$NDAQ (-3,51 %)

$RTX (+2,29 %)

$KO (-0,49 %)

$MMM (-0,52 %)

$NOC (-0,62 %)

$LMTB34

$OR (-0,91 %)

$TXN (+2,96 %)

$NFLX (-5,23 %)

$HEIA (+1,44 %)

$SAAB B (+5,24 %)

$UCG (-2,45 %)

$BARC (+4,75 %)

$GEV (-2,46 %)

$TMO (+1,42 %)

$T (-1,96 %)

$MCO (-3,54 %)

$IBM (-3,44 %)

$SAP (-3,65 %)

$TSLA (-0,77 %)

$AAL (-2,16 %)

$FCX (-1,24 %)

$HON (-1,1 %)

$DOW (-0,4 %)

$NOKIA (-1,63 %)

$TMUS (-0,98 %)

$INTC (-3,2 %)

$NEM (+0,75 %)

$F (-1,11 %)

$PG (+0,6 %)

$GD (-0,83 %)

Debate sobre INTC

Puestos

4103D·

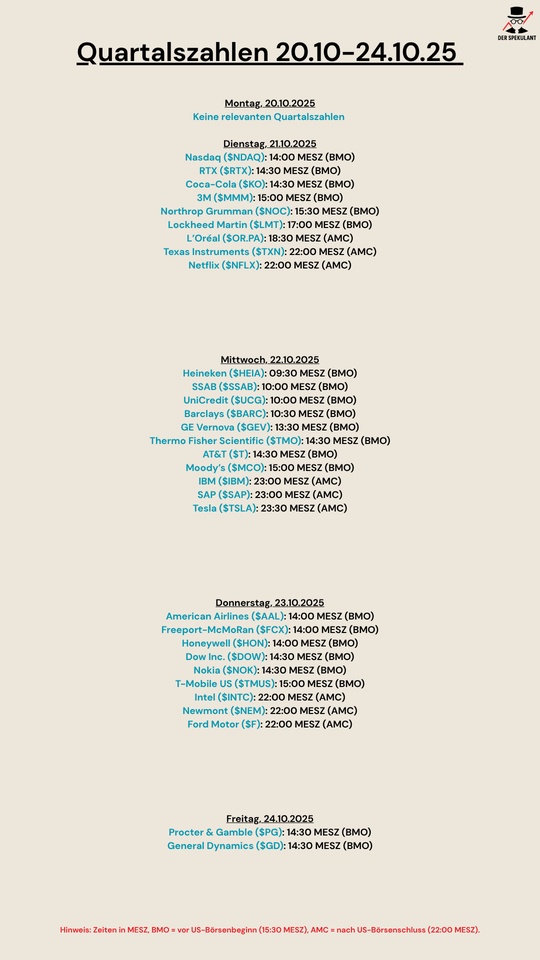

Quartalsberichte 21.10-24.10.25

33

1Semana·

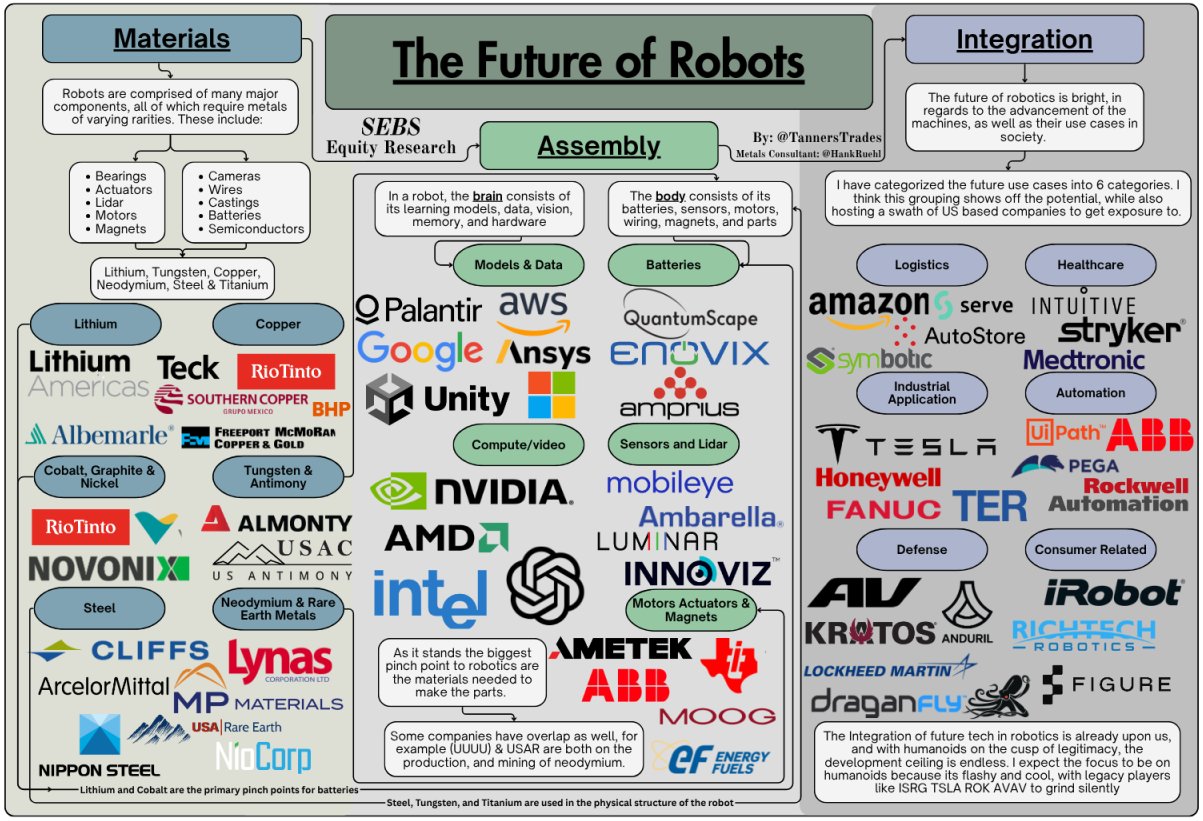

The Future of Robots 🤖🦾🦿

$ISRG (-2,4 %)

$PATH (-7,7 %)

$RR

Here is an exciting overview, for me the most attractive in terms of growth/potential of the stocks I know $RR

$PATH (-7,7 %) also $ISRG (-2,4 %) I would perhaps add to the portfolio again in the event of a correction. However, there are some stocks I don't know either.

What do you think are the most exciting stocks on the list, where should we perhaps take a closer look?

$AMZN (-1,75 %)

$MSFT (+0,65 %)

$NVDA (-1,17 %)

$AMD (-4,24 %)

$GOOGL (+0,53 %)

$GOOG (+0,51 %)

$RIO (+1,35 %)

$ALB (-0,6 %)

$INTC (-3,2 %)

$PLTR (-3,25 %)

$IRBT (+3,21 %)

$SYK (+2,17 %)

$MDT (-0,3 %)

$LMT (-0,89 %)

$DPRO (-6,47 %)

3939

15 Comentarios

Chris@Multibagger

1Semana

•

33

•Ver todas las 4 respuestas adicionales

1Semana·

My biggest mistakes so far

Reading time: 10 minutes

Mistakes are to the stock market as volatility is to the chart. Looking back, they are what hurts the most - but also teaches the most. In recent years, I have deliberately tried out many strategies in order to develop my own system. There have been some hits - but also misses, which have shown me what really counts in the long term.

This article is primarily aimed at new investors. I hope to save you from making one or two costly mistakes - or at least to show you what really matters if you want to invest sustainably.

Five examples are particularly influential. They mark the turning points at which I went from being a pure yield hunter to a structured investor.

1. historical performance overvalued

My entry into the $INRG (-1,37 %) (iShares Global Clean Energy ETF) was, in retrospect, almost textbook bad timing. I bought when the story sounded perfect: energy transition, political tailwinds, ESG money, green euphoria. The share price was close to an all-time high and fund providers were outbidding each other with promises for the future.

I let myself be dazzled - not by fundamentals, but by charts and headlines. The ETF portfolio consisted mainly of highly valued solar and hydrogen stocks with P/E ratios that were beyond all reason. I didn't really understand the product and only saw the impressive historical performance.

After a few months, I was down around -17% and realized the loss - a classic example of past performance bias. Today, the ETF is trading significantly lower again.

Learning:

High historical returns are not an argument, but a warning. When a sector is already overrun by institutional money, the regression to the mean begins. Since then, I have checked the composition, valuation levels and the cycle of the narrative for every investment. An ETF is only as good as its components - and hype is no substitute for analysis.

2. value trap instead of value opportunity

$INTC (-3,2 %) (Intel) seemed to me at the time to be a classic underperformance opportunity: lower P/E ratio than $NVDA (-1,17 %) (NVIDIA) or $AMD (-4,24 %) (Advanced Micro Devices), solid cash flow, decent dividend. I saw the numbers, not the structure.

The company has been struggling for years with innovation gaps, manufacturing problems and a protracted strategy. Margins were falling, market share was shrinking - but the valuation looked attractive. This is precisely the nature of a value trap: cheap because the business model is losing competitiveness.

I held on to the thesis for too long and eventually realized a loss of around -21 %. Despite the current upswing, Intel is still lagging behind today, while its competitors have further extended their lead.

Learning:

Valuation alone is not a safety net. Favorable multiples are often a symptom, not an opportunity. I have learned that capital flows, technological dynamics and management quality are crucial. Value only works if the business model is intact - not if you are hoping for a renaissance that is fundamentally unproven.

3. "What falls is cheap" - the fallacy using the example of $PYPL (-1,46 %)

(PayPal)

Another classic mistake: the belief that a sharp fall in the share price is automatically a good entry point. After PayPal's massive correction in 2021, I thought this was a rare opportunity. The company was once overvalued - no question - but I interpreted the setback as a downward exaggeration.

I got in after the share had already fallen sharply and even bought more as it continued to fall. The assumption: "It won't fall that low again." But it continued to fall - and has not recovered sustainably to this day. The exaggerated valuation premium from the boom years was simply no longer justified.

In the end, I realized a loss of around -44 %. The share will probably never reach the old highs again because the market environment, margin structure and growth have changed permanently.

Learning:

A falling share price does not automatically make a share cheap. You have to examine why it has fallen - and whether the fundamental situation has changed. An exaggeration on the upside is often followed by an overcorrection on the downside, and the old valuation remains out of reach for years. Today, I prefer to invest in companies whose trend is intact instead of speculating on "comebacks".

4. warning signals ignored - the example $CLI (+0,85 %)

(Cliq Digital)

For those unfamiliar with CLIQ, the company positions itself as a streaming provider - similar to $NFLX (-5,23 %) (Netflix), only much more niche. On paper, everything seemed to fit: high margins, strong growth, an attractive dividend and a barely noticed small cap with potential.

I saw the opportunities - but not the contradictions. The business model was difficult to understand, the reporting was incomplete and the short interest was extremely high. Nevertheless, I held on to the position - "because the figures were so good".

In the end, I realized a loss of around -26 %, including dividends. Today, the value is almost 90 % lower.

Learning:

If you don't understand a business model, it's not a good idea to be invested. Transparency is not a nice-to-have, but a must. In small caps in particular, you should check carefully whether growth is real, repeatable and sustainable. Since this experience, I have avoided business models that I cannot explain in two sentences - and take high short ratios as a serious warning signal.

5. trend understood - implementation missed

I wanted to focus on the self-service trend early on: Terminals for fast food chains, supermarkets, airports. A massive growth market - but I was looking for the wrong player. I found $M3BK (-2,48 %) (Pyramid), a small German company with a reverse IPO structure, hardly any investor relations, low liquidity and a non-transparent balance sheet.

I invested, convinced by the trend - not the business model. The share fell for months and I realized a loss of around -34%. Today it is trading at penny stock level.

Learning:

A strong trend alone does not make a good investment. The decisive factor is who has the real leverage in the value chain. It is often not the visible brands that benefit, but the blade manufacturers in the background - suppliers, infrastructure companies, platform providers. I have learned to analyze the ecosystem first and then look for the most profitable position in it.

Overarching learnings

These five mistakes were expensive, but their impact was priceless. Today, they are an integral part of my methodology - both in the 10B model (for growth opportunities) and in the Hidden Quality Radar (for quality values).

1. foundation beats narrative:

Stories are loud, but numbers are honest. Today, I check every investment for cash flow quality, return on capital and strategic positioning - and only then for valuation.

2. timing is crucial - but only in the right context:

I used to think that timing was unimportant, the main thing was to invest for the long term. Today I have a more differentiated view: the time of entry is a decisive factor in determining the risk/reward profile. If you buy in euphoric phases, you often pay for the correction years later. On the other hand, those who invest in downward exaggerations - with fundamental analysis and patience - gain a massive advantage. Timing is therefore not a game of chance, but the result of preparation, market observation and discipline.

3. accept small losses:

Discipline beats hope. Getting out early when things go wrong saves capital for better opportunities.

Here I would like to recommend a great article by @DonkeyInvestor recommend: https://getqu.in/eymPwi/

4 Transparency and management count:

I only invest in companies whose strategy and communication are transparent. Trust is not a gut feeling, but a data point.

These experiences have shaped the way I think today: patience instead of greed, quality before valuation, understanding before actionism. I have learned that you don't always have to be right on the stock market - you should think consistently.

Mistakes are inevitable. But if you reflect on them honestly, you build up your expertise with every bad experience.

What mistakes have shaped you - and what have you learned from them?

6262

16 Comentarios

Thanks for the article.

I also find myself in a few things.

Now I'm really trying to understand the reasons why hypes arise, why a share falls, sinks, etc.

A mistake I made yesterday:

I am convinced of $RACE, invested all my liquid cash yesterday instead of waiting a bit. It was a rare opportunity, so to speak.

As you can see now, today would have been a better opportunity.

Learning = Don't let your greed drive you and sometimes watch the market from the sidelines. The stock market always likes to exaggerate in both directions.

Well, in the long term, Ferrari is one of my favorites and almost a collector's item.

I also find myself in a few things.

Now I'm really trying to understand the reasons why hypes arise, why a share falls, sinks, etc.

A mistake I made yesterday:

I am convinced of $RACE, invested all my liquid cash yesterday instead of waiting a bit. It was a rare opportunity, so to speak.

As you can see now, today would have been a better opportunity.

Learning = Don't let your greed drive you and sometimes watch the market from the sidelines. The stock market always likes to exaggerate in both directions.

Well, in the long term, Ferrari is one of my favorites and almost a collector's item.

•

44

•

2Semana·

Does the Nvidia deal make Intel shares interesting?

Background and Nvidia investment

Intel is under pressure and has seen its share price fall sharply, but Nvidia is now investing USD 5 billion and is working with Intel on chips for PCs and data centers, especially for AI applications.

Following the announcement, Intel shares rose by 25 percent - the strongest rise in decades.

The cooperation reduces risks for Intel, for example due to the high level of competition with AMD and the previous dependence on customers from China, Europe and Taiwan.

Effects on the competition

The deal is challenging for AMD, as the cooperation between Nvidia and Intel weakens AMD's market position in the server chip business.

Nevertheless, AMD remains technologically competitive, especially in modular chip architectures, and has customers such as Meta for their data centers.

Nvidia benefits strategically as it will be closer to the US market and less dependent on TSMC and chip production in Taiwan in future - this reduces geopolitical risks.

Fundamental key figures and outlook

Intel has shown major weaknesses, such as stagnating sales (approx. USD 50 bn) and a lack of profit.

Nvidia is significantly larger and more profitable; the Nvidia investment is small for Nvidia, but an accolade for Intel and an enormous strategic plus.

Valuation

According to Kuhnert, Intel's stock market value after the increase does not yet sufficiently reflect the potential; the deal is actually worth more to Intel than the 30% increase in the share price to date.

There are risks in terms of competition law (monopoly position for Nvidia), but the current focus is on national security, which is hampering regulatory intervention.

Analysts expect a setback of around 10% for Intel, while prices of USD 220-240 are forecast for Nvidia over the next 12 months.

Intel is seen as an interesting normal portfolio addition, especially for long-term investors and as a hedge against geopolitical tensions, e.g. around Taiwan.

Nvidia remains the favorite in the AI megatrend, Oracle is another example of growth in the cloud and AI sector.

Conclusion

The Nvidia deal provides Intel with new opportunities for a turnaround and strengthens its position in technology and AI.

The share is volatile in the short term after the recent rise, but offers long-term potential, especially for investors with an eye on AI, robotics and security risks in the chip sector.

Charts/analyst recommendations in my lounge. https://steady.page/de/finanzen-anders/about

steady.pageFinanzen Anders

55

2Semana·

Chips – Intel & AMD

$INTC (-3,2 %) is in early talks with $AMD (-4,24 %) to manufacture some of AMD’s chips at Intel fabs, per Semafor. Most AMD designs are currently made by TSMC, which still leads in advanced tech. Any deal would likely cover less advanced chips, with no details yet on scale or investment.

11

1 Comentario2Semana

Probably has no added value, only a deal to make the orange dictator happy, and protect from tariffs

••

3Semana·

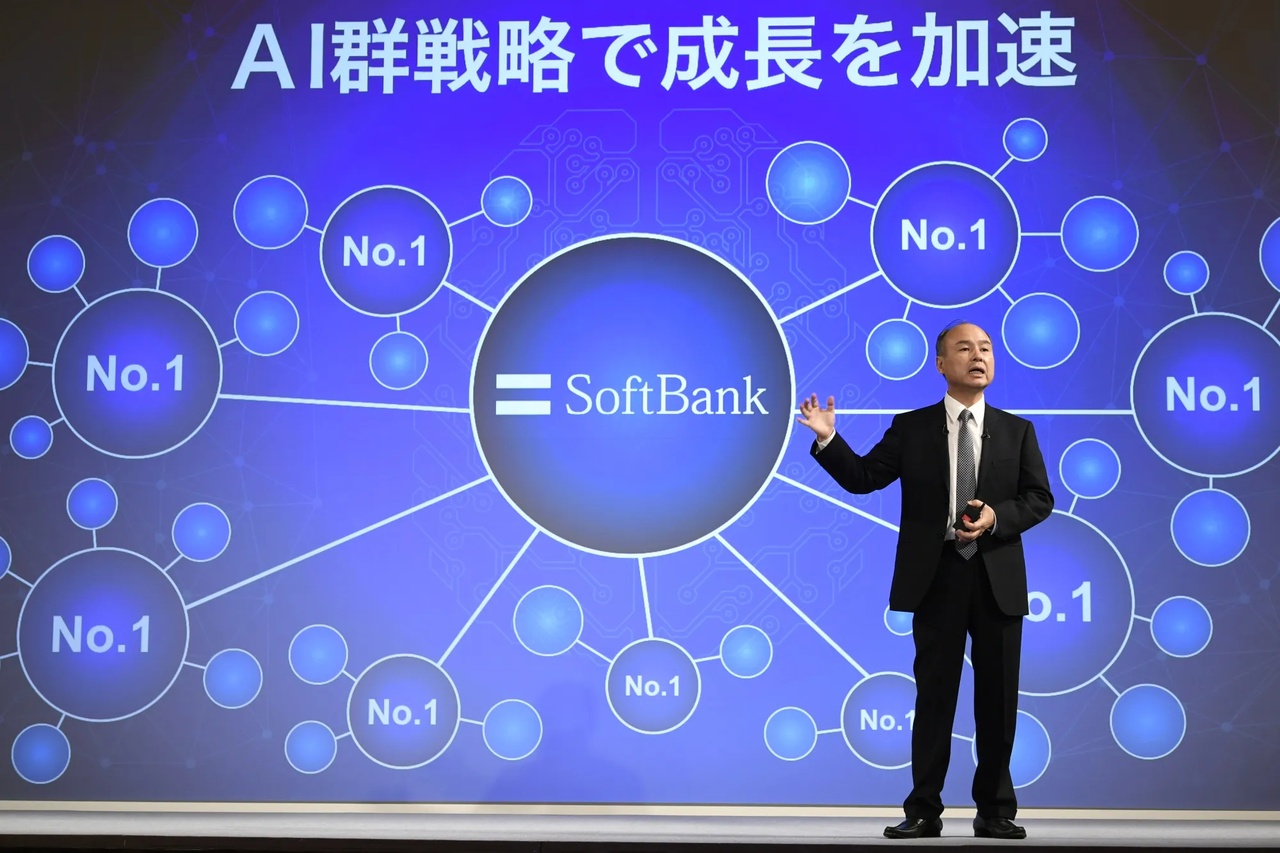

SoftBank update ℹ️ - share price gains of over 150%

I have already described here several times this year why I think that the SoftBank Group share $9984 (-6,65 %) is a top pick when it comes to AI. Now the share price confirms this assumption with an increase of more than 150% since April.

What is the reason for the sharp rise? The answer is short and clear: AI. The reorientation towards everything to do with AI in order to "become the number 1 platform provider for AI" has caused the share price to explode.

So many new projects were announced in 2024/2025 that it was impossible to keep up. The 500 billion dollar Stargate project in the USA and the 40 billion dollar financing round for OpenAI were particularly prominent.

Added to this is a strategic investment of 2 billion dollars in Intel $INTC (-3,2 %)the announcement by the portfolio company ARM $ARM (-1,72 %) to switch from pure IP licensing to its own chip design, a JV with OpenAI for enterprise AI in Japan, a JV with TempusAI $TEM (-4,23 %) for medical AI in Japan, a JV with Intel for the development of energy-efficient memory chips (Saimemory) an IPO of the portfolio company and No. 1 fintech in Japan PayPay in New York, the plan together with NVIDIA $NVDA (-1,17 %) to convert the Japanese telecommunications network for AI workloads (AI-RAN), several data centers under construction (independent of Stargate)........ The list could go on and on, but I think the message is clear.

In my opinion, no company is so broadly positioned when it comes to AI. From energy (SoftBank Energy), to the chips used (ARM, Ampere, Graphcore), to the data center as a whole (Stargate, others), to the AI itself (OpenAI) and the AI applications (various). They are active along the entire value chain.

I was also skeptical at first about how to manage all of this at once, also in terms of the sheer amount of work involved, but the first results are becoming visible. SoftBank is building 2 data centers with a capacity of 1.5 GW with OpenAI as part of Stargate. The fact that they are only involved in part of the Stargate data centers and then only with OpenAI is very positive, as I consider the projects on this scale to be very realistic. In addition, there are no conflicts about the technology to be used and SoftBank can clearly favor its portfolio companies in everything.

It will also be interesting to see how the 40 billion financing round progresses. The second half should be invested by the end of the year. With an agreed valuation of 260 billion dollars (plus cash 300), SoftBank should hold around 10% of OpenAI after the financing round. Now that NVIDIA has announced that it will invest 100 billion in OpenAI, although it is still unclear when, how and at what valuation, this is likely to have a massive impact on the value of SoftBank's stake.

The two Vision Funds are also doing well and have recovered from the difficult years. They are now another positive influence on the company's profits. However, they are becoming less and less important as more and more staff are withdrawn from them to work on the AI projects. Fewer new positions are also being added and some older ones are being liquidated.

I am particularly interested in how SoftBank's chip design ambitions will develop over the next few years. Now already in possession of three chip designers (ARM, Ampere Computing and Graphcore), a partnership with Intel (Saimemory) and a strategic stake in the Japanese giga start-up Rapidus, the focus is becoming increasingly visible. How quickly will the restructuring of ARM take shape? Will individual portfolio companies be merged? Will Rapidus, with its impressive interim results, be a success?

These questions will continue to occupy me over the next few years and I will continue to keep a close eye on the milestones achieved so far. The 2030s could definitely be transformative for the SoftBank Group.

1919

4Semana·

SK Hynix expands: 20 new EUV systems planned within 2 years

$HY9H (-1,2 %)

$ASML (-1,3 %)

$INTC (-3,2 %) . $MU (-2,2 %)

SK Hynix is now the market leader in memory, also thanks to greater use of EUV than its competitors. According to current expansion plans, this is set to continue: Within just two years, around 20 more EUV systems are to be purchased to equip new factories and are intended for HBM and the latest memory solutions.

Number of EUV systems to double

SK Hynix already uses around 20 EUV systems from ASML in the Netherlands in its production. According to South Korean media today, this number is set to double by 2027, which could make SK Hynix one of the three largest customers.

According to analyses, SK Hynix would then have as many or even more EUV systems in use than Intel, which is rather atypical for a memory manufacturer. The number 1 in EUV is of course TSMC, which is unbeaten, while Samsung is number 2 as the world's second largest foundry, because it was here, in the logic sector, that EUV established itself many years earlier.

Intel completely missed the boat and is now having to pay for its failure with extensive problems including mass redundancies and new partnerships for financial injections.

SK Hynix, on the other hand, is extremely active in the new EUV systems. The manufacturer has been using EUV since 2021, and the South Koreans have already taken delivery of their first high-NA EUV system. This is now being used to test when it will be worth using in series production.

Micron is taking exactly the opposite approach: Here, EUV has only just been ramped up and is now slowly being integrated. However, the difference of four years does not seem to make as much of a difference in memory production as it does in the logic sector, as Micron also continues to make a lot of sales and high profits. After four years without EUV, Intel had once again fallen behind TSMC in terms of processor production.

The new EUV and later also high-NA EUV systems should help SK Hynix to bring new products to market faster and with good yields. The advantage of the newer equipment is always that the number of exposure steps can be reduced, resulting in fewer errors. Ultimately, this saves time and costs, even though the initial investment of several hundred million euros per exposure system is huge. The scanners are to be used in both the M15X factory extension in Cheongju and the M16 factory in Icheon.

www.computerbase.deSK Hynix expandiert: 20 neue EUV-Systeme binnen 2 Jahren geplant

4Semana·

Sometimes you have to be satisfied with the little things.

Yesterday evening my short on $INTC (-3,2 %) was stopped out after all. But ok. There is still something left.

1111

11 Comentarios

@Iwamoto I no longer have my Oracle long (unfortunately I bought it too early), gold is running with a long OS, which I posted. I also bought a long on Siemens Energy a week ago during the setback. Also long on Rheinmetall, Hensold, NVIDIA and inliners on Siemens, CoBa and MTU... If you are interested in which OS I have exactly, just write me which one and I can send you the WKN... Long on MELI and Adobe would certainly also be interesting right now... ✌️ HG

•

11

•4Semana·

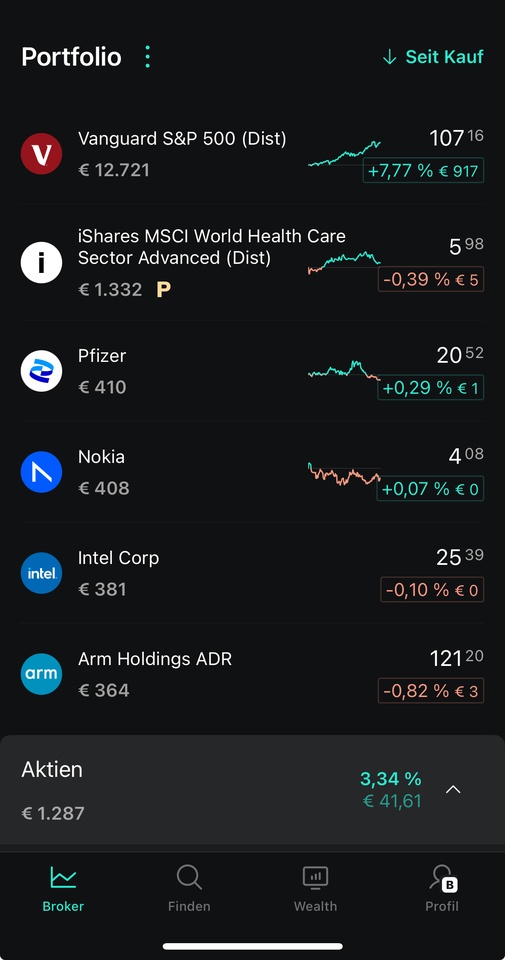

Today I bought extremely unpopular shares 🦍

Good morning,

Today I actually bought the first tranche of the following shares:

Intel - Arm Holding - Nokia - Pfizer

---------------------------------------------------------------------------------------------

$INTC (-3,2 %) Nobody believes me, but I actually wanted to buy Intel last week before the significant rise, after the rise I speculated on a setback, which didn't turn out to be so strong and today I simply bought.

Why Intel? What distinguishes Intel from AMD and NVIDIA?

Intel is the only one that develops and also produces itself. Of course, this also entails risks, but it is also the case that Intel is the only non $MU (-2,2 %) is the only non-Asian chip manufacturer that has the latest ASML machines. Is that not one of the reasons why even Nvidia is now investing in Intel... By the way, I actually bought Micron today, simply to increase the size of the position.

In my opinion, anyone investing in Intel today should have a lot of patience. As you know, I don't have much of that, so maybe this will be my gym.

--------------------------------------------------------------------------------------------------------

$ARM (-1,72 %) Arm develops the Arm architecture for processors, which are particularly efficient and do not require cooling, which is why you find them as standard in smartphones, tablets and other devices, and sells the licenses to Qualcomm, Apple, Samsung and Nvidia, for example.

They are involved in almost all smartphone chips, earning money from the license without having to bear any production costs themselves.

The risks are a very high valuation, in which a lot of growth is already priced in. Strong dependence on the smartphone market, competitors could contest market shares and the company is very dependent on the Asian market.

--------------------------------------------------------------------------------------------------------

$NOKIA (-1,63 %) is quite well positioned and a leader in 5G network technology. For example, it controls over 29% of the 5G market outside China and is already in the lead in 6G... The business model is quite cyclical, investment intensive and the technological change is very fast.

--------------------------------------------------------------------------------------------------------

$PFE (-0,47 %) has made many strategic acquisitions in recent years. The acquisitions of Seagen and currently Metsera, among others, show that Pfizer is making targeted investments in growing and lucrative therapeutic areas. Whether the pipeline will be successful remains to be seen and is probably one of the greater risks.

--------------------------------------------------------------------------------------------------------

I have mentioned some of the risks, there are probably countless. The stocks fit into my portfolio quite well, as I mainly invest in boring ETFs and the weighting of these individual stocks is too low to significantly jeopardize my basic investment. If things go really badly, the money is gone, if things go reasonably badly, I have dividend stocks 🤪

1111

8 Comentarios

But now also hold for 2 years and don't sell again at - 4% 👀😊

•

88

•Valores en tendencia

Principales creadores de la semana

<contenedor>Datos LSX</contenedor> · Datos financieros de FactSet