE) - Metrology & Simulation

$AWE (-2,82 %) Alphawave IP Group (UK) - High-speed chip IP for AI/robotics

1.Synopsis, 2.Siemens and 3.Adobe are my top 3 in this sector

2. manufacturing technology & equipment

$ASML (-5,06 %) ASML (NL) - Lithography (EUV)

$AMAT (-6,65 %) Applied Materials (US) - Semiconductor equipment

$8035 (-7,11 %) Tokyo Electron (JP) - wafer fabrication

$KEYS (-7,24 %) Keysight Technologies (US) - Metrology

$6857 (-6,61 %) Advantest (JP) - Chip test systems

$TER (-9,45 %) Teradyne (US) - test systems + cobots

$6954 (-1,33 %) Fanuc (JP) - Industrial robots, CNC

$CAT (-2,48 %) Caterpillar (US) - autonomous machines

$KU2G KUKA (DE) - industrial robots

Comau (IT) - automation - not listed on the stock exchange

$ROK (-3,15 %) Rockwell Automation (US) - industrial automation

$JBL (-5,69 %) Jabil (US) - contract manufacturing (EMS/ODM)

$KIT (+2,23 %) Kitron (NO) - European EMS/ODM manufacturer

$AIXA (-7,29 %) Aixtron (DE) - deposition equipment for compound semiconductors

$LRCX (-8,15 %)

Lam Research (US) - Etch/deposition systems

$MKSI (-10,1 %)

MKS Instruments (US) - Plasma/vacuum technology

$ASM (-3,08 %)

ASM International (NL) - Deposition systems

1.ASML, 2.Keysight Technologies, 3.Fanuc are my top 3 in this sector

3. chip manufacturing (foundries)

$TSM (-6,55 %) TSMC (TW) - leading foundry

$SMSN (-4,06 %) Samsung Electronics (KR) - foundry + memory

$GFS (-7,55 %) GlobalFoundries (US) - specialty chips

$INTC (-5,15 %)

Intel Foundry Services (US) - new western foundry player

$981

SMIC (CN) - largest Chinese foundry

$UMC

UMC (TW) - Power/RF/Embedded chips

1.TSMC, 2.Intel, 3.Samsung Electronics are my top 3 in this sector

4. computing & control unit ("brain")

$NVDA (-6,14 %) Nvidia (US) - GPUs, AI chips

$INTC (-5,15 %) Intel (US) - CPUs, FPGAs

$AMD (-10,01 %) AMD (US) - CPUs, GPUs

$MRVL (-5,93 %) Marvell (US) - Network Chips

$MU (-6,96 %) Micron (US) - Memory

$DELL (-4,8 %) Dell Technologies (US) - Edge & Infrastructure

Graphcore (UK) - AI chips (IPU) - not a listed company

Cerebras (US) - Wafer-scale engine - not a listed company

SiPearl (FR) - European HPC chip - not a listed company

1.Nvidia, 2.Marvell, 3.Micron are my top 3 in this sector

5. sensors ("senses")

$6758 (-5,66 %) Sony (JP) - image sensors

$6861 (-1,03 %) Keyence (JP) - Industrial sensors

$STM (-5,65 %) STMicroelectronics (FR/IT) - Sensors, MCUs

$TDY Teledyne (US) - optical/infrared sensors

$CGNX (-13,21 %) Cognex (US) - Machine Vision

$HON (-2,58 %) Honeywell (US) - sensor technology, security

ANYbotics (CH) - autonomous sensor fusion - not a listed company

$AMBA (-13,21 %) Ambarella (US) - video & computer vision SoCs for real-time image recognition

$OUST

Velodyne Lidar (US) - Lidar sensors - acquisition by Ouster

$AMS (-5,97 %)

OSRAM (AT/DE) - optical sensors

1.Teledyne, 2.Keyence, 3.Ouster are my top 3 in this sector

6. actuators & power electronics ("muscles")

$IFX (-4,21 %) Infineon (DE) - Power Electronics

$ON (-7,46 %) onsemi (US) - Power & Sensors

$TXN (-4,45 %) Texas Instruments (US) - Mixed-Signal Chips

$ADI (-6,83 %) Analog Devices (US) - Signal Processing

$PH Parker-Hannifin (US) - Hydraulics/Pneumatics

$MP (+8,11 %) MP Materials (US) - Magnets

$APH (-3,8 %) Amphenol (US) - Connectors

$6481 (-1,59 %) THK (JP) - Linear guides & actuators

$6324 (-6,99 %)

Harmonic Drive (JP) - Precision gears & servo drives for robotics

$6594 (-2,91 %)

Nidec (JP) - Electric motors

$6506 (-1,37 %)

Yaskawa (JP) - Drives & Robotics

$SU (-2,76 %)

Schneider Electric (FR) - Energy & control solutions

$ZIL2 (+5,96 %)

ElringKlinger (DE) - Battery & fuel cell technology, lightweight construction

1.Parker-Hannifin, 2.MP Materials, 3.Infinion are my top 3 in this sector

7. communication & networking ("nerves")

$QCOM (-8,32 %) Qualcomm (US) - mobile communications, edge AI

$ANET (-4,24 %) Arista Networks (US) - Networks

$CSCO (-3,83 %) Cisco (US) - Networks, Security

$EQIX (-1,43 %) Equinix (US) - Data centers

NTT Docomo (JP) - 5G/6G carrier - not a listed company

$VZ Verizon (US) - Telecommunications

$SFTBY SoftBank (JP) - Carrier + Robotics

$ERIC B (-0,31 %)

Ericsson (SE) - 5G/IoT infrastructure

$NOKIA (+1,08 %)

Nokia (FI) - 5G/6G for industry

$HPE (-7,48 %)

Juniper Networks (US) - Network technology - acquisition by HP

1.Arista Networks, 2.SoftBank, 3.Cisco are my top 3 in this sector

8. energy supply

$3750 (-10,56 %) CATL (CN) - Batteries

$6752 (-3,59 %) Panasonic (JP) - Batteries

$373220 LG Energy (KR) - Batteries

$ALB (-7,74 %) Albemarle (US) - Lithium

$LYC (+3,13 %) Lynas (AU) - Rare earths

$UMICY (-0,49 %) Umicore (BE) - recycling

WiTricity (US) - inductive charging - not a listed company

$ABBN (-0,59 %) Charging (CH) - charging infrastructure

$SLDP

Solid Power (US) - Solid state batteries

Northvolt (SE) - European batteries - not a listed company

$PLUG

Plug Power (US) - fuel cells

$KULR (-6,68 %)

KULR Technology (US) - Thermal management & battery safety for mobile systems

1.Albemarle, 2.CATL, 3.Panasonic are my top 3 in this sector

9. cloud & infrastructure

$AMZN (-5,92 %) Amazon AWS (US) - Cloud, AI

$MSFT (-3,3 %) Microsoft Azure (US) - Cloud, AI

$GOOG (-3,33 %) Alphabet Google Cloud (US) - Cloud, ML

$VRT (-6,22 %)

Vertiv Holdings (US) - Data center infrastructure (UPS, cooling, edge)

$ORCL (-3,03 %)

Oracle Cloud (US) - ERP + Cloud

$IBM (-4,51 %)

IBM Cloud (US) - Hybrid cloud + AI

$OVH (-2,16 %)

OVHcloud (FR) - European cloud

1.Alphabet, 2.Microsoft, 3.Oracle are my top 3 in this sector

10. software & data platforms

$PLTR (-7,09 %) Palantir (US) - Data integration

$DDOG (-5,26 %) Datadog (US) - Monitoring

$SNOW (-4,44 %) Snowflake (US) - Data Cloud

$ORCL (-3,03 %) Oracle (US) - Databases, ERP

$SAP (-3,86 %) SAP (DE) - ERP systems

$SPGI S&P Global (US) - financial/market data

ROS2 Foundation - robotics middleware - not listed on the stock exchange

$NVDA (-6,14 %) NVIDIA Isaac (US) - robotics development - part of Nvidia

$INOD (-11,68 %) Innodata (US) - data annotation & AI training data

$PATH (-10,71 %)

UiPath (RO/US) - Robotic process automation

$AI (-7,18 %)

C3.ai (US) - AI platform

$ESTC (-4,39 %)

(NL/US) - Search & data analysis

1.S&P Global, 2.Palantir, 3.Datadog are my top 3 in this sector

11. end applications / robots

$ABBN (-0,59 %) ABB (CH/SE) - Industrial Robots

$6954 (-1,33 %) Fanuc (JP) - Industrial robots

$TSLA (-6,86 %) Tesla Optimus (US) - humanoid robot

$9618 (-5,5 %) JD.com (CN) - logistics robot

$AAPL (-4,63 %) Apple (US) - Platform & UX

$700 (-6,61 %) Tencent (CN) - Platform & AI

$9988 (-8,32 %) Alibaba (CN) - logistics & platform

PAL Robotics (ES) - humanoid robots - not a listed company

Neura Robotics (DE) - cognitive humanoid robots - not a listed company

$TER (-9,45 %) Universal Robots (DK) - cobots - belongs to the Teradyne Corporation

Engineered Arts (UK) - humanoid robots - not a listed company

$ISRG (-4,16 %) Intuitive Surgical (US) - surgical robotics

$GMED (-5,44 %)

Globus Medical (US) - surgical robotics (ExcelsiusGPS platform)

$7012 (-7,11 %) Kawasaki Heavy Industries (JP) - industrial robots, automation

$CPNG (-4,08 %) Coupang (KR) - Logistics end user

$IRBT (-7,91 %)

iRobot (US) - consumer robotics (e.g. Roomba), non-humanoid, but navigation/sensor fusion

Boston Dynamics (US) - humanoid & mobile robots-no listed company

Hanson Robotics (HK) - humanoid robots (Sophia) - not a listed company

Agility Robotics (US) - humanoid robot "Digit" - not a listed company

1.Apple, 2.Tencent, 3.Alibaba are my top 3 in this sector

🛠 2. cross enablers (shovel manufacturers) - with hidden champions

Raw materials & battery materials

Albemarle - Lynas - Umicore

$SQM

SQM (CL) - Lithium

$ILU (-2,29 %)

Iluka Resources (AU) - Rare earths

$ARR (+44,81 %)

American Rare Earths (US/AU) - New supply chains

my number 1 in the sector is Albemarle

manufacturing technology

ASML - Applied Materials - Tokyo Electron

$LRCX (-8,15 %)

Lam Research (US) - Plasma/etching processes

$ASM (-3,08 %)

ASM International (NL) - ALD equipment

$MKSI (-10,1 %)

MKS Instruments (US) - Plasma/vacuum technology

my number 1 in the sector is ASML

Quality assurance

Keysight - Advantest - Teradyne

$EMR (-4,69 %)

National Instruments (US) - Measurement technology - from Emerson Electric adopted

$300567

ATE Test Systems (CN) - test systems

$FORM (-1,8 %)

FormFactor (US) - Wafer probing

my number 1 in the sector is Keysight

Motion & Drive

Parker-Hannifin

Festo (DE) - Pneumatics, Soft Robotics - not a listed company

Bosch Rexroth (DE) - Drives, Controls - not a listed company

$6481 (-1,59 %)

THK (JP) - Linear guides

my number 1 in the sector is Parker-Hannifin

Sensors/Imaging

$TDY Teledyne

$BSL (-3,33 %) Basler (DE) - Industrial cameras

FLIR (US) - Thermal imaging sensors - acquisition by Teledyne

ISRA Vision (DE) - Machine Vision - not a listed company

my number 1 in the sector is Teledyne

Magnets & Materials

MP Materials

$6501 (-7,57 %)

Hitachi Metals (JP) - Magnetic materials

VacuumSchmelze (DE) - Magnetic materials - not a listed company

$4063 (-3,42 %)

Shin-Etsu Chemical (JP) - Specialty materials

my number 1 in the sector is MP Materials

Chip Design & Simulation

Synopsys - Cadence - ARM

$SIE (-2,34 %)

Siemens EDA (DE/US)-Mentor Graphics-strategic business unit of Siemens AG

Imagination Tech (UK) - GPU-IP - not a listed company

$CEVA (-12,41 %)

CEVA (IL) - Signal Processor IP

my number 1 in the sector is Synopsys

Engineering & Lifecycle

PTC - Dassault - Siemens

Altair (US) - Simulation - no longer a listed company

$HXGBY (-2,42 %)

Hexagon (SE) - Metrology

$SNPS (-12,42 %)

ANSYS (US) - Simulation - takeover by Synopsys

my number 1 in the sector is Siemens

Networks & Data Centers

Arista - Cisco - Equinix

$HPE (-7,48 %)

Juniper (US) - Networks - Acquisition of HPE

$DTE (+0,17 %)

T-Systems (DE) - Industry cloud

$OVH (-2,16 %)

OVHcloud (FR) - European cloud

my number 1 in the sector is Arista

Cloud infrastructure

AWS - Azure - Google Cloud

$ORCL (-3,03 %)

Oracle Cloud (US) - ERP & databases

$IBM (-4,51 %)

IBM Cloud (US) - Hybrid Cloud

$9988 (-8,32 %)

Alibaba Cloud (CN) - Asian Cloud

$VRT (-6,22 %)

Vertiv Holdings (US) - Cloud/Infra

my number 1 in the sector is Alphabet (Google)

finance/information infra

S&P Global

$MCO (-2,16 %)

Moody's (US) - Ratings

$MSCI (-2,55 %)

MSCI (US) - Indices

$MORN

Morningstar (US) - Investment Research

my number 1 in the sector is S&P Global

Creative/Experience Infra

Adobe

$ADSK (-3,77 %)

Autodesk (US) - CAD & Design

$U

Unity (US) - 3D/AR simulation

Epic Games (US) - Unreal Engine - not a listed company

my number 1 in the sector is Adobe

Platform & Ecosystem

Apple - Tencent - Alibaba

$META (-5,02 %)

Meta (US) - AR/VR, Social Robotics

ByteDance (CN) - AI & platforms - not a listed company

$9888 (-8,29 %)

Baidu (CN) - AI & Cloud

my number 1 in the sector is Tencent

Infrastructure/Edge

Dell

$HPE (-7,48 %)

HPE (US) - Edge Computing

$SMCI (-9,91 %)

Supermicro (US) - AI servers

$6702 (-5,49 %)

Fujitsu (JP) - Edge & HPC

my number 1 in the sector is Dell

storage solutions

Micron

$HY9H (-4,16 %)

SK Hynix (KR) - Memory

$285A (-4,8 %)

Kioxia (JP) - NAND

$WDC

Western Digital (US) - Storage solutions

my number 1 in the sector is Micron

🏛 3. secondary key sectors with hidden champions

Financing & Capital

$GS (-2,43 %) Goldman Sachs (US) - investment bank; ECM/DCM, M&A, growth financing

$MS Morgan Stanley (US) - investment bank; tech banking, capital markets

$BLK (-3,34 %) BlackRock (US) - asset manager; capital allocation, ETFs/index funds

$9984 (-8,87 %) SoftBank Vision Fund (JP) - mega VC; growth equity in robotics/AI

Sequoia Capital (US) - venture capital; early/growth in AI/robotics - this is a classic venture capital fund

DARPA (US) - government R&D funding (robotics/defense) - independent research and development agency

EU Horizon (EU) - research funding/grants for DeepTech - Innovative Europe pillar

China State Funds (CN) - state industry/technology fund

Lux Capital (US) - VC for DeepTech - Uptake (US) - AI-based predictive maintenance

DCVC (US) - Robotics & AI focus - investing exclusively via VC fund investments

Speedinvest (AT) - EU VC for robotics - access to investment only via fund investments

my number 1 in the sector is Softbank

Maintenance & Service

$SIE (-2,34 %) Siemens (DE) - Industrial Service, Lifecycle & Retrofit

$ABBN (-0,59 %) ABB (CH/SE) - Robotics Service, Spare Parts, Field Support

$GEHC (-4,73 %) GE Healthcare (US) - Medtech service incl. robotic systems

Uptake (US) - AI-based predictive maintenance - not a listed company

Augury (US/IL) - condition monitoring, condition diagnostics - not a listed company

$KU2 KUKA Service (DE) - Robotics maintenance

$6954 (-1,33 %) Fanuc Service (JP) - global service network

Boston Dynamics AI Institute (US) - Robotics longevity - funded by Hyundai Motor Group

my number 1 in the sector is Siemens

Marketing & Advertising

$WPP (-4,43 %) WPP (UK) - global advertising group; branding/communications

$OMC Omnicom (US) - marketing/PR network

$PUB (-1,04 %) Publicis (FR) - communications/advertising group

$META (-5,02 %) Meta (US) - Digital Ads (Facebook/Instagram)

$GOOG (-3,33 %) Google Ads (US) - search & display advertising

TikTok / ByteDance (CN) - social ads & distribution - not a listed company

$AAPL (-4,63 %) Apple (US) - Branding/UX; Acceptance & Platform Marketing

$WPP (-4,43 %)

AKQA (UK/US) - Tech branding - Since 2012 majority owned by the WPP Groupbut continues to operate as an autonomous operating unit

R/GA (US) - Innovation marketing - not a listed company

Serviceplan (DE) - largest independent EU agency - not a listed company

my number 1 in the sector is Meta

Law, Regulation & Ethics

ISO (CH) - international standards, robotics standards

TÜV (DE) - certification & safety tests

UL (US) - safety/conformity testing

EU AI Act (EU) - legal framework for AI & robotics

UNESCO AI Ethics (UN) - global ethics guidelines

Fraunhofer IPA (DE) - Robotics safety standards

ANSI (US) - standards

IEC (CH) - Electrical engineering standards

Training & Talent

MIT (US) - Robotics/AI Research & Education

ETH Zurich (CH) - autonomous systems & robotics

Stanford (US) - AI/Robotics labs & spin-offs

Tsinghua University (CN) - Robotics/AI in Asia

CMU (US) - Robotics Institute

EPFL (CH) - Robotics research

TU Munich (DE) - humanoid robot "Roboy"

🌍 Top 25 companies for humanoid robotics

These companies are central to the development & production of humanoid robotsbecause without them, crucial parts of the chain would be missing:

Chips & computing power (brain of the robots)

$NVDA (-6,14 %) Nvidia (US) - AI GPUs & Isaac platform, foundation for robotic AI

$2330 TSMC (TW) - world's most important foundry, produces the AI chips

$ASML (-5,06 %) ASML (NL) - EUV lithography, indispensable for chip production

$005930 Samsung Electronics (KR) - memory, logic, foundry

$HY9H (-4,16 %) SK Hynix (KR) - DRAM & NAND memory for AI

$MU (-6,96 %) Micron (US) - Memory solutions for AI workloads

my number 1 in the sector is ASML

Sensors & perception (senses of robots)

$SONY Sony (JP) - image sensors, market leader

$6861 (-1,03 %) Keyence (JP) - Industrial sensors & vision systems

$CGNX (-13,21 %) Cognex (US) - Machine Vision, precise image processing

my number 1 in the sector is Keyence

Actuators & motion (muscles of robots)

$IFX (-4,21 %) Infineon (DE) - power electronics, motor control

$6594 (-2,91 %) Nidec (JP) - World market leader for electric motors

$PH Parker-Hannifin (US) - hydraulics/pneumatics, motion technology

$6481 (-1,59 %) THK (JP) - Linear guides & actuators

my number 1 in the sector is Parker-Hannifin

Communication, cloud & infrastructure (nerves & data flow)

$QCOM (-8,32 %) Qualcomm (US) - Mobile & Edge Chips

$AMZN (-5,92 %) Amazon AWS (US) - Cloud & AI infrastructure

$MSFT (-3,3 %) Microsoft Azure (US) - Cloud, AI services

$CSCO (-3,83 %) Cisco (US) - Networks & Security

$VRT (-6,22 %) Vertiv Holdings (US) - Data Center Infrastructure

my number 1 in the sector is Microsoft

End Applications & Platforms (robots themselves)

$TSLA (-6,86 %) Tesla (US) - humanoid robot Optimus

$ABBN (-0,59 %) ABB (CH/SE) - Robotics & Automation

$6954 (-1,33 %) Fanuc (JP) - industrial robots & CNC systems

$7012 (-7,11 %) Kawasaki Heavy Industries (JP) - industrial robots

PAL Robotics (ES) - humanoid robots (TALOS, ARI, TIAGo) - not a listed company

Neura Robotics (DE) - cognitive humanoid robots - not a listed company

Universal Robots (DK) - cobots

my number 1 in the sector is Tesla

🇪🇺 Top 10 European key companies for humanoid robotics

$ASML (-5,06 %)

ASML (NL)

World market leader in EUV lithography - no modern chips for AI & robotics without ASML.

$IFX (-4,21 %) Infineon (DE)

Leading in power electronics & motor control - crucial for actuators of humanoid robots.

$STM (-5,65 %)

STMicroelectronics (FR/IT)

Sensors, microcontrollers & power chips - the basis for control & perception.

$SAP (-3,86 %)

SAP (DE)

ERP & data platforms, important for integrating humanoid robots into industrial processes.

$SIE (-2,34 %)

Siemens (DE)

Industrial software, automation, digital twin - key for engineering & lifecycle management.

$KU2 KUKA (EN)

Robotics pioneer, industrial robots & automation - know-how for humanoid motion mechanics.

PAL Robotics (ES) - not a listed company

Specialist for humanoid robots (TALOS, ARI, TIAGo), internationally used in research & service.

Neura Robotics (DE) - Not a listed company

Young high-tech company, develops cognitive humanoid robots with advanced AI (4NE-1).

Universal Robots (DK) - Not a listed company

Market leader for cobots - platform for safe human-robot collaboration.

Engineered Arts (UK) - not a listed company

Develops humanoid robots such as Amecaknown for realistic facial expressions & gestures - important for HRI (Human-Robot Interaction)

🌏 Top 10 Asian key companies for humanoid robotics

$2330

TSMC (Taiwan)

World's largest semiconductor foundry, produces high-end chips (e.g. Nvidia, AMD, Apple) - no AI hardware without TSMC.

$005930

Samsung Electronics (South Korea)

Foundry, memory, logic chips, image sensors - extremely broadly positioned in robotics components.

$HY9H (-4,16 %)

SK Hynix (KR) - Memory

$SONY

Sony (Japan)

Market leader in CMOS image sensors, essential for robotic vision & perception.

$6861 (-1,03 %)

Keyence (Japan)

Sensor technology & machine vision for industrial automation, widely used in robotics.

$6954 (-1,33 %)

Fanuc (Japan)

Industrial robots & CNC systems, one of the most important manufacturers of robotics hardware worldwide.

$6506 (-1,37 %)

Yaskawa Electric (Japan)

Drives, motion control & robot arms - relevant for humanoid motion control.

$6594 (-2,91 %)

Nidec (Japan)

World market leader for electric motors (from mini motors to high-performance drives).

$7012 (-7,11 %)

Kawasaki Heavy Industries (JP) - Industrial robots

$9618 (-5,5 %)

JD.com (China)

Driver for robotics in e-commerce & logistics, invests in humanoid robotics applications

1Lun·

Build robots, earn shovels

The hype is all about humanoid robots, but the constant winners are in the background.

I have divided the analysis into two perspectives. 1. the complete value chain of humanoid robots, which shows all the players from the chip to the finished robot, and 2. the blade manufacturers in the background, who always earn money as enablers, regardless of which manufacturer wins the race.

ASML, Applied Materials and Tokyo Electron dominate in manufacturing technology. Quality assurance comes from Keysight, Advantest and Teradyne. Chip design is supported by Synopsys, Cadence and ARM. Data streams are secured by Arista Networks, Cisco and Equinix. The computing basis is created in the cloud by Amazon, Microsoft and Alphabet. Albemarle, Lynas and Umicore play a central role in raw materials and battery materials. These companies monetize their customers' investment waves, have high barriers to entry, service revenues and pricing power, but remain cyclical with risks from export rules, capex cuts and currency movements.

🌐 Value chain of humanoid robots Sector overview

1. research & chip design (IP / EDA)

$ARM (-10,82 %)

ARM Holdings (ARM, UK/USA) - CPU architectures

$SNPS (-12,42 %)

Synopsys (SNPS, USA) - Chip design software

$CDNS (-9,81 %)

Cadence Design Systems (CDNS, USA) - EDA & Simulation

2. manufacturing technology & equipment

$ASML (-5,06 %)

ASML (ASML, NL) - EUV lithography, key monopoly

$AMAT (-6,65 %)

Applied Materials (AMAT, USA) - Process equipment

$8035 (-7,11 %)

Tokyo Electron (8035.T, JP) - Wafer equipment

$KEYS (-7,24 %)

Keysight Technologies (KEYS, USA) - Test & RF measurement technology

$6857 (-6,61 %)

Advantest (6857.T, JP) - Semiconductor test systems

$TER (-9,45 %)

Teradyne (TER, USA) - Test systems + robotics (Universal Robots)

3. chip production (Foundries)

$TSM (-6,55 %)

TSMC (TSM, TW) - Largest contract manufacturer

$005930

Samsung Electronics (005930.KQ, KR) - Memory + Foundry

$GFS (-7,55 %)

GlobalFoundries (GFS, USA) - Specialized production

4. computing & control unit ("brain")

$NVDA (-6,14 %)

Nvidia (NVDA, USA) - GPUs, AI accelerators

$INTC (-5,15 %)

Intel (INTC, USA) - CPUs, FPGAs

$AMD (-10,01 %)

AMD (AMD, USA) - CPUs/GPUs

$MRVL (-5,93 %)

Marvell Technology (MRVL, USA) - Network/data center chips

5. sensors ("senses")

$6758 (-5,66 %)

Sony (6758.T, JP) - CMOS image sensors

$6861 (-1,03 %)

Keyence (6861.T, JP) - Vision systems, sensors

$STM (-5,65 %)

STMicroelectronics (STM, CH/FR) - MEMS sensors

6. actuators & power electronics ("muscles")

$IFX (-4,21 %)

Infineon (IFX, DE) - Power semiconductors, SiC

$ON (-7,46 %)

N Semiconductor (ON, USA) - SiC/Power Chips

$STM (-5,65 %)

STMicroelectronics (STM, CH/FR) - Motor control & power

$TXN (-4,45 %)

Texas Instruments (TXN, USA) - Motor control, power ICs

$ADI (-6,83 %)

Analog Devices (ADI, USA) - Energy & BMS chips

7. communication & networking ("nerves")

$QCOM (-8,32 %)

Qualcomm (QCOM, USA) - 5G/SoCs

$AVGO (-7,17 %)

Broadcom (AVGO, USA) - Network & radio chips

$SWKS (-7 %)

Skyworks Solutions (SWKS, USA) - RF components

8. energy supply

$300750

CATL (300750.SZ, CN) - Batteries

$6752 (-3,59 %)

Panasonic (6752.T, JP) - Batteries for automotive/robotics

$373220

LG Energy Solution (373220.KQ, KR) - Batteries

9. cloud & infrastructure

$AMZN (-5,92 %)

Amazon (AMZN, USA) - AWS

$MSFT (-3,3 %)

Microsoft (MSFT, USA) - Azure

$GOOG (-3,33 %)

Alphabet (GOOGL, USA) - Google Cloud

$EQIX (-1,43 %)

Equinix (EQIX, USA) - Data center operator

$ANET (-4,24 %)

Arista Networks (ANET, USA) - Network infrastructure

$CSCO (-3,83 %)

Cisco Systems (CSCO, USA) - Edge & Data Center Networks

10. software & data platforms

$PLTR (-7,09 %)

Palantir (PLTR, USA) - Data integration, decision software

$DDOG (-5,26 %)

Datadog (DDOG, USA) - Cloud monitoring / observability

$SNOW (-4,44 %)

Snowflake (SNOW, USA) - Cloud-native data platform

$ORCL (-3,03 %)

Oracle (ORCL, USA) - Databases, ERP

$SAP (-3,86 %)

SAP (SAP, DE) - ERP/cloud systems

$PATH (-10,71 %)

UiPath (PATH, USA) - Automation software (RPA)

$AI (-7,18 %)

C3.ai (AI, USA) - Enterprise AI platform

11. end applications / robots

$ABB

ABB (ABB, CH) - Industrial robots

$6954 (-1,33 %)

Fanuc (6954.T, JP) - Industrial robots, CNC

$TSLA (-6,86 %)

Tesla (TSLA, USA) - Optimus" humanoid robot

$9618 (-5,5 %)

JD.com (JD, CN) - E-commerce & automated logistics

🛠️ Shovel manufacturer for humanoid robots

🔹 Hardtech (physical "shovels")

These companies provide the material basis: manufacturing machines, raw materials, semiconductor base.

Semiconductor Equipment & Manufacturing

$ASML (-5,06 %)

ASML (ASML, NL) - EUV lithography (monopoly).

$AMAT (-6,65 %)

Applied Materials (AMAT, USA) - Wafer equipment.

$8035 (-7,11 %)

Tokyo Electron (8035.T, JP) - Process equipment.

Test systems (hardware-side)

$6857 (-6,61 %)

Advantest (6857.T, JP) - Semiconductor test.

$TER (-9,45 %)

Teradyne (TER, USA) - Test systems + industrial robots.

Materials & raw materials

$ALB (-7,74 %)

Albemarle (ALB, USA) - Lithium (batteries).

$LYC (+3,13 %)

Lynas Rare Earths (LYC.AX, AUS) - Rare earths for magnets.

$UMICY (-0,49 %)

Umicore (UMI.BR, BE) - Cathode materials, recycling.

🔹 Soft/infra (digital "shovels")

These companies supply the infrastructure & toolswithout which development, training and operation would be impossible.

Design Software & IP

$SNPS (-12,42 %)

Synopsys (SNPS, USA) - EDA software.

$CDNS (-9,81 %)

Cadence Design Systems (CDNS, USA) - Chip design & simulation.

$ARM (-10,82 %)

ARM Holdings (ARM, UK/USA) - CPU architectures (license model).

Test & Measurement (software/signal level)

$KEYS (-7,24 %)

Keysight Technologies (KEYS, USA) - Electronics & RF test systems.

Network & data center backbone

$ANET (-4,24 %)

Arista Networks (ANET, USA) - High-speed networks.

$CSCO (-3,83 %)

Cisco Systems (CSCO, USA) - Data center/edge networks.

$EQIX (-1,43 %)

Equinix (EQIX, USA) - Data centers (colocation).

Cloud infrastructure

$AMZN (-5,92 %)

Amazon (AMZN, USA) - AWS (cloud, AI training).

$MSFT (-3,3 %)

Microsoft (MSFT, USA) - Azure.

$GOOG (-3,33 %)

Alphabet (GOOGL, USA) - Google Cloud.

Takeaway: Investing in the infrastructure stack allows you to participate in the robotics trend regardless of the subsequent product winner and reduces the individual product risk, but you have to live with cycles. In your opinion, which stage of the chain offers the best risk/return combination and fits into a disciplined portfolio?

Source: Own analysis based on publicly available company information and IR materials of the companies mentioned.

Image material: Techa Tungateja/iStockphoto

4848

34 Comentarios

•

55

•

2Lun·

Trump, Earnings, and My New Buy: Doubling Down on an Undervalued Giant

US markets opened strongly today, then faded throughout the day, while President Trump made headlines by proposing new tariffs on semiconductors and pharmaceutical imports, emphasizing onshore production. Despite broader market hesitation, Palantir ($PLTR (-7,09 %) ) impressed with strong earnings, while other players fell flat on expectations, voicing concerns about tariff impact. I also doubled down on one of my key positions, Salesforce ($CRM (-2,41 %) ), reinforcing my conviction in the company’s bright future. Looking forward, my eyes are on Oscar Health ($OSCR (-4,92 %) ) and Novo Nordisk ($NVO (-3,35 %) /$NOVO B (-3,44 %) ), both of which report earnings tomorrow.

Macro View – Trump vs. The Economy

After sending a rather peculiar letter to drug companies last week demanding lower prices, President Trump continued his harassment tour of pharmaceutical companies today by threatening an initially “low” tariff rate, which would then eventually increase to 250% over the next 12 to 18 months.

Sorry Mr. President having to break it to you, but you can’t dictate companies to throw out their pricing strategies, just because you disapprove of them, only to tell them a week later they’ll have to pay three times more to import their drugs. The math doesn’t add up: Lower prices don’t mix well with higher production costs. That’s business 101, a course a Wharton graduate should have attended, at least physically, if not mentally.

Earnings – The ONE Massively Overvalued Exception

While many earnings left investors disappointed amid this booming earnings season, from Caterpillar ($CAT (-2,48 %) ) over Lucid ($LCID (-3,53 %) ) to SuperMicro ($SMCI (-9,91 %) ), citing different reasons for their misses, ranging from an increasingly noticeable impact of tariffs to just weak execution, one name continues its upward trajectory: Palantir, a great company with an exorbitant price tag.

Don’t get me wrong, I find Palantir to be an incredibly interesting business, with strong growth prospects and a solid leadership, but I just can’t imagine a reality in which a P/E ratio of close to 800 is justified for any company. Even if they cured cancer, that valuation would be a stretch. But I suppose the stock has become more of a religion or cult anyway, rather than an investment based on fundamentals.

My Move – Added to $CRM (Salesforce)

While markets were busy decoding Trump’s latest comments and speculating about his future FED chair pick, I expanded my position in Salesforce, by buying 5 shares at $250, bringing my total share count to 25, which equates to roughly 4% of my portfolio, representing the second largest position behind ASML ($ASML (-5,06 %) ).

Salesforce is trading at a forward P/E ratio of 21, while boasting solid 8% revenue growth YoY and strong double-digit EPS expansion. Admittedly, the company isn’t the growth machine it once was, but its focus has shifted visibly from expansion at every cost to an emphasis on profitability. Margins are steadily improving, with gross profit approaching 80%. That’s part of the game, as companies become more mature, they grow different metrics.

One thing to look at, however, is Salesforce’s implementation of AI. The main reason for the stock’s weakness and historically low valuation is concerns about the company’s AI-powered task-managing platform Agentforce, which hasn’t yet shown the results investors would have hoped for. Nevertheless, I see an attractive risk/reward ratio at the current levels. And let’s not forget that Marc Benioff and his team have consistently delivered and proven strong execution. If the stock dips further, I may add more.

Looking Ahead

Tomorrow two companies in my portfolio will report earnings: Novo Nordisk and Oscar Health. I am bullish on both, for different reasons.

I recently published a detailed analysis on Novo Nordisk, arguing that while short-term headwinds might persist, long-term trends remain in place and the company is in a prime spot to capitalize on them. If I had to bet, I would bet on a beat tomorrow, given the conservative estimates and comments from the recently appointed CEO.

With Oscar it’s simpler: I firmly believe in its disruption potential within the health insurance industry, and I look forward to hearing from the company’s stellar leadership during the earnings call.

No matter what happens tomorrow, I remain confident in both companies and will be following them closely.

+ 1

1616

2Lun·

Super Micro Computer Q4'25 Earnings Highlights

🔹 Revenue: $5.8B (Est. $5.99B) 🔴; UP +7% YoY

🔹 Adj EPS: $0.41 (Est. $0.44) 🔴; -24% YoY

Guidance

🔹 FY26 Revenue: At least $33.0B (Est. $30.03B) 🟢

🔹 Q1 Revenue: $6.0B–$7.0B (Est. $6.61B) 🟡

🔹 Q1 EPS (Non-GAAP): $0.40–$0.52 (Est. $0.56) 🔴

Other Metrics:

🔹 Net Income: $195M; DOWN -34% YoY

🔹 Gross Margin: 9.5%; DOWN -70bps YoY

🔹 Operating Cash Flow: $864M

🔹 Capex & Investments: $79M

CEO Commentary

🔸 “We made solid progress in FY25 by growing our AI solution leadership in Neoclouds, CSPs, Enterprises, and Sovereign entities, which fueled our 47% annual growth.”

🔸 “Our new Datacenter Building Block Solutions (DCBBS) offer exceptional value to customers seeking faster datacenter deployment.”

🔸 “We’re on track to grow more large-scale datacenter customers from four in FY25 to six to eight in FY26.”

88

2Lun·

AEX opens positive amid global stock market turmoil

The AEX index starts the day with an indication of +0.3%, while international markets also turn green. Wall Street largely managed to recover from Friday's sell-off, and Asian stock markets follow with Korea and Taiwan as outliers. U.S. 10-year interest rates rise slightly to 4.21%, while German rates fall to 2.62%. The euro/dollar exchange rate is quoted at 1.1550. The Damrak is relatively quiet, with only B&S presenting figures. Internationally, however, there is plenty of activity: Palantir surprises with strong quarterly results, while Hims & Hers falls sharply. Figma debuts with a 27.4% drop. The US puts pressure on India and China because of Russian oil imports, further raising trade tensions. Investors look forward to figures from AMD, Snap, Rivian and Super Micro Computer. Also on the agenda are the purchasing managers' indices of the service sectors in Germany and the US. In short: plenty of excitement and thrills on the trading floor.

$PLTR (-7,09 %)

$HIMS (-8,47 %)

$SHEL (-3,05 %)

$BP. (-2,96 %)

$AMD (-10,01 %)

$SNAP (-8,55 %)

$RIVN (-3,35 %)

$SMCI (-9,91 %)

🔗 Source reference:

This summary is based on the article "AEX indicatie is +0,3%, volop spanning en nog meer sensatie" by Arend Jan Kamp, published on StockWatch on Aug. 5, 2025.

www.stockwatch.nlAEX indicatie is +0,3%, volop spanning en nog meer sensatie - StockWatch

11

2Lun·

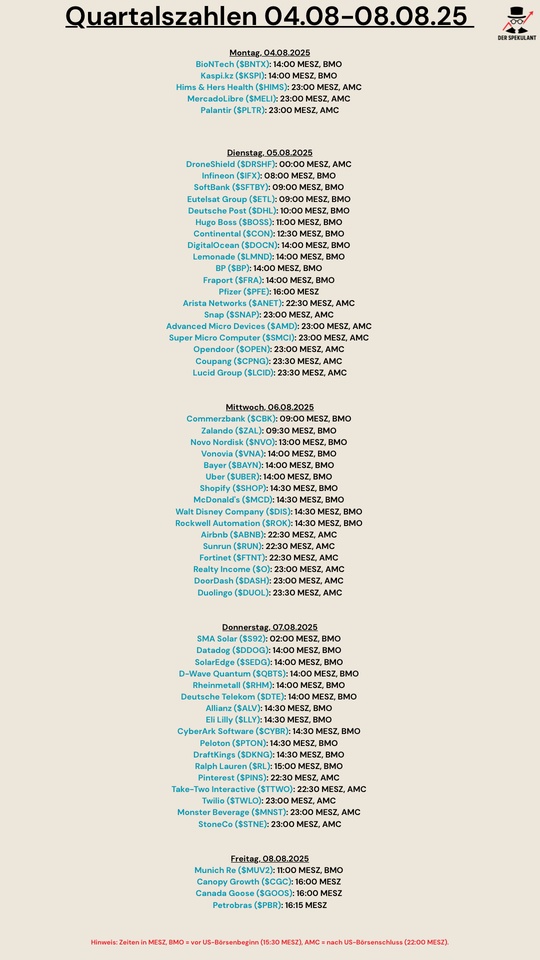

Quartalszahlen 04.08-08.08.2025

$BNTX (-2,88 %)

$KSPI (-2,43 %)

$HIMS (-8,47 %)

$MELI (-6,22 %)

$PLTR (-7,09 %)

$DRO (-4,78 %)

$IFX (-4,21 %)

$9434 (-3,05 %)

$FR0010108928

$DHL (-1,89 %)

$BOSS (-1,63 %)

$CONTININS

$DOCN (-5,38 %)

$LMND (-10,89 %)

$BP. (-2,96 %)

$FRA (-0,1 %)

$PFIZER

$SNAP (-8,55 %)

$AMD (-10,01 %)

$SMCI (-9,91 %)

$OPEN (-10,72 %)

$CPNG (-4,08 %)

$LCID (-3,53 %)

$CBK (-0,56 %)

$ZAL (-4,18 %)

$NOVO B (-3,44 %)

$VNA (+0,52 %)

$BAYN (-1,05 %)

$UBER (-3,78 %)

$SHOP (-9,54 %)

$MCD (+0,18 %)

$DIS (-2,19 %)

$ROK (-3,15 %)

$ABNB (-2,76 %)

$RUN (-8,53 %)

$FTNT (-4,55 %)

$O (-1,42 %)

$DASH (-5,35 %)

$DUOL

$S92 (-2,39 %)

$DDOG (-5,26 %)

$SEDG (-9,46 %)

$QBTS (-7,49 %)

$RHM (-2,26 %)

$DTE (+0,17 %)

$ALV (-0,68 %)

$LLY (-3,36 %)

$CYBR (-3,24 %)

$PTON (-6,11 %)

$DKNG (-7,73 %)

$RL (-4,68 %)

$PINS

$TTWO (-2,88 %)

$TWLO (-6,43 %)

$MNST (+0,39 %)

$STNE (-3,7 %)

$MUV2 (-0,74 %)

$WEED (-16,71 %)

$GOOS (-2,97 %)

$PETR3T

$ANET (-4,24 %)

3Lun·

Trimming my position in Celestica

I initially bought shares of Celestica $CLS (-7,11 %) because I saw it as a clear beneficiary of the AI boom. It felt like an undervalued gem:

· A pristine balance sheet

· Strong fundamentals

· A valuation that simply didn’t reflect its growth potential.

That conviction paid off: my total position was up 235% at the time of selling.

My first purchase was at €20.54 per share. I added twice more, at €48.80 and again at €90.00. I recently trimmed my position, selling part of it at €133.50.

I still believe in the company’s long-term vision. The pipeline of new products, the ramp-up in production, and the explosive growth of hyperscalers all suggest a promising future. However, valuation has run ahead of fundamentals, and that’s where I draw a line. The stock now commands a premium that no longer aligns with the initial reasons I bought in.

Additionally, Celestica still has concentrated exposure to a few large clients, both in terms of revenue and geography — a risk that’s grown too large for the current weight it had in my portfolio.

I’ve decided to keep 75% of my position. The stock remains in a strong bullish trend, and there could be further upside in the short term. But I’m also being cautious. With the potential impact of U.S. tariffs — which may or may not materialize, depending on how serious Trump’s rhetoric turns out to be — I'm choosing to de-risk a little.

I’ve learned from past mistakes with $SMCI (-9,91 %) (sold 100% for less than half the price of its peack) and $APP (-6,13 %) (keeping 100% of it), where I held onto full positions despite feeling the stocks were clearly overvalued. I could have sold partial positions and added back later at much better prices.

If $CLS (-7,11 %) experiences another meaningful pullback, I’ll likely buy back in. For now, the proceeds from this partial sale will remain ready for better opportunities or better entry points. That said, $CLS (-7,11 %)

still holds the third-largest position in my portfolio — and for good reason.

77

Valores en tendencia

Principales creadores de la semana

<contenedor>Datos LSX</contenedor> · Datos financieros de FactSet